Spring’s VP Prabal Lakhanpal is breaking is tying together employee benefits, captives, and third party risk in this piece published in Captive International.

Dazed & Confused

Think about your last visit to the doctor. Did you know what questions to ask? Did you leave with a clear picture of the next steps or alternative options? Did you know the cost of your appointment and treatment path before starting it, or what would be covered by your health insurance? If you answered “no” to any of these questions, you are certainly not alone.

Bend Financial[i] recently conducted a survey that showed that only 29% of people were completely confident in their ability to navigate the healthcare system, whereas 56% were entirely confused when it comes to health insurance. Unfortunately, an alarming subset of consumers opt to avoid healthcare completely, too defeated by the complexity.

Beyond health insurance, employees must navigate the suite of benefits offered to them by their employer. While these are meant to provide support, they can cause more confusion when employees are looking for assistance. Employers must consider how introducing a new program or benefit will fit into their overall strategy and integrate the resources, without adding to the complexity employees face.

[i] https://www.bendhsa.com/newsroom/more-than-half-of-americans-confused-by-health-insurance-including-hsas

Breaking Through the Fog

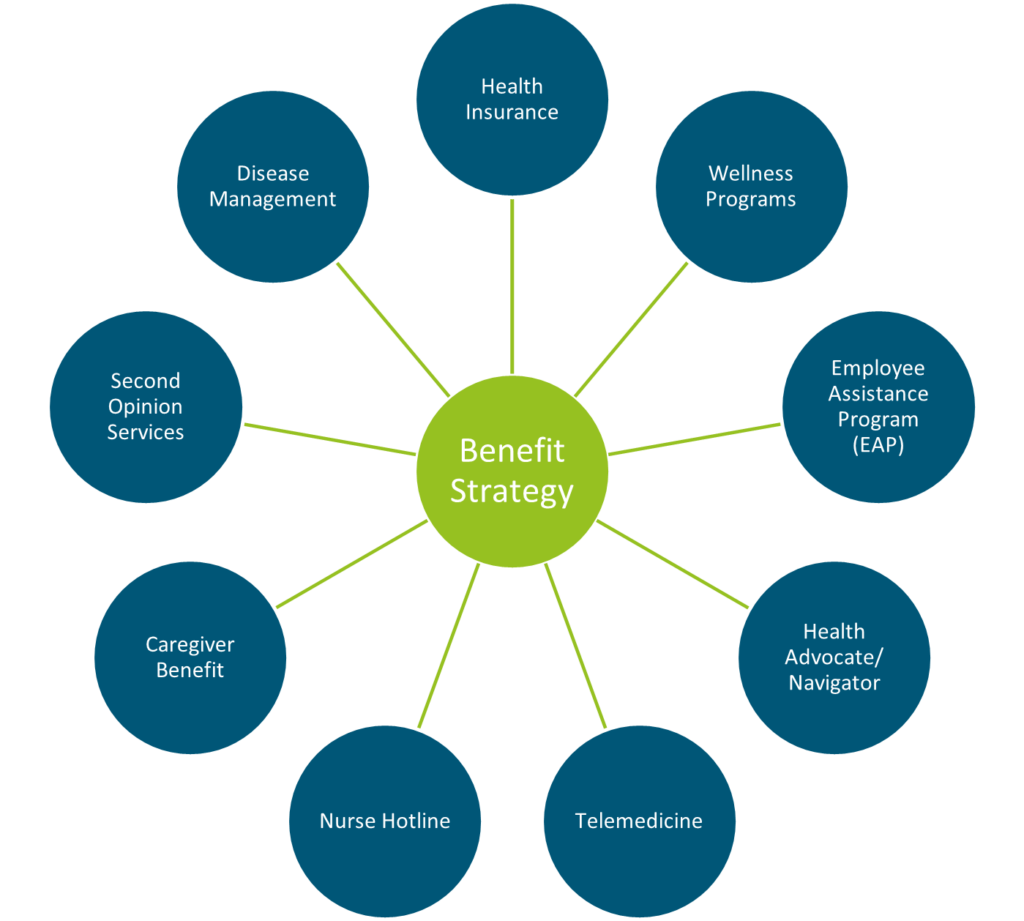

Advocacy tools have popped up as a response to the confusing environment. These tools offer a wide variety of clinical, educational and administrative resources, such as:

- Helping members understand test results or treatment plans

- Advocating for members with complicated conditions and managing their care

- Coordinating care at inpatient facilities

- Identifying top providers

- Arranging second opinions

- Providing information about alternative prescription options

- Assisting employers to understand health risks through biometrics, claims and other data

- Developing customized Employee Assistance Programs (EAPs) or other life coaching services

- Reviewing medical bills and allowing for transparency of costs

- Facilitating prescription drug delivery

- Assisting with wellness goals

- Accessing telemedicine

- Booking appointments and sending reminders

- Optimizing HSA, FSA and HRA accounts

- Integrating with other vendors offered by the employer

The landscape for these platforms is robust and ever-changing. The spectrum of vendors include those that offer:

1. Holistic approach

Major players may provide all of the above features on a one-stop shop model for employees.

2. Preventive approach

Some vendors focus on prevention of common conditions, encouraging employees to get annual eye exams, diabetes screenings, cancer screenings, medication adherence, and more.

