The Captive Insurance Companies Association (CICA) has announced that Mary Ellen Moriarty will become the new chair of CICA, and our Senior Vice President will take on the role of secretary/treasurer. You can find Captive International’s full article here.

The Captive Insurance Companies Association has announced that Mary Ellen Moriarty will become the new chair of CICA, and our Senior Vice President will take on the role of secretary/treasurer. You can find Captive Review’s full article here.

Title:

Director of Marketing

Joined Spring:

I joined Spring in March 2017.

Where are You From?:

I’m a Boston native! I grew up just south of the city in Quincy. I moved to Maine in 2020.

At Work Responsibilities:

I provide strategic direction and oversight of all of Spring’s marketing, with a focus on content, email communications, digital, events and sponsorships, and proposal writing.

Outside of Work Hobbies/Interests:

I’m a huge bookworm and like writing too. I also do kickboxing and ski in the winter.

Fun Fact:

I did figure skating as a kid.

Describe Spring in 3 Words:

People. Growth. Dynamic.

Favorite Place Visited:

Byron Bay, Australia

Favorite Band/Musician:

The Avett Brothers, The Head and the Heart, The Lumineers, Hozier.

Pets:

I have a 4 year old black lab named Patsy who is the best!

Unfortunately, news of rising healthcare costs seems less like news and more like the norm. In the last two years, we saw medical cost trend level out a bit, but it’s projected to spike back up. According to a recent survey by PwC’s Health Research Institute, the projected medical trend for 2024 is around 7% year over year, about the same as it was for 2021 and higher than both 2022 and 2023. Other sources predicted an even higher trend, coming in around the 8% – 9% range. Much of the cost burden falls on employees. The Kaiser Family Foundation reports that employees will pay an average of $6,575 for their health plan on a family basis, and around $1,400 for single coverage.

Cost Drivers

What’s behind the increase? There are a range of factors working behind the scenes here, most notably:

- Specialty drug and pharmacy costs. This is perhaps the biggest pain point when we think about overall healthcare costs, with specialty drugs or cell/gene therapy drugs seeing double-digit price increases year over year. The influx of demand for weight loss medications is a significant factor.

- Inflation. While the worst of inflation this go-around might have come and gone, inflationary impacts are typically delayed in the healthcare sector due to the lengths of contracts. This means that provider costs have risen, and that dynamic is playing out in the price of care.

- Healthcare worker shortage. The U.S. Bureau of Labor Statistics projects a need for 1.1 million new registered nurses across the U.S., and an Association of American Medical Colleges report projects a shortage of between 54,100 and 139,000 physicians by 2033.

- The worker shortage is further heightened by the next cost driver: increased utilization. As we finally stave off the extreme effects of COVID-19, healthcare consumers are back in a way they haven’t been since pre-pandemic. According to the International Foundation of Employee Benefit Plans (IFEBP), much of this uptick in utilization is due to chronic conditions.

- Catastrophic claims. IFEBP reports that catastrophic claims are responsible for nearly 20% of cost increases.

It is our job as health and welfare consultants to help employers navigate this landscape and identify solutions that can address the cost curve.

Combative Strategies

In such a difficult environment, it’s important to discern any tactics you can take to establish more control over your plans and create a sustainable program that works better for your organization and your employees. Here are a few of the strategies we typically evaluate on behalf of our clients:

