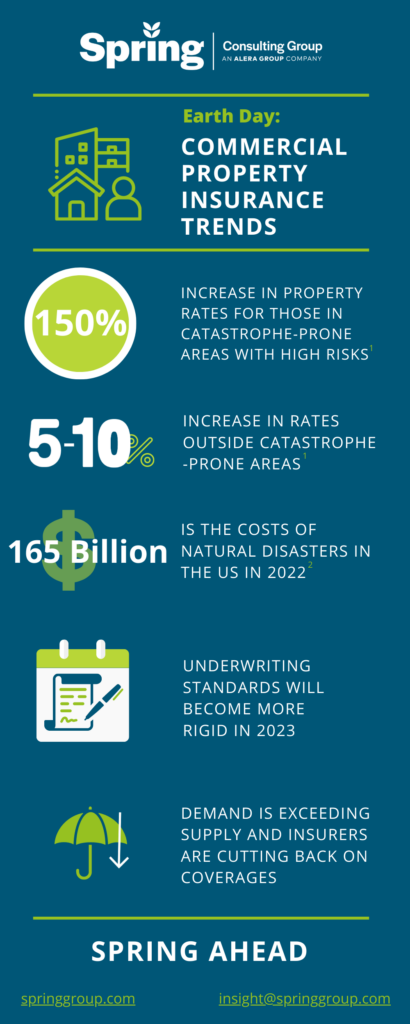

This Earth Day, we wanted to highlight the effects of climate change and natural disasters on the property & casualty insurance industry. Check out the infographic for a quick glimpse of where things stand.

Sources:

1 Alera Group’s 2023 P&C Market Outlook + Commercial Property Update

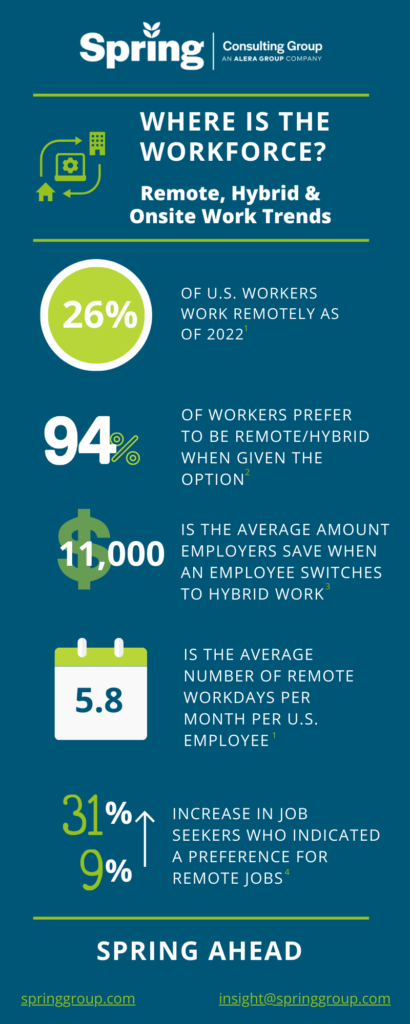

As we transition past the pandemic, we are seeing shifts in remote, hybrid, and onsite practices across the US. Below are some of the top trends impacting workforces nationwide.

1Zippia. “25 Trending Remote Work Statistics [2023]: Facts, Trends, And Projections” Zippia.com. Oct. 16, 2022

2Alera’s EB Market Outlook

3https://globalworkplaceanalytics.com/telecommuting-statistics

4https://fortune.com/2023/01/25/workers-prefer-remote-first-roles-hybrid-work/

On National Pharmacist Day, our Assistant Vice President of Pharmacy, Jennifer Perlitch, a clinical pharmacist, is offering her view and surprising facts about the pharmacy industry today, as well as how she’s helping Spring’s clients combat the difficult climate.

The fact that pharmacy costs continue to skyrocket is not groundbreaking news. But what many people aren’t aware of is the “why” behind the increases. Several factors influence the price of a prescription drug such as the drug’s uniqueness and effectiveness and how much, if any, competition exists in the market. Unfortunately, there are times when drug prices increase significantly without important new clinical evidence. Regardless of why, as these prices continue to increase, it creates a significant burden on patients who need to pay deductibles or coinsurance.