3. Targeted approach

This last category of vendors specialize in support for employees with common chronic conditions including diabetes, hypertension and high cholesterol. While likely not the most costly conditions, the potential for savings and member support is significant when factoring in the volume at play. These vendors aim for condition management by giving members the tools to monitor and manage their conditions better on their own, hopefully necessitating less emergency care in the future.

Comparatively, other tools focus only on the highest cost conditions and members, such as cancer diagnoses. Offering a specialized tool for members going through this difficult time enables them to procure the best and most cost-effective care, while also giving them access to resources related to nutrition, mental health, and more. While available on a standalone basis, advocacy solutions may also be accessible to employers through their insurance carriers, Third-Party Administrators (TPAs), or Employee Assistance Programs (EAPs). Programs embedded with a carrier or TPA tend to focus on overall health management programs, disease management and wellness, as well as resolving billing issues and comparing costs of providers. A commonality across platforms is the prioritization of the consumer experience – offering easy, self-service access in mobile apps or online portals. Members typically have a single point of contact at the advocacy company, so they know who to call and do not have to navigate being transferred or having an unfamiliar staff member pick up their case. Overall, for employees, health advocacy platforms may:

- Help them get the most out of their insurance plans and programs

- Cut through the clutter of healthcare

- Promote health and productivity

- Increase preventive behavior

For employers, health advocacy tools can:

- Cause an uptick in employee engagement and satisfaction

- Increase health plan utilization.

- Yield savings in healthcare costs by allowing employers to better understand cost drivers,

- Facilitate the creation of more informed preventative and wellness programs and ultimately lead to a healthier population

Advocacy Adoption: Is It Right For You?

Ultimately, it is up to the employer to determine what programs would best support their employees. Based on the 2020 Integrated Disability Management (IDM) Employer Survey conducted by Spring Consulting Group, 61% of employers offer a health advocacy solution today, compared to only 41% in 2018. Determining which model and which vendor to select can be difficult as there are many players in the market. In assessing whether an advocacy tool would be a good fit for your organization, any decision around advocacy solutions should be tied to program objectives.

- Are you primarily concerned with cost savings?

Health advocacy solutions can provide cost savings to employers or health plans, as they direct employees to access only necessary healthcare services, perhaps at a lower cost facility than they otherwise would have used. A tool like this should, in theory, help avoid bigger, high-cost problems down the road by assisting the employee with addressing issues early. Certain vendors may even offer a cost savings guarantee. However, it will take time to see a possible Return on Investment (ROI). On the flip side, an advocacy solution can encourage greater utilization, such as for behavioral health services. While a higher utilization rate may mean increased claims, giving employees tools to access the services they need can lead to less emergent or high-cost care down the road. As such, you should determine if you are looking for immediate or long-term results.

- Are you looking for higher engagement in your health and benefits plans?

There is a lot of logic behind the argument that an advocacy tool will increase engagement. However, if an employer has had trouble engaging employees in the past, such as in wellness challenges, incentives, education, etc., nothing is guaranteed. Vendors claim that anywhere from 30% to 80% of employees will participate in their program, but this is highly variable based on different aspects of the program and the employer, such as program features or employer incentives.

- Are you focused on population health management?

By equipping members with the necessary tools to make health care decisions based on value and outcomes, better outcomes are achieved. The plan data will guide your decision related to population health management. For example if you are struggling with diabetes specifically, you may want to consider a targeted point solution focused on diabetes management before committing to a more comprehensive program that tends to be more expensive.

- Are you hoping to improve the employee experience?

With an advocacy tool, members have support to mitigate confusion around healthcare services, surprise billing, complex diagnoses…but it only works if members leverage the support. Programs should be communicated often and where possible linked to activity within the plan. We always recommend eliciting employee feedback before launching a program such as this, to ensure you are solving for problems that really exist for employees, instead of problems you think exist for employees. Sometimes our clients even roll out a smaller pilot program as a test before implementing the wider solution for the whole organization.

Most organizations will have a few different goals at play, which are not limited to those listed above, but typically there is a hierarchy to consider. Working with a trusted advisor can help to understand key differences and ensure programs are designed to work for the employer and their employees. At Spring, we routinely help employers vet solutions to find the one that is optimal for their goals and population.

Conclusion

Overall, health advocacy tools have risen in popularity for a reason. They address critical problems in our healthcare system – confusion, expenses, access, lack of trust – and serve as a different avenue for employers to limit the rising costs associated with healthcare. Advocacy helps ensure employees are understanding the care they receive and have greater visibility into actual costs. While results will vary by platform and organization, vendors are confident in their results; they report significantly lower healthcare trend for clients, compared to previous years when there was no advocacy program in place. With an ever-changing landscape, it is possible that health advocacy programs can bridge the gap between consumers and care, but only time will tell if they can make a long-term impact on the market.

Employees bring their whole selves to work each day which allows for the highly efficient, effective, and creative workforce we enjoy. As Human Resource professionals we appreciate the diversity of our workforce and continue to adjust within our employee benefit programs to meet the changing needs of our employees and their families. Top employers know that thinking more strategically about caregiving will help them fight for top talent and provide the corporate culture employees are seeking especially in this more complicated caregiving landscape brought on by COVID-19.

The concept of caregiving is not new but as our workforce evolves it is becoming more critical to consider caregiving as an area of opportunity within employee benefits. This shift, further amplified by the pandemic, highlights a cavern between top tier employers who appreciate the multitude of responsibilities employees must navigate versus those that hire people despite them.

