Captive International has released the winners for the 2024 US Awards. Spring is proud to announce that our team has been recognized among the best in the industry for Top Feasibility Study (Firm), Top Feasibility Study (Individual) and Top Captive Consultant (Individual). You can access the full list of winners here.

Regardless of the specific line of coverage, claim audits are a best practice for employers and plan sponsors to ensure accuracy, identify errors, and document process gaps. A comprehensive claims audit can uncover issues related to compliance, adherence to contractual provisions, and consistency with best practices.

While most employers and plan sponsors understand the value of a claim audit, it is common to struggle with knowing where to start, and more specifically, when to start. For clients looking to audit their disability claims, we recommend considering the following factors in determining an optimal timeframe:

1. Vendor Implementation

If you are implementing your fully-insured disability plan with a new carrier or your self-funded disability plan or program with a new claim administrator, conducting a claim audit after the go live date can ensure that:

- Workflows established during implementation are being properly followed

- The vendor is correctly managing claims through the entire claim cycle

- Any areas where additional training or communication would be beneficial are flagged

Conducting a claim audit post-vendor implementation can help solidify the foundation for the relationship and serve to identify opportunities for improvement before they grow into more significant roadblocks as the volume of claims increases.

2. Renewal & Stewardship

Whether you have a vendor administering your self-funded disability plan or program or a carrier insuring your fully-insured plan, it may make sense to conduct a claim audit in anticipation of your renewal, allowing you greater insight into:

- Any process or performance issues that need to be addressed

- The financial implications of any findings of non-conformance

- Whether any performance guarantee should be added as part of the renewal negotiation to address a specific area of concern identified by the audit

As your team comes to the table to advocate for a fair renewal, audit findings can be a powerful negotiation tool. They can be used not only to position your organization for a more favorable renewal, but also as leverage to correct those findings that have had a negative impact on the plan or program’s financials and/or your employees’ experience.

3. Compliance

When determining the right time for a disability claim audit, if your plan is subject to The Employee Retirement Income Security Act (ERISA), your fiduciary duties may drive your decision to conduct an audit. As the plan sponsor, your organization is a fiduciary and must act prudently. An audit is one way to fulfill your fiduciary duty to act prudently as it not only monitors your vendor’s performance, but also ensures that the plan is in compliance with ERISA, the Internal Revenue Code, and other applicable laws.

4. Trend

Most employers receive some type of regular reporting and claims analysis from their vendor partners. When considering a claim audit, pay close attention to the data you are receiving, and consider setting things in motion if your plan or program’s experience is yielding an unexpected or new trend. In doing so, the claim audit can:

- Validate whether the trend is real and/or significant

- Identify the root cause of the shift in trend to inform potential strategies for mitigation or reversal

5. Self-Funded, Self-Administered

If you have a self-funded disability plan or program which you manage inhouse, you may want to consider establishing a routine cadence for conducting an audit of your team’s claim handling to:

- Validate that insourcing is still the right path for your organization

- Determine if there are any areas of opportunity for improvement and efficiency

- Confirm that your workflows and controls are being properly followed and applied

- Identify if there are any compliance issues

Conclusion

Disability claim audits should be one tool in an employer’s toolbox for ensuring compliance, vendor and internal performance, and an overall positive claim experience for your employees. In conducting a claim audit, employers need to determine stakeholders involved, resources (internal or external), data gathering methods, goals, and processes. While the ideal time may vary by employer, the question of when to conduct the audit is another integral component of your claim audit strategy and should not be overlooked.

If you are interested in conducting a claims audit but need guidance or an objective partner to assist, please get in touch with the Spring team.

Spotlight on Cancer Point Solutions: Supporting Employees with Targeted Innovations

In today’s rapidly evolving healthcare landscape, cancer remains one of the most complex and challenging conditions to treat and is a top cost driver for many employers, including colleges and universities. Thankfully, advancements in cancer care are offering hope and transforming patient outcomes. One of the most promising developments is the rise of cancer point solutions, which aim to address the specific needs of cancer patients through targeted interventions and comprehensive care models.

What Are Cancer Point Solutions?

Cancer point solutions are specialized programs or services designed to address key aspects of cancer care, from prevention and diagnosis to treatment and survivorship. These solutions often combine cutting-edge technology, personalized care, and multi-disciplinary approaches to improve patient outcomes and enhance the overall healthcare experience.

Why Are They Important?