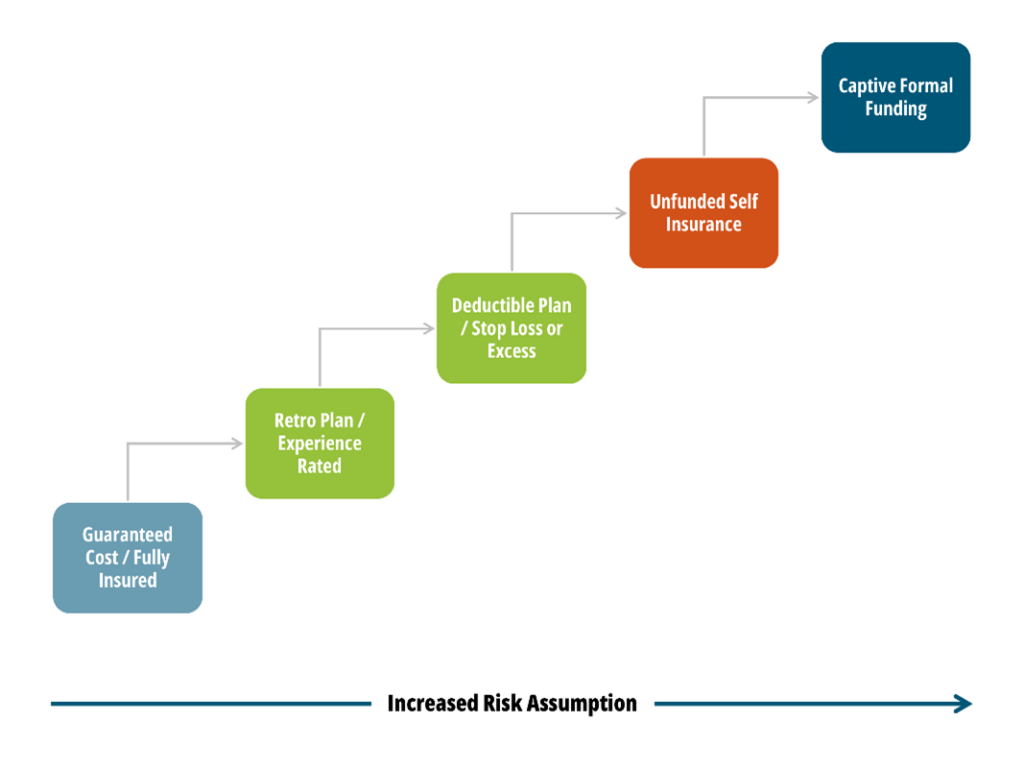

- Alternative funding. By considering an alternative risk financing vehicle like captive insurance, employers can expect to save between 10% and 30% on costs in the long run. However, a range of self-insured models exist for organizations lacking the risk appetite for a single parent captive. This is a trend that has caught on. IFEBP reported that 79% of employers surveyed are self-insured. A captive or similar solution is even more powerful if paired with stop-loss insurance, which can protect against those catastrophic claims we mentioned above.

- Pharmacy benefits strategy evaluation. With the staggering prescription drug prices we are seeing, it is imperative that you ensure your Pharmacy Benefit Manager (PBM) is truly working on your behalf by considering a PBM audit, contract review, or market check. In addition, make sure that you have protocols in place for utilization control, like prior authorization. We also work with clients to improve plan design, utilize clinical programs geared toward population health goals, and dig into data to make informed decisions around possible solutions, whether they be formulary changes, point solutions, or something else.

- Wellbeing. Often overlooked as a buzzword, wellbeing programs can have an impact on your bottom line. To yield results, it’s important to be targeted toward workforce demographics, ensure you can measure success, and that employee engagement is maximized.

- Plan design. It may be time to reevaluate items like cost-sharing (high deductible health plans, copays, etc.), dependent eligibility, the inclusion of telemedicine and mental health, and more.

At Spring, we work across four main pillars: plan design, process, technology, and funding while leveraging benchmarks to look comprehensively across clients’ programs and identify areas for improvement. If you could use objective guidance on how your organization might be able to better manage rising healthcare costs, please get in touch.

As societal norms and workplace attitudes continue to shift, the property and casualty (P&C) insurance space has been significantly impacted by a phenomenon known as social inflation. This trend has presented challenges for insurers, actuaries, and risk managers alike, leading to increased costs and complexities in compliance and managing risks. In this article, we delve into the concept of social inflation, explore current trends, and discuss strategies that employers can employ to address its effects effectively.

Background

For the purpose of this article, social inflation refers to the rising insurance claim costs above economic inflation due to societal and legal trends that increase the dollar amount of claims settlements and judgments. It encompasses various factors, including evolving attitudes toward litigation, changing legal interpretations, and increasing jury awards. For instance, more employees are seeking legal counsel to resolve workplace-related issues and asking for higher settlements than in the past. Several underlying elements that contribute to social inflation include:

- Litigious Culture: Society’s growing propensity to turn to litigation as a means of workplace conflict resolution has fueled an increase in the frequency and severity of insurance claims.

- This phenomenon is playing out across multiple lines of coverage including Workers’ Comp, Employment practices liability insurance (e.g., employee misconduct, sexual harassment, wrongful termination, etc.) professional/general liability, and auto (both individual and commercial). It is important to note as litigiousness varies by state/region so does the impact of social inflation on insurance cost between two different locations.

- Judicial Trends: Courts’ and jury’s decisions and interpretations of laws, particularly regarding liability and compensation, have become more favorable towards claimants, resulting in larger settlements and verdicts.

- Economic Factors: Economic downturns or uncertainties may prompt individuals to pursue legal avenues for financial security, adding to the volume of claims and the pressure on insurers to settle.

- Media and Advocacy Influence: Public perception and media coverage of high-profile cases can shape attitudes towards compensation and influence jury decisions, potentially leading to inflated awards.

- Litigation Funding: Third-party investors may provide litigation finance to plaintiffs, driving up pressure to prolong lawsuits and possibly resulting in higher awards and increased legal expenses.