The Rosalynn Carter Institute for Caregiving recently released Caregivers in Crisis: Caregiving in the Time of COVID-19. This thoughtful piece attaches hard data to the burden we have all experienced over the last 6 weeks. The data indicates that 83% of caregivers have increased stress since the start of the pandemic, and 42% have indicated that the number of other caregivers available to help them has declined. Caregivers themselves – in addition to those requiring care – are experiencing an increased burden from isolation, stress, financial concerns, and general instability.

Employers that are new to the concept can consider caregiving solutions as a continuum or suite of solutions; not a one size fits all approach or something that has to be implemented all at one time. A core offering typically includes:

- Educational resources

- Advocacy support

- Self-service tools

Enhancements allow for 24/7 live support and paid time off when necessary to address caregiving emergencies.

Defining Caregivers

AARP estimates that each year approximately 40 million American adults provide support to others with basic functions (i.e. activities of daily living). Many of those, including 75% of millennial caregivers are working.

For millennials in particular the stress of caregiving can be more challenging since they are typically providing care for more hours in a week, making less money and having less support from other family members (i.e. reduced family size). Also of note, millennials are the most diverse caregiving community to date (i.e., racially, ethnically and more likely to identify as LGBTQ+) which can be important to consider related to diversity and inclusion.

It is important to think broadly about caregiving solutions. In addition to introducing separate solutions, it is equally important to shift our mindset and expand common employer benefits that could be leveraged for extended family members (i.e. second opinions, medical guidance with challenging health diagnoses, etc.). The term caregiving must also extend beyond elder care of medical conditions but include children struggling with online school or developmental disabilities or Medicare eligibility and financial planning when moving into retirement. The goal of caregiving solutions is to support your employees as both caregivers and those needing care.

We have all heard the announcement on the airplane about putting on your own mask before helping others; employer sponsored caregiving is building on that logic and allowing your employees to more efficiently:

- Find educational information related to their caregiving needs

- Direct employees toward potential solutions

- Provide tools to support decision making

- Pair employees with short-term and long-term caregiving solutions

Caregiving support as an employee benefit is still in its infancy. Unfortunately, many employers do not realize the need, the impact on employee performance and the demand that exists at the employee level. A 2019 Harvard Business School Study, The Caring Company, indicates that while only 24% of employers surveyed believed employee caregiving influenced their employees’ performance at work, 80% of employees surveyed admitted that caregiving had an effect on their productivity. In addition, 32% of employees surveyed indicated that they left a job because of their caregiving responsibilities.

Employers who take a proactive position on caregiving support – along with the tools needed for successful roll out and measurement – will see a direct impact on attraction, retention, productivity, and corporate morale.

If your organization is interested in exploring caregiving support as an employee benefit, or is ready to identify partners for a best practice roll out, please reach out to our team.

As seen on Captive Insurance Company Reports (CICR)

As organizations have grown and globalization has created an international workforce, a lot of employers are faced with challenges around the selection, administration and management of their employee benefits across the globe. International benefits programs can be a complex maze to navigate, given the varying local cultures, business practices and legislations.

We are seeing an uptick in organizations looking to harmonize their global programs. The COVID-19 pandemic has accelerated this need. With increasing globalization and limitations of travel, employees are spending more time online virtually engaging with colleagues across the world. We have come to rely on digital connectivity, which makes it easier to share ideas and understand the experiences of others. As many organizations moved to a remote work environment, employees are wondering why they ever needed to be in a specific location every day, and relocation is on the rise. With all of this said, a siloed benefits program may not align with the upwards trend of globalization. As your international employees meet online, you will want them to find comparable policies and practices being followed, regardless of physical location.

As multinational corporations, employers are relying on businesses or consumers from other countries to drive business growth. It is important to understand how to appeal to a diverse customer and employee base – how to celebrate differences while bringing everyone together. Benefits and wellness programs can serve as a unifier, engrained in your culture as a way for employees to feel a sense of belonging. Creating and maintaining a strong culture is exceedingly difficult when you have an international workforce, and a synchronized benefits program is a great way to unite your people.

Traditionally there have been two major schools of thought on international programs. One is to have a completely decentralized benefits program, where each country’s local teams have control over benefit offerings. This approach has the least resistance as local teams are able to make decisions in the best interest of the local employees. From a global perspective, this limits the benefits that accrue to the organization as there is no coordination of carriers, limiting the ability to get preferential pricing. From an employee’s perspective, moving from one country to another for short-term and long-term assignments can mean a complete overhaul of their benefits. Alternatively, the second approach is where the head office controls most major aspects of the benefit offerings globally – including the carriers and the benefit plan designs. This option usually generates savings for the company, as employers are negotiating for global contracts. However, local partners usually push back on this approach or require accommodations. Providing accommodations and carve outs creates confusion and a lack of cohesiveness, eventually resulting in the slow disintegration of the global program.

One may wonder why creating such a program is the need of the hour. Most employers are interested in providing market competitive benefits in a cost-effective manner, while being able to leverage the scale of the company across the globe. A good benefits strategy also acknowledges and adjusts to local practices and cultural needs. Finally, employers are looking to ensure that the benefits they provide are valued by their employees, who represent a diverse population across the globe.

As you can see, both of the approaches mentioned have pros and cons, but most importantly, they do not provide a sustainable way to build a long-standing multinational employee benefits program. Luckily, there is a more advantageous option. Leveraging a captive can provide organizations with the ability to create a third kind of program structure, one which brings the positive aspects of the first two approaches and builds on them to create a framework that adds value to all stakeholders – employees, employer, local and international HR teams.