Traditional cancer treatment often involves navigating a fragmented system of specialists, treatments, and services. Cancer point solutions are designed to streamline these touchpoints by offering a holistic approach that integrates various aspects of care. These areas may include:

- Early Detection and Screening: Advanced diagnostic tools and AI-driven screening methods improve the chances of detecting cancer at its earliest, most treatable stages.

- Personalized Treatment Plans: Leveraging genetic testing and precision medicine, cancer point solutions can tailor treatments to the unique genetic profile of each patient, improving efficacy and reducing side effects.

- Patient Support and Navigation: Dedicated care teams, including patient navigators, help guide individuals through their cancer journey, ensuring they receive timely care, emotional support, and access to necessary resources.

- Holistic Care Models: Integrating mental health, nutrition, and survivorship programs helps address the broader impacts of cancer, providing patients and their loved ones with the comprehensive support they need for both physical and emotional recovery.

Benefits to Patients and Providers

Cancer point solutions offer several advantages to both patients and healthcare providers:

- Improved Patient Outcomes: By leveraging innovative treatments and technology, cancer point solutions can lead to more successful outcomes, fewer hospital readmissions, and improved quality of life for patients.

- Cost-Efficiency: Early detection, personalized treatments, and streamlined care processes can reduce unnecessary treatments and hospital visits, ultimately lowering overall healthcare costs.

- Enhanced Care Coordination: With all aspects of cancer care integrated under one solution, providers can collaborate more effectively, reducing the risk of miscommunication and errors in treatment and improving the patient experience.

How Cancer Point Solutions Are Shaping the Future

As healthcare systems continue to adopt value-based care models, cancer point solutions may play an increasingly important role in optimizing care delivery. By focusing on both clinical and holistic outcomes, these solutions not only enhance patient care but also align with broader goals of improving efficiency and contributes to a holistic employee benefit model to support employees at various points in their lives.

Conclusion

While many cancer patients may have access to certain benefits through their providers and care teams, providing additional support through an employee benefit solution can give employees seeking care or caregivers supporting their family members additional resources and tools during a difficult time. By embracing these innovative models within a benefits program, employers can help their employees access more personalized, coordinated, and effective care, ultimately improving the lives of those affected by cancer and positively impacting organizational population health.

For more information on how our health and welfare consulting team can help you implement or optimize cancer point solutions within your organization, please contact us today.

1 https://www.ncbi.nlm.nih.gov/pmc/articles/PMC8634312/

2 https://www.cancer.org/#:~:text=The%20American%20Cancer%20Society%20offers,patients%2C%20families%2C%20and%20caregivers

3 Improving Modern Cancer Care Through Information Technology

4 Patient-Centered Cancer Treatment Planning: Improving the Quality of Oncology Care. Summary of an Institute of Medicine Workshop

Workforce populations tend to be diverse in terms of demographics as well as other factors such as geography. This is one of the primary reasons healthcare programs are aligned with and sponsored by employers. These programs aim to achieve high enrollment to accommodate the demographic diversity among members. This, in turn, creates a system where the highest utilizers are subsidized by the leanest. There are several typical drivers that affect utilization: age, gender, morbidity, family size, etc. For mature populations participating in employer-sponsored healthcare programs, new hires with more favorable demographic characteristics help offset rising costs for aging employees, providing a consistent balance between those subsidizing and those being subsidized.

One of the largest demographic drivers of cost is age. As age increases, so do costs. When a population has aging members staying on well beyond 65, it becomes difficult to maintain the same influx of younger members to offset these rising costs. There are many industries where employees tend to work beyond age 65, such as education, public administration, and real estate. Additionally, due to rising retirement costs and increases in the cost of living, it has become necessary for many individuals to work beyond the traditional retirement age. The result is an average age that dramatically increases over time and average plan costs that outpace already burdensome medical and pharmacy trend rates.

How can we control these ongoing costs?

In general, there are many levers typically used to control healthcare costs. Many of them still make sense in the present environment, though they may be unattractive in a competitive employment situation. Examples include increased employee cost-sharing, leaner healthcare offerings, more stringent participation requirements, disease management, utilization management, and leaner pharmacy formularies.

How can we specifically address older members?

In the case of consistently increasing average age, these cost-control approaches may be temporary and insufficient. Further steps may include such approaches, but employers may also seek to decrease the number of older members remaining enrolled in the plan. Some specific suggestions include:

- Salary-banded employee contributions – This involves charging scaled contributions to members based on salary ranges. While this will not directly address older members, they tend to have higher salaries.