The combination of these factors has created a challenging environment for insurers and businesses, leading to increased premiums and retained losses for the insured and reduced profitability, and greater uncertainty in estimating future liabilities for the insurance carriers.

Social Inflation’s Impact on the Market

Here are some ways social inflation has been impacting P&C markets:

- Rising Claims Costs: Insurers have experienced a notable uptick in claims costs across various lines of business, including auto liability, general liability, and professional liability.

- Increased Frequency of High-Dollar Claims: There has been a noticeable increase in the frequency of large claims and multimillion-dollar settlements, particularly in cases involving bodily injury, property damage, and product liability.

- Erosion of Underwriting Profitability: Social inflation has contributed to declining underwriting profitability for many insurers, as higher claim payouts outpace premium revenue growth therefore many carriers were forced to take large rate increases.

- Reserving Challenges: Insurers face challenges in accurately reserving for future claim payments, given the uncertainty surrounding the magnitude and frequency of social inflation-driven losses.

These circumstances underscore the need for proactive risk management strategies to mitigate the impact of social inflation on businesses and insurers alike.

Addressing Social Inflation: Strategies for Employers

In today’s dynamic business environment, where the landscape of P&C insurance is continually evolving, addressing social inflation has become a paramount concern for employers. Failing to acknowledge and mitigate the impacts of social inflation can lead to significant financial ramifications and operational disruptions for businesses of all sizes and industries.

- Risk Identification and Assessment: Employers should conduct comprehensive risk assessments to identify potential exposures to social inflation-driven claims. This involves analyzing industry trends, historical claims data, and emerging legal developments to anticipate future liabilities.

- Risk Optimization: Employers can explore alternative risk transfer mechanisms, such as captive insurance or excess liability coverage, to mitigate the financial impact of large claims and volatile insurance markets.

- Investment in Loss Prevention and Safety Programs: Proactive investment in loss prevention and safety programs can help reduce the frequency and severity of insurance claims, particularly with lines like workers’ compensation and auto. These programs, or lack thereof, will be imperative in claims settlements.

- Contractual Reviews and Protections: Employers should review and update contractual agreements to include indemnification provisions, liability limitations, and alternative dispute resolution mechanisms to mitigate the risk of costly litigation and claims disputes.

- Engagement with Legal and Insurance Partners: Collaboration and alignment with legal counsel and insurance partners is essential for staying informed about evolving legal and regulatory trends and developing effective risk management strategies tailored to the organization’s specific needs.

Social inflation poses significant challenges for insurance providers, businesses, and risk management teams. This requires a proactive and multifaceted approach to risk management, risk assessment, and corporate risk profile to adapt as the forces behind social inflation are constantly shifting. By understanding the underlying drivers of social inflation, monitoring industry trends, and implementing effective risk mitigation strategies, employers can better navigate this landscape and safeguard their financial stability in the face of uncertain liabilities.

As Captive International and Spring share the same birthday (March 24th), here is a collaborative Q&A with our leadership team. Some of the topics discussed include the progression of the captive industry, market challenges and future opportunities.

Each year on International Women’s Day, I take time to reflect on the women in my life, the state of women in the workforce and the progress and barriers that remain. While there has been great progress to encourage greater equity and opportunity both here and in the workforce broadly, obstacles still exist that prevent women from building generational wealth.

In fact, one of the largest gaps we see in our clients’ employee benefits and healthcare programs pertains to women’s health issues. Organizations and society at large continue to take a narrow view of women’s health, limiting their approach to traditional pregnancy-related benefits. However, women’s health covers a much wider spectrum of issues including infertility, menopause, the stress of caregiving, breast cancer, and so much more.

Over the years, more and more women have joined the workforce, but their home and personal lives have not stopped for the benefit of their careers. Meanwhile, the health and benefits environment has not caught up to where we are or what is needed. I am proud that we routinely help employers assess whether their health plans take a 360-degree view of all components of women’s health issues and if they address gaps that may exist to help provide a level playing field for women in the workforce.

Only when we provide women the healthcare they need to be successful, can we begin to make a real and meaningful impact on ensuring women have the tools and support they need to build the futures they imagined. This means women can be more productive and build wealth to have greater access to opportunity. With greater health equity, she can access the care she needs, along with paid time off and treatment without exiting the workforce, which we have seen time and time again. In fact, healthier women are proven to expand their wealth which, in turn, means expanded opportunity.

While this year I do feel more positive about women’s position in the workplace than in years past, let’s not forget that pay inequity still exists – 84 cents is not equal to a dollar – and that women across the country are struggling to meet their basic health needs with any type of support.

In 2024, let’s make healthcare inequity a thing of the past, and healthier and better-supported women our