This approach allows for centralized decision making as it relates to carrier selection. Most of the clients we work with choose to select one or two multinational carriers, creating flexibility for local teams. Due to a stronger employer negotiating position, the centralized carrier selection process ensures lower rates and pricing across benefit lines and geographies. The transaction is structured such that the risk associated with benefits is ceded by the carriers to the employer’s captive, where it is pooled across all lines of coverage and countries. This creates greater stability for the program as a whole and limits the possible rate increases for programs and countries due to one bad claims year. Using the captive also provides employers with the ability to go beyond what local carriers will provide. Since the risk of the plan is with the captive, the carriers operate as third-party administrators (TPAs) and are usually willing to provide better coverage terms than under traditional fully insured plans.

In addition, in cases where employers are looking to go above and beyond to provide better than market benefits, the captive can help fund these elements at cost. For instance, we helped a major technology employer looking to provide HIV related coverage for its employees across the globe, and they were able to have the benefit be administered by the carriers on a local basis and pay for it through the captive. Without a captive, funding for this coverage might be difficult as local carriers may not know how to price this coverage or may not want to cover it under their plan design at all. In addition to HIV, mental and nervous related benefits along with fertility programs are other popular coverage employers like our client mentioned above are providing in this manner as many countries do not offer these benefits as part of their standard offerings, but they are benefits yielding an increasing employee interest.

From a local HR perspective, such a program provides some flexibility for carrier selection, while being able to control local plan offerings. The additional plan offerings which may not be provided on a local level create a huge value proposition, ensuring local HR buy-in for this program.

Captives and multinational benefits programs not only save money while providing better benefits, but they also provide a holistic view of the programs from a risk management perspective and lower the administrative burden. To recap, here are some advantages that make such a program extremely attractive:

Fill Gaps in Critical Coverage

Cultural norms and market availability play a huge role in what your employees across the globe want and what they can access. A benefit available in the US may not be available through commercial carriers in Brazil. A captive allows for customized coverage and can help even the playing field for your international employees. For instance, COVID-19 has heightened the need for covered mental health assistance as a component of a health plan. A lot of international plans do not provide this essential benefit. A captive is a cost-effective way of obtaining this coverage for all your employees.

Obtain Higher Limits

Using multinational pooling programs and captives allow employers to increase the coverage limits available to local employees. For instance, most carriers have filed local policies allowing for life insurance benefits of up to $5M in most countries. However, they offer guaranteed issue limits of around $500K in international markets. Using this approach, we have seen carriers increase guaranteed issue limits.

Improve Your Reporting

A captive allows the parent organization to be one step closer to claims and plan activity. With less intermediaries than a traditional insurance structure, a captive leads to greater transparency and faster access to data. As a result, captive owners have enhanced data management and tracking capabilities they can use to inform decisions in real-time. This way you can follow your investment closely and understand your return, or where changes need to be made. With a global workforce, this becomes critical.

Gain Flexibility

In traditional fully insured programs, there are limitations on the plan designs you can create. A captive creates an opportunity to customize your plans according to your unique workforce, and with a range of international needs, this will become even more valuable. COVID-19 has shed light on the importance of such flexibility, with organizations seeing changes in exposures and gaps they did not know existed.

Lessen Your Administrative Burden

By eliminating conflicts and engagements with local brokers, employers reduce the time spent on administration as these needs are met by a centralized team of support staff who have all your plan information and do not need to be brought up to speed on the cultural nuances of the programs and geographies. Also, captives eliminate the need for bidding exercises and negotiations on both the central and local levels. Due to the transparency of a captive program, there is almost no need for bidding of carriers to get lower pricing. The captive is capturing any surplus in pricing and using it to provide improved benefits to the employees.

Answer to a Hardening Market

Maintaining an international benefits program that is comparable in value across your diverse workforce is no small feat. With globalization, digitization and relocation on the rise, your employees are not siloed within their geography, and an integrated benefits program can serve to bring your employees together and improve your corporate culture. We have seen great success with multinational corporations moving toward a more centralized approach, where the same robust set of benefits can be offered to employees across the globe. By pairing this strategy with a captive, you can offer enhanced benefits, additional coverage and plan designs customized for your population, all while generating savings, improving your data and reporting, and “future-proofing” your benefits program. If you have questions about how to get started on harmonizing your international benefits, or aren’t convinced why you should, please get in touch.

Maintaining an international benefits program that is comparable in value across your diverse workforce is no small feat. With globalization, digitization and relocation on the rise, your employees are not siloed within their geography, and an integrated benefits program can serve to bring your employees together and improve your corporate culture. We have seen great success with multinational corporations moving toward a more centralized approach, where the same robust set of benefits can be offered to employees across the globe. By pairing this strategy with a captive, you can offer enhanced benefits, additional coverage and plan designs customized for your population, all while generating savings, improving your data and reporting, and “future-proofing” your benefits program. If you have questions about how to get started on harmonizing your international benefits, or aren’t convinced why you should, please get in touch.

According to SHRM, paid leave may have been 2020’s biggest workplace news. A number of U.S. companies (between 27% and 52% depending on the study) expanded their paid leave benefits, with paid parental leave growing at a faster pace than paid family care leave. The states and jurisdictions of California, Colorado, Connecticut, Massachusetts, New Jersey, New York, Oregon, Rhode Island, Washington, and Washington DC have passed paid family and medical leave (PFML) laws to date and at least another ten states are considering them. In addition, numerous localities have passed paid sick and safe leave laws. These can vary across cities and counties, even within a given state.