- Enrollment in Medicare – Increased Medicare enrollment could significantly mitigate post-65 costs. One potential approach, though often considered unattractive, is to move to a leaner pharmacy benefit for the active plan. If the pharmacy benefit is not as generous as contemporary Medicare Part D benefits, Medicare-eligible members will have to enroll in Medicare or pay a scaled penalty when they eventually do register, based on the number of months they were not enrolled.

- Offer an active stipend or payout – Some employers offer an annual or monthly stipend for not enrolling in an employer-sponsored plan, which may encourage members to seek coverage elsewhere. It could also make sense to offer a one-time lump-sum payout to help partially cover some of the estimated $165,000 (per Fidelity1) per individual for post-retirement healthcare costs.

- Offer post-retirement medical – One reason members remain in the workforce into later years is the challenge of acquiring and affording medical benefits after retirement. A post-retirement medical benefit is a large and expensive undertaking, but there can be more controllable mechanisms that limit costs to predictable amounts. A specific example is a defined contribution-type plan, where an explicit subsidy helps offset ongoing costs. This can be based on various factors to yield a predictable set of costs.

In summary, mitigating the increase in medical and pharmacy costs over time is already a significant challenge for employers, and aging populations can exacerbate these increases. It’s important for employers to address these issues head-on or face financial headwinds that could impact their stability. Please reach out to our team to explore these solutions further.

In recent years, a new term, carewashing, has emerged in discussions about workplace culture and employee benefits. The concept reflects a growing concern that companies are superficially adopting caring practices and policies—often as part of their branding—without genuine commitment. Modern employers aiming to foster authentic and supportive workplace environments should reflect on this term and how it relates to their positioning with their external clients as well as their employees.

When we shine a spotlight on employee benefits, carewashing refers to the practice of companies presenting themselves as caring and employee-focused, without implementing substantial, changes that truly benefit employees. In some instances, employers may implement meaningful programs, but since employees are unable to take advantage of them due to cultural limitations they are still viewed as carewashing. For example, a company might promote its new mental health day policy or wellness app extensively but fail to address systemic issues like excessive workloads, inadequate mental health resources, or poor management practices. The result is a veneer of care that can mislead both current and prospective employees about the organization’s true commitment to well-being.

It is imperative that organizations work to combat carewashing because of the impacts it can have on the business, employees, and their families.

- Genuine care and support for employees are critical for building trust and engagement. According to Gallup, organizations that show true commitment to their employees’ well-being experience higher levels of engagement and lower turnover rates1

- When employees recognize that initiatives are merely cosmetic, McKinsey & Company indicates it can not only lead to disengagement and turnover, but reduced productivity as well

- Negative perceptions about carewashing can damage a company’s reputation, making it harder to retain and attract top talent. A Harvard Business Review article highlights that companies perceived as inauthentic in their employee care practices can face significant reputational damage

- Although on the surface carewashing is not illegal, it could lead to legal risks (e.g., promoting care but not giving adequate support) and certainly presents ethical concerns

To mitigate the risk, employers must self-reflect and talk openly about their approach to employee benefits, ensuring their programs reflect their culture and vice versa. In some instances, offering programs without cultural support may do more harm than good. Using these guiding principles will go a long way to reduce the risk of carewashing:

- Set a holistic approach considering mental, physical and financial health

- Focus on implementing highly effective programs, invest in understanding the impact and align solutions with employee needs while considering business impact (positive and negative)

- Involve front line managers in roll-out campaigns to convey the importance of the program, understand their concerns and work together to find solutions

- Work toward a culture of caring that includes training and advocacy. If that is not possible in your organization, pinpoint solutions that can be genuinely adopted, appreciated and accepted

- Be transparent; every organization is unique. It’s better to make incremental, successful change than provide an offering that provides little to no value to employees and creates reputational risk for the organization

Although the terminology will change, any program design that undermines the trust of employees or clients will lead to disengagement and dissatisfaction. Make sure the programs you implement within your benefit offering do not mislead employees. Employees often tap into employee benefit programs during some of the direst times in their lives; nobody wants to feel carewashed when what they really need in that moment is care.

If you could use objective guidance on building and prioritizing realistic benefits initiatives, or evaluating your current state for carewashing red flags, please get in touch with our team.

1 Witters, Dan. “Showing That You Care About Employee Wellbeing.” GALLUP. https://www.gallup.com/workplace/391739/showing-care-employee-wellbeing.aspx

In August 2022, the Inflation Reduction Act (IRA, P.L. 117-169) was signed into law, bringing significant changes to Medicare. The law expands benefits, reduces drug costs, and improves the sustainability of the program, providing meaningful financial relief to millions of Medicare beneficiaries by enhancing access to affordable treatments1.