So, what’s going on behind the scenes? Pharmacy is just one piece of the healthcare puzzle, and we know overall healthcare costs are also on the rise. There are five key reasons why healthcare costs are rising1:

- Aging population: The Baby Boomers, one of America’s largest adult generations, is approaching retirement age. As such, they are leveraging the system more, as seniors have the most need for prescription medication and other health services and are now or will soon stop contributing to the workforce.

- Chronic disease prevalence

- Rising drug prices

- Healthcare service costs, such as expensive procedures and physician salaries, are one component of the system that’s trending upwards

- Administrative costs, such as financial transactions and patient services, account for between 15%-25% of total healthcare expenditures2

When it comes to pharmacy specifically, there are two of these areas that I want to dive further into.

Chronic Disease Prevalence

Six out of every 10 adults in the United States have a chronic disease or condition, according to the Centers for Disease Control and Prevention (CDC). The most common chronic conditions in the U.S. include:

- Heart disease

- Stroke

- Cancer

- Diabetes

- Chronic kidney disease

- Chronic obstructive pulmonary disease (COPD)

Chronic conditions often require long-term medical attention and prescription drugs which often delay disease progression and improve or preserve quality of life. Some conditions may limit daily living activities, which could warrant use of home health care or other support services. The challenges of living with chronic illness also may increase the likelihood of suffering from anxiety, depression, and other mood disorders.

All these factors make caring for chronic disease patients more complex and resource intensive. There is a strong relationship between healthcare costs and chronic diseases in the United States. According to a report from the American Action Forum, the U.S. spends about $3.7 trillion each year for the treatment of chronic health conditions and the resulting loss of economic productivity.

In addition, the COVID-19 pandemic has caused some chronic disease patients to delay or avoid essential care. This means that chronic disease patients are spending less on healthcare services in the short term, but this will likely have damaging health and financial effects in the long term. When chronic disease patients delay care, they risk suffering from potentially life-threatening complications as a result. The long-term management of these complications will likely contribute to rising national health expenditures and consumer costs.

Rising Drug Prices

According to the Organization for Economic Cooperation and Development (OECD), the average American spent about $1,226 on prescription drugs in 2019 (the most recent year with internationally comparable data). This per capita cost is significantly higher than other developed countries. These costs will likely continue to increase, as the Centers for Medicare & Medicaid Services (CMS) estimates that prescription drug spending in the U.S. will grow by 6.1 percent each year through 2027.

The spending growth is due in part to a continuing emphasis on specialty medications and precision medicine. Specialty drugs are high-cost prescription medications used to treat complex conditions such as autoimmune diseases, chronic conditions, and cancers. Some therapies utilize genetic data to deliver a highly targeted, personalized treatment. The complex nature of these drugs makes them very costly to develop and distribute.

Drug pricing strategies also contribute to rising healthcare costs. Drug manufacturers establish a list price based on their product’s estimated value, and manufacturers can raise this list price as they see fit. In the U.S., there are few regulations to prevent manufacturers from inflating drug prices. There is no federal oversight; the federal government does not regulate drug pricing. It does however encourage the development of generic drugs through an abbreviated approval process to help improve access and affordability, but this often takes years.

Private Health Insurance and Out-of-Pocket Costs

Private health insurance spending growth accelerated slightly to 4.5 percent in 2018, from 4.2 percent in 2017. This trend is the net effect of faster spending growth in many services such as physician and clinical services and prescription drugs, which were only partly offset by slower projected growth in the net cost of private health insurance spending. In 2019, private health insurance spending growth slowed to 3.3 percent, which, in part, reflects the estimated impact of the effective repeal of the individual mandate within the Affordable Care Act (ACA). Over the latter period of the projection, 2020-27, private health insurance spending is projected to grow by 5.1 percent per year on average (or 1.8 percentage points more rapidly on average than in 2019) resulting mainly from the lagged response to higher projected income growth, especially in 2020-22.