On a federal level, laws exist such as the Family and Medical Leave Act (FMLA), enacted in 1993, which affords unpaid job-protection, and programs such as the Fischer Tax Credit, the Federal Employee Paid Leave Act (FEPLA), and the Families First Coronavirus Response Act (FFCRA). Federal programs offer limited coverage as wage replacement and job protection may or may not be included in each law. A federal paid leave program is now seemingly supported by both democratic and republican parties, with the biggest difficulty being how to pay for it.

In addition, and to complement paid leave policies, more companies are offering and triggering EAP and wellness programs than they have in the past. About a fourth of companies say they provide a caregiver benefit, separate from EAP, that might include flexible work hours, personal time, counseling services, free programs for finding and managing care, employer subsidized online resources, child, or eldercare. You can read more about the landscape for caregiver benefits here.

- Where do the bulk of my employees work?

- What corporate disability, paid family and medical leave and sick or safe leave policies are they subject to?

- How are these plans being offered, administered, and paid for?

- To what extent do they coordinate or integrate with other leave of absence, workers’ compensation and sick or PTO policies? Or with broader health and wellbeing programs?

- To what degree can the process be centralized? Can current vendor partners be leveraged to streamline? Can tools be provided to simplify, educate, and personalize?

Taking these factors into account gives benefit professionals the opportunity to heighten the discussion with senior management, consider plan and policy design more holistically and determine administration that will minimize employee confusion, position managers for stronger engagement, and lead the organization towards better outcomes.

Sources:

Leave and Flexible Working Survey, SHRM Employee Benefits, 2019. Paid Time Off Survey, WorldatWork and PTO Inc., 2019. Integrated Disability, Absence and Health Management Survey, Spring Consulting Group, 2020.

Integrated Disability, Absence and Health Management Survey, Spring Consulting Group, 2020.

Data compiled by the Organization for Economic Cooperation and Development (OECD), 2018.

Paying the Way, Large Employers and the State Paid Leave Patchwork, The ERISA Industry Committee, 2020.

Paid Leave: Exploring the Impacts to Other Benefits Programs, Spring Consulting Group and ClaimVantage, 2020

As seen in Captive Insurance Company Reports (CICR)

For most companies today, its people are one of the largest investments its makes. COVID-19 accentuated this point and further showed us how the health of a company depends in large part on the health and wellbeing of its workforce. Providing competitive benefits is not just the right thing to do, but a sound business decision. Employee benefits usually account for one of the largest expense line items on an income statement for organizations. In a world where employee benefits consistently become both more important and more expensive, businesses of all types are looking for an affordable mechanism to finance these risks. One solution that has become central to discussions about employee benefits has been captive insurance.

To provide some background, a captive is an insurance or reinsurance company – which can help insure or reinsure the risks of its owners, the parent company (or companies).

Employee Benefits & Captives

Over the past decade as healthcare and benefit costs have been rising, captives have become the go-to solution for organizations looking to bend the healthcare cost curve as well as create a more efficient employee benefits program. More recently, however, organizations are recognizing the many qualitative advantages of a captive that can help attract and retain employees- a company’s most import asset. As we enter a new decade, these qualitative advantages or “soft costs” of human capital will drive the next iteration of captive insurance.

Traditionally, captives have been viewed as purely a funding mechanism for employee benefits that provides the following advantages:

- Improved cost savings

Cost savings can be yielded through: better control of premium costs, reduced frictional costs (commissions, taxes, insurer profit, administration), captured underwriting savings, earned investment returns, and improved cash flow for the parent organization.

- Improved risk management & increased control

- Enhanced reporting: Captive programs usually provide reporting in a more timely manner, allowing stakeholders to make decisions regarding potential plan design changes for the upcoming year.

- Centralized risk pool: From an organizational risk perspective, leveraging a captive allows risk managers to have a more complete understanding of the risks associated with the programs. Also, life and disability lines are usually considered to be third party risks and have a positive impact on the captive’s risk distribution.

- Non-correlated risk: Employee benefits usually add non-corelated risk for existing captive programs, thereby, reducing the risk exposure to the captive.

- Quantification of loss prevention programs and wellness initiatives: By utilizing a captive, the organization has the ability to implement data analytics programs that provide actionable insights on the effectiveness of existing programs and the current cost drivers.

- Design coverages and provisions for programs that are unique to the parent company: Every organization has a unique set of risks and captives can be used to fill in gaps in the existing benefit programs.

In our view, the next generation of captive insurance will have a sharper focus on the soft costs of human capital, such as:

- Intangible results

While employee benefits account for large costs for employers, they are running a significant risk by not providing the right benefits. By establishing a captive, employers can open doors to focus on human capital and the more qualitative aspects of a program. Further, a captive allows for customized benefits programs to meet the needs of your unique demographic. Employees a technology company will have different priorities and expectations than, for example, those that work in manufacturing. With a captive you can understand and meet those unique needs better than you could with a commercial carrier, in a cost-effective manner. This will go a long way with retention and engagement, and will make your employees feel their voices are heard.

Another intangible result of a captive program is the parent organization’s ability to capture enhanced data analytics. This data comes in months sooner than it would with a commercial carrier, meaning you can analyze your programs and make real-time decisions to yield better claims results. For example, if you know one of your biggest population health issues is diabetes, you can establish programs to address diabetes before your renewal is up. With commercial carriers, the information comes in too late to make changes for that plan year.