For the first time, Medicare now has the authority to directly negotiate the prices of certain high-cost, single-source drugs that lack generic or biosimilar competition. This groundbreaking provision is designed to help control costs and ease the financial burden on both the program and its participants.

Medications Selected for Price Negotiation

The Centers for Medicare & Medicaid Services (CMS) identified the initial group of drugs for negotiation based on multiple criteria, including the drug’s cost and the number of Medicare Part D enrollees currently using them. CMS engaged in direct negotiations with drug manufacturers to secure lower prices for some of the most expensive brand-name medications.

This negotiation process includes CMS presenting a final offer to the manufacturer, which can either accept or reject the proposal. The outcome? CMS and participating manufacturers have finalized pricing agreements, with Maximum Fair Prices (MFP) for ten selected drugs set to take effect on January 1, 20261,4.

This initiative is part of a broader, multi-year effort. By February 2025, CMS will select up to 15 additional drugs covered under Medicare Part D for negotiation, with new prices projected to be implemented in 2027. Another 15 drugs will be chosen in 2028, and an additional 20 the following year, expanding the reach of negotiated price reductions as required by the IRA4.

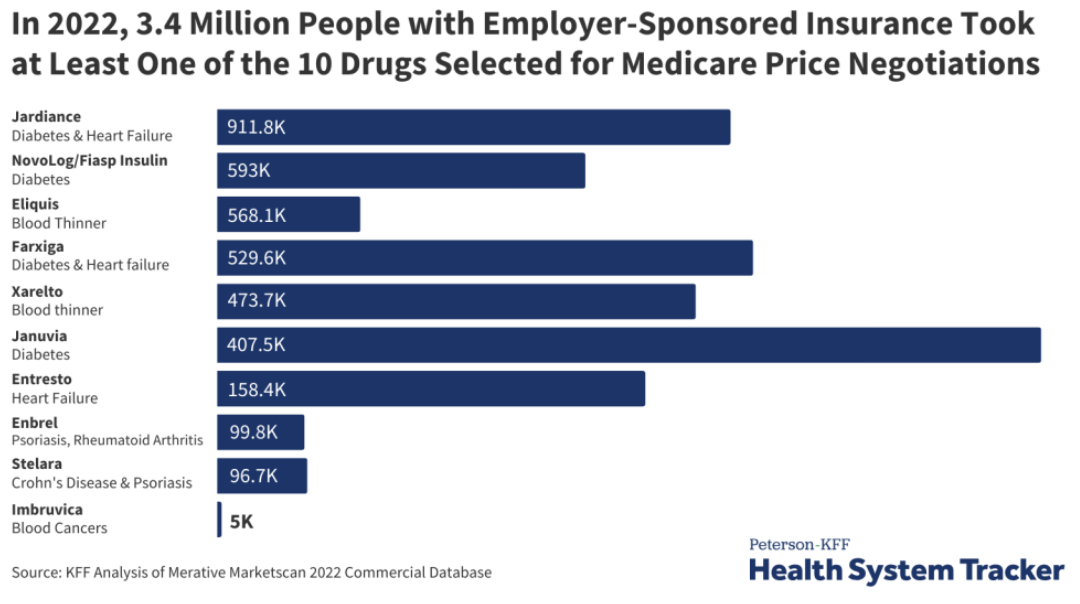

Although the Medicare drug price negotiations don’t apply to private insurance, 3.4 million people with employer coverage take at least one of the selected drugs. The ten medications are listed in the below graph3.

How Does This Affect Commercial Insurance?

Although these Medicare negotiations do not directly apply to private insurance, they could still have ripple effects on commercial drug pricing. Currently, 3.4 million people with employer-sponsored coverage use at least one of the drugs selected for negotiation3.

The impact on commercial insurance remains uncertain. Some experts suggest that lower Medicare prices could result in higher costs for private insurers as manufacturers look to recoup losses. Conversely, others believe that the negotiated Medicare prices could serve as a benchmark, potentially leading to lower prices in the private sector as well3.

While it’s too early to tell how private insurance will be affected, the ongoing Medicare drug price negotiations will be a closely watched development in the healthcare landscape.

To stay updated on this topic and learn more, click here.