Out-of-pocket (OOP) spending growth is projected to have grown faster at 3.6 percent in 2018, from 2.6 percent in 2017, due to faster income growth, as well as higher average deductibles for private health insurance enrollees with employer sponsored insurance. During 2020-27, out of pocket spending growth is projected to accelerate to an average annual rate of 5.0 percent, which is a similar rate as private health insurance during this period. During this timeframe, somewhat faster growth was projected for 2022, a year in which OOP spending was anticipated to grow 5.4 percent related to the excise tax on high-cost insurance plans3.

How can the Spring Consulting Team help?

As an employer you want the best for your employees and their families. Ensuring your pharmacy benefits meet their needs and supports their well-being is a critical component of your benefits package.

Evaluating your current pharmacy benefit offerings is an excellent place to start!

Here is an overview of our Pharmacy Benefits Consulting Services:

Evaluate current Pharmacy Benefit Management (PBM) Services

– Conduct annual/semi-annual reviews of PBM services, contract compliance, and performance guarantees and provide recommendations/assist in developing a plan to rectify any deficiencies.

– Perform follow-up activities as necessary to ensure contract compliance, efficient program management and responsive account management

– Review and evaluate utilization and any other key reports to assess trends/areas for opportunity

New PBM Implementation Services

– Facilitate implementation of the new PBM services including transition of benefit design, formulary, eligibility and pre-existing prior authorization approvals to new PBM

Pharmacy Benefit Consulting Services

– Review pharmacy benefit packages options and assist in selecting best option for your business needs

– Evaluate and recommend options for managing specialty pharmacy products

– Analyze the performance of the retail, mail order, and specialty pharmacy benefit option and make recommendations to improve the management of the drug cost trends

– Review and evaluate clinical and other optional programs and provide recommendations

– Meet with key stakeholders semi-annually (or quarterly) to review drug plan performance and identify recommended changes going forward.

Account Management Services

– Manage the ongoing relationship and communications with the PBM regarding specific eligibility and benefit updates

– Represent and advocate for business needs with the PBM when needed

– Participate in all PBM and client meetings related to pharmacy benefit and mail order services

Given the perfect storm outlined above, now is a great time to reassess all your benefits programs, but especially those related to pharmacy; please get in touch if you would like to optimize in this area.

1 https://www.definitivehc.com/blog/5-reasons-why-healthcare-costs-are-rising

2 https://jamanetwork.com/journals/jama/fullarticle/2785479

3 https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/Downloads/ForecastSummary.pdf

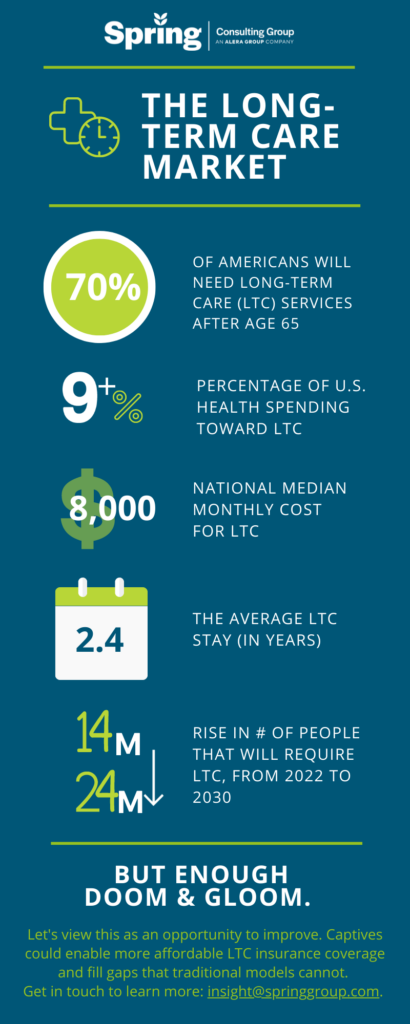

At the VCIA 2022 Annual Conference, our Managing Partner participated in a panel that highlighted the scary long-term care landscape, but that ended on a high note in exploring the possibility of captives as a next generation solution for long-term care insurance.

With innovation embedded in the DNA of both Spring and captive insurance, we are interested in helping reshaping the long-term care market of the future. Check out the other discussions our team members had on VCIA session panels, or get in touch to talk in more detail about long-term care captive strategies.