Which Benefits Can I Fund Through a Captive?

A wide range of employee benefits may be funded through a captive – the most common coverages are Medical, Life, Disability, Retiree Medical and Voluntary Benefits.

Captives can be used to fund Employee Retirement Income Security Act (ERISA), or non-ERISA benefits. ERISA benefits are primarily the benefit plans sponsored by and contributed to by employers. Life and Disability plans are usually ERISA in nature. These plans are subject to federal oversight, under the auspices of the Department of Labor (DOL) and require express approval from the DOL to fund them in a captive. Approval from the DOL is subject to meeting certain criteria – using an A rated fronting carrier, not paying any more than market rates for the coverages, no direct commissions as part of the contract, requirement for an indemnity contract, to name a few.

Medical stop-loss is usually not considered to be subject to ERISA and has become an extremely popular benefit to add to a captive. The reason for this has been two-fold. Firstly, the rising cost of catastrophic claims. Self-insured organizations are increasingly concerned about the financial impact of high-cost claims – unfortunately seeing $1M or $2M claims is becoming commonplace. One such large claim could have a material impact on the financial sustainability of the program. Second, the hardening insurance market is driving employers of all sizes towards a captive based stop-loss solution, as it reduces the opaqueness of the pricing process and helps employers get a much clearer understanding of their premiums and cost drivers. Usually a captive stop-loss program involves the employer creating an annual aggregate limit, and purchasing excess coverage from the commercial markets above the captive’s aggregate retention. Thereby, protecting the captive from most catastrophic claims.

Long-tail benefits such as group universal life insurance and long-term disability are ideal captive candidates. Benefits that pay out over multiple years (e.g. long-term disability and retiree medical), provide cash flow stability and loss predictability.

Using a captive for voluntary benefits has recently risen in popularity. This is a cost-efficient way of offering benefits that your employees can choose to participate in, or not. More and more employers are turning to this strategy as healthcare becomes more expensive, as a way to supplement benefits and lessen both their financial burden and the financial burden faced by their employees. One of the most attracting elements of writing voluntary benefits into your captive is that voluntary benefits typically have a very low loss ratio, which means they can generate a lot of savings within a captive. Those savings can then be leveraged to reduce premiums for employees or expand the coverage offered. An example of a prime voluntary benefit often offered in a captive structure is hospital indemnity, which can be critically helpful coverage, but one that is often otherwise too expensive to fund.

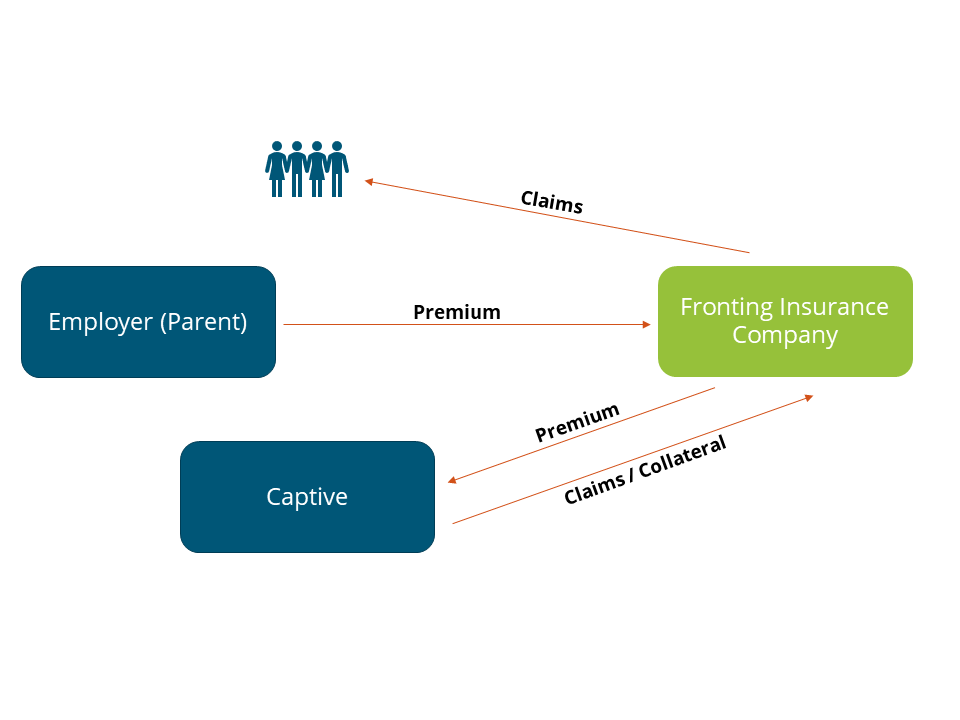

How it Works

Unlike property and casualty lines of coverage, employee benefit lines have a unique value proposition. They allow organizations to recapture dollars that would have otherwise gone to an insurance carrier. Both life and disability coverages use a fronted carrier, i.e. a commercial carrier stands in front of the captive so that from an employee perspective there is no change in the way they interact with the insurance company. On the back end, the carrier cedes risk and premiums to the captive.

The following illustrates how a typical fronted captive program works.

Under such an arrangement the fronting insurer to continue to administer the program. The employer pays the fronting insurer an annual fee for its services, allowing the captive to retain underwriting profit (if any) from the program. Depending on the risk appetite of the organization and the results of the actuarial modeling – the employer may choose to buy reinsurance for the program.