1 Negotiating for lower drug prices works, saves billions. CMS. August 15, 2024. Accessed September 13, 2024. https://www.cms.gov/newsroom/press-releases/negotiating-lower-drug-prices-works-saves-billions

2 https://www.ajmc.com/view/lower-drug-prices-announced-under-medicare-negotiation-program

3 https://www.kff.org/medicare/issue-brief/explaining-the-prescription-drug-provisions-in-the-inflation-reduction-act/

4 https://www.cms.gov/inflation-reduction-act-and-medicare#:~:text=The%20Inflation%20Reduction%20Act%20makes,and%20limiting%20increases%20in%20prices

As Vermont was named the largest captive domicile globally in 2022, it has developed into a hub for alternative risk financing and insurance innovations. The Vermont Captive Insurance Association (VCIA) recently hosted its 2024 Annual Conference, a beacon in the captive insurance industry. This year’s conference, held in the heart of Vermont (Burlington), offered a dynamic platform for industry professionals to delve into the evolving landscape of captive insurance. From exploring the fundamentals of captive formation to addressing the pressing challenges posed by emerging technologies and regulatory changes, the conference provided invaluable insights and strategies. Attendees had the opportunity to engage with thought leaders, share best practices, and discover innovative solutions that will shape the future of the industry.

1) Captive Formation and Feasibility

Since Vermont is the most popular domicile globally, VCIA provides a great avenue to help first-time employers explore potential captive endeavors. Understanding the basics of captive formation and testing for feasibility is essential for anyone looking to establish or manage a captive insurance company. Here are some related sessions that caught my eye:

-The opening session, “Captive Immersion: Feeling Puzzled? Let’s Piece It Together,” brought together various stakeholders, including an attorney, underwriter, actuary, consultant and a state official to give piece-by-piece instructions on entering the captive industry.

– The presentation, “The Economic Landscape & Your Captive’s Investment Portfolio,” reviewed the current state of the economy and macroeconomic factors that may influence investment gains in a captive.

2) Emerging Technologies and Innovation

As the risk landscape evolves rapidly, captives must adapt to emerging tools and technologies. Addressing emerging risks such as cyber threats and leveraging innovations like AI and data analytics are vital for maintaining relevance and effectiveness in risk management, ensuring captives can proactively manage and mitigate modern challenges. These presentations spotlighted the need for alternative solutions to address emerging (and at times unforeseen) risks:

– The Cost of Compliance: ADA/FMLA Court Cases and Jury Verdicts offered a deep dive into recent legal cases, providing lessons on how to avoid costly compliance mistakes.

– The presentation, “Your Data Reimagined! A Captive Case for Data Visualization,” showcased how employers can utilize data visualization to help interpret large data sets and areas for risk optimization.

3) Regulatory and Compliance Updates

Navigating the complex regulatory environment and staying updated on captive taxation and oversight changes are crucial for compliance and strategic planning. It is essential that captive managers and owners are informed about regulatory requirements and can adapt their practices to remain in good standing and avoid potential legal pitfalls. Some insightful sessions include:

– Our VP, TJ Scherer, teamed up with the State of VT’s Dan Patterson in an open discussion group to chat about “Upcoming Changes in Regulation Oversight” and what captive owners in VT should keep their eyes out for.

– Four tax experts convened to discuss “Captive Taxation: What’s New & What’s Next.” They reviewed recent IRS, federal and state updates and discussed how companies can best prepare for an IRS audit.

4) Passing the Torch

Energizing new leaders and providing growth opportunities for newcomers are essential for the long-term sustainability of the captive insurance industry. By fostering new leadership, organizations can drive future success and address the ongoing challenge of talent shortages. These topics focused on the importance of developing talent to ensure that fresh perspectives and innovative ideas are woven into the industry:

– State of VT’s Chief Examiner, Heidi Rabtoy’s “Discussion Group: Attracting & Energizing New Leaders” spotlighted the current talent shortage in the insurance space, and tips to attract and retain next-generation industry leaders.

– One of my favorite parts of VCIA is the Newcomers’ Orientation; ensuring first-time attendees are educated and feel welcome is essential to the industry’s future success.

The enthusiasm and forward-thinking discussions from this year’s conference left a lasting impact on the captive insurance landscape. The conference highlighted the importance of understanding the fundamentals of captive formation and staying ahead of emerging risks, underscoring the critical need for compliance amidst shifting regulations. Moreover, the focus on cultivating new leadership promises a vibrant future for the industry. By harnessing the knowledge and connections gained at VCIA, risk professionals are well-equipped to navigate the complexities ahead and drive continued success in the world of captive insurance.