In Closing

The typical steps involved in adding benefits to an existing captive or forming a new captive are a feasibility study which outlines qualitative and quantitative factors for consideration, such as potential savings, program structures, design alternatives, insurance considerations, and implementation requirements.

Today those in the insurance industry are facing difficult circumstances on a variety of fronts. The recent pandemic has led to hardening of markets. We are seeing substantial rate increases for clients. Captives offer a solution to mitigate these increasing costs in a sustainable manner. In addition, captives provide access to additional data and insights that can help organizations get a clearer understanding of claims drivers and therefore allow for implementation of solutions and tools that reduce claim costs. Further, captives provide organizations the ability to impact the soft costs of human capital by identifying and crafting unique solutions to meet their employees’ needs, more important now as the pandemic shed light on gaps in coverage many did not realize existed.

Captives are useful and versatile risk financing tools, especially for employee benefits. They provide significantly better cash management than can be provided through a trust and can produce impressive cost savings as compared to fully insured guaranteed cost plans.

We hope we’ve piqued your interest and we’re here for you. Over the next months, we will dive further into employee benefits captives to cover things like types of captives, moving to a self-insured program, medical stop-loss, feasibility studies, solutions for small and mid-sized businesses and more. We hope you’ll keep reading.

“Why do I need a broker?” This is a question that surprisingly gets asked more than you would expect. In today’s society of consumerism, the internet, and “do it yourself” mentality, tied with the desire to save money, this is a valid question. I would ask in turn – would you go to court without legal representation? Of course not. It makes financial sense to use a broker as in most cases, you do not get charged for their services. Typically, brokers are paid by the insurance carrier, the one that you jointly decide best meets your needs as an employer. More importantly, brokers protect your best interests as an objective third party. There is no specific financial incentive for brokers to decide on one insurance provider over another.

An insurance broker acts as an intermediary between you and your insurer, lessening the administrative burden for you and negating the need for you to weed through complex policy jargon. We bring over 200 years of training and experience and our insurance know-how, and our goal is to always find a policy that best suits your coverage needs at the best possible price. Brokers do the shopping and analysis on your behalf, saving you the time of plodding through quotes from various carriers and trying to determine the optimal solution. We provide impartial advice based on the client’s unique situation.

Some of the benefits of using an insurance broker are:

- We listen to understand what you are trying to accomplish

- We search the entire marketplace looking for the best coverage at the most affordable price

- Once we find the ideal coverage, we review and discuss the cost, coverages, and exclusions with you in simple language so there are no misunderstandings

- We walk you through the appropriate paperwork and submit it on your behalf to the insurance company

- Once we have approval, we continually assist and advise you throughout the year to ensure you are getting the most from your plan

- We assist with issues like billing and claims questions

- We have compliance experts who will deal with issues like healthcare reform, paid family and medical leave and COVID-19 regulations, ensuring your policies pivot as necessary

- Come renewal time, we are there to negotiate for you and handle much of the legwork involved

These are very important considerations for you to take into account when deciding if a broker is right for you. The alternative is to spend a lot of your own time educating yourself, taking away valuable time from your day job and family. Insurance brokers go through strict educational and licensing requirements and have significant knowledge in the industry. Our deep understanding of your local market and the players involved ultimately yield enhanced, cost-effective coverage for you.

All that said, it’s important to note that not all brokers are the same. Some have specialized services and products or are focused on specific markets. For example, there are brokers with expertise in the property and casualty or life insurance areas but that just dabble in health insurance. Today some payroll companies are even offering employee benefit services as well but again, their bread and butter is payroll, not benefits. To offer an analogy – you would not go to a foot doctor to address a heart condition, so make sure your broker’s core competencies are the ones you need.

In summary, your insurance needs are best met by a broker who works for you and not by an insurance company, who have their own interests to look out for. Brokers yield more choices, usually at a much lower cost to you and your business. Unless you happen to be an expert in insurance plans, why risk the headache and lose the resources needed to do it on your own? Further, a consultative broker like Spring will take the time to truly understand your business so we can constantly be on the lookout for new and innovative solutions that will align with your objectives.

People are typically the largest investment a company makes. Taking care of those people through employee benefits is a niche area of your business, and you need an insurance broker who has the training and expertise necessary in today’s complicated and competitive marketplace. Spring’s approach to brokerage is collaborative and strategic, but we ultimately remove the legwork for you and ensure you have the best plan options available.

As Seen in the Captive Review Group Captive Report

Medical stop-loss coverage protects self-insured groups from catastrophic medical claims. Medical stop-loss has long been used as risk management tool by small- and medium-sized organizations to limit their exposure to medical claims above their desired retention levels. This strategy has been used by single parent programs as well as group captive programs.

The reason this strategy has been more popular in the mid-market is because of two primary reasons. First, businesses have wanted to insulate themselves from catastrophic claims risk, as one large claim could have a material impact on the financial sustainability of the program. Second, the relatively small size of the groups means greater variability from an actuarial perspective. In comparison, large companies have stronger balance sheets allowing them to take on a more aggressive risk management strategy and reduce third party spend with insurers.

As I write this in April of 2020, there are a myriad of unprecedented challenges facing both small and large employers and medical stop-loss can help mitigate some of these concerns. Recently, we have seen a shift in the market where large employers are increasingly becoming interested in reviewing the possibility of leveraging a captive to provide medical stop-loss coverage. I anticipate this trend to continue. Below are four points as to why.

As we stare towards the possibility of a recession and reduced economic output, poor investment income will have an adverse impact on insurance company financials.

Prabal Lakhanpal

- Hardening markets

This past renewal season, we saw that markets are starting to harden, and given the current Covid-19 pandemic and the financial and economic climate, this is bound to continue. A variety of factors have contributed to this including regulatory changes (ACA and healthcare reform) and many recent natural disasters (Hurricane Harvey, California wildfires, etc.). Insurers for a large part of the past decade have benefitted from the favorable financial markets world over, thereby reducing their need to increase rates to continue to make their target earnings per share (EPS).

As we stare towards the possibility of a recession and reduced economic output, poor investment income will have an adverse impact on insurance company financials. Further, as markets tighten, access to inexpensive cash is becoming harder. Since most insurance companies are public, the increased pressure to keep their share prices buoyant is going to result in them wanting to beat their expected EPS – which requires higher profit margins. Finally, as reserves balances diminish due to market conditions, principles of conservatism are going to require them to shore up financials, and the easiest way to do this is by increasing premiums.

These factors coupled with the ongoing pandemic, which will likely result in an increase in aggregate claims, led me to believe hardening insurance markets are upon us. This is likely to result in an increase to reinsurance costs for employers who are currently self-insured. A well-structured medical stop-loss solution can help employers navigate these market conditions by providing them greater control over the program and creating an alternate avenue for reinsurance.

Hardening markets make captives more favorable, as they allow for customized coverage otherwise unavailable in the commercial market. Employers currently using captives have been provided an opportunity to leverage the captive program to fund for Covid-19-related expenses. For non-captive employers, this impact is felt directly on their financial statements.

- Cashflow volatility due to higher claims costs

Claims costs have been increasing at an aggressive pace. The US has long been criticized for poor population health management, with rising chronic conditions like diabetes that are expensive to treat. In addition, the pricey cost of medication has made extremely high cost claims a reality of healthcare. Claims in excess of $1m are becoming commonplace. For large employers, who are traditionally self-insured, such claims cause volatility from a cashflow perspective, making it harder for finance teams to budget and build expected proformas. Using a medical stop-loss program eliminates this volatility as claims above the self-insured retention level are funded in the captive, creating a level funded premium plan.

- Upwards healthcare trend

According to studies by PwC, while medical cost trend has been flat for a couple years, it is expected to increase from 5.7% to 6% in 2020. This rise in healthcare costs is attributable to an increase in the utilization rates. Medical trend increases are outpacing those of inflation, which was 2.07% in 2018 and 1.55% in 2019.

As a result, employers have had to leverage solutions such as high deductible health plans and other forms of cost sharing to bend the healthcare cost curve. The crux of the issue is that now organizations are having to combat both rising medical trends as well as increasing claims costs, while still needing to retain talent and provide competitive benefits.

A well-crafted medical stop-loss solution can help ease the burden for employers and provide them a sustainable way to bend the healthcare cost curve. Development of a formal reserve mechanism is an efficient way for employers to set aside dollars to mitigate large cost increases in the future. While an employer cannot control what happens in the insurance and healthcare markets, they can make the decision to put themselves in a position to be able to navigate the landscape more efficiently. We are seeing an increasing number of CFOs drive conversations around better managing employee benefits spend as it is becoming one of the largest expense items for organizations.

- Control

By writing stop-loss into a captive, an employer can leverage captive savings to focus on initiatives most useful for its employee demographic. We have seen employers use the captive savings for wellbeing initiatives as well as cost control programs focused on disease management for conditions like diabetes or musculoskeletal problems. This kind of structure can then be tied with programs dedicated to population health management, wellness and health advocacy for a robust, employee-first package aimed at gradually reducing claims costs.

Using a captive provides employers access to data in a timely manner, allowing them to better analyze and review drivers of claims, in turn providing them an opportunity to implement measures that would focus on addressing those drivers. While this is possible without a captive, we have seen employers are more engaged when using a captive — meaning they are more likely to create a structured approach to claims and cost management leveraging the captive. In my view, this is because of lack of funds for such initiatives and the lack of a structured risk framework in some cases. Using a captive to underwrite medical stop-loss addresses both of these aspects.

Transparency is one of the core benefits of a captive. Once organizations begin to use a captive funding solution for its medical spend, they usually begin to expand their horizons for other cost reduction initiatives. One such initiative has been carving out drugs (Rx). Using a pharmacy benefit management (PBM) solution can generate additional savings ranging between 15% to 30% of Rx spend. These savings are in addition to those that an employer may recognize by restructuring their funding approach. Further, these savings have a multi layered benefit, reducing the overall medical trend and generating additional reserves for the program to offset possible cost increases in the future.

In general, large employers are more accustomed to customization and retaining control, so a captive program for medical stop-loss aligns with their needs and enhances their ability to control their healthcare programs. Better data analytics and understanding of claims also provides employers the ability to be more reactive and make necessary changes quickly, in a much more agile setup. A captive provides monthly and quarterly reports which are usually much more detailed and timelier than those provided by a commercial insurer. Finally, adding additional risk to the captive also helps the risk managers develop a more comprehensive understanding of enterprise risk at large.

Conclusion

Medical stop-loss coverage in a captive continues to be a prudent business strategy for companies of all types and sizes. It creates multi-layered protection. Large employers are beginning to realize the attractiveness of such a program, whose advantages have been especially highlighted lately due to market and global economic shifts and conditions.