In a recent podcast from the International Risk Management Institute (IRMI), or Chief P&C Actuary, Peter Johnson gives an inside view into the actuarial methodologies that go into calculating loss development patterns and optimizing risk management strategies across long-tail lines. You can find the full podcast episode here.

As summer winds down, the Disability Management Employer Coalition (DMEC) hosted its 2024 Annual Conference in the energetic city of Nashville, TN. Known for its rich musical heritage, Nashville provided a lively backdrop for this year’s event, bringing together professionals from across the absence management spectrum to discuss the latest trends, challenges, and best practices. Here are some key highlights from the conference.

1) The Future of Paid Family and Medical Leave (PFML)

The focus on mental health remains prevalent as organizations continue to find innovative ways to support employee well-being. This year’s conference offered valuable insights into how mental health is evolving in the benefits industry:

-The session The Importance of a Guided Claim Experience emphasized the need for compassionate and informed support during the claims process, which can significantly impact employee well-being.

– I was joined by a group of leave solution leaders to examine findings from a recent leave report which looked at various factors including recruitment, retention, productivity, moral, and more with a focus on how successful employers are addressing leave managementns on benefits spend and workplace culture.

– One of the catchiest presentations, Walk, Crawl, Run: The PWFA Turns One, reflected on the one-year anniversary of the Pregnancy Workers Fairness Act (PWFA) and best practices for HR teams to stay compliant.

2) ADA/FMLA Compliance Updates

Navigating the complex web of federal, state, and local regulations remains a critical challenge for employers. This year’s sessions provided valuable guidance on staying compliant while managing diverse and geographically dispersed workforces:

– The Cost of Compliance: ADA/FMLA Court Cases and Jury Verdicts offered a deep dive into recent legal cases, providing lessons on how to avoid costly compliance mistakes.

– The ADA Compliance Mini Boot Camp led by Rachel Shaw was a must-attend for anyone looking to deepen their understanding of ADA requirements and refine their compliance strategies. This workshop was instrumental in equipping participants with tools to tackle common challenges and elevate their programs.

– I led a workshop with Baystate Health’s Manager of Disability and Leave, Lauren McCormick, in a session titled A Step-by-Step Guide to Refining Your ADA Strategy. In an interactive format, the session provided participants an opportunity to address real-life ADA scenarios and how to best address each individual case using a methodical process.

3) Telework Accommodations

As companies continue to navigate the post-pandemic landscape, finding the right balance between remote work and returning to the office is top of mind. The conference sessions provided practical insights into managing this transition effectively:

– The session “You Can Have Paid Leave AND a Productive Workforce. Here is the Secret Sauce.” explored how flexible work arrangements can coexist with robust paid leave policies to enhance employee satisfaction and productivity.

– Council from Reliance Matrix explained how many employers are quick to provide leave of absence to workers with a medical condition, whereas many alternative compliant leave options exist in their presentation, Encouraging Employees to Stay at Work or Return to Work.

–Another eye-catching session, We Goofed. Now What? An Accommodations Tale, brought light to a common scenario in which an employer fails to provide adequate accommodations under the ADA and/or PWFA; as well as best practices to address said employees’ needs.

4) Tech/AI’s Role in Absence Management

Technology continues to play a transformative role in the absence and disability management space, offering new ways to streamline processes and improve decision-making:

– Spring’s in-house attorney, Lynne Noel, together withPatagonia’s Senior Manager, Leave of Absence, Lauren Shipper, discussed Using Benchmarking to Refresh Your Program. They highlighted the importance of leveraging data to stay competitive and refine absence management programs. Insights provided actionable strategies for using benchmarking as a tool for continuous improvement.

– A group of data analytic experts explained the practical parameters of AI solutions in claims processes and the upsides and dangers to implementing AI systems in their presentation, The Transformation: How AI is Enhancing Analytics and Optimizing Decision-Making.

– During the session, The Future of AI in Leave and Disability Management, three leave and disability administrators discussed the current state of AI in the industry and how it can help streamline processes and improve employee satisfaction.

Final Thoughts

The DMEC 2024 Annual Conference in Nashville was a resounding success, filled with opportunities to learn, connect, and share best practices. From deep dives into compliance and mental health to exploring the latest technological innovations, the conference offered something for everyone. As always, it was a pleasure to reconnect with industry leaders and bring back fresh ideas to enhance our consultative offerings. We’re already looking forward to what next year’s conference will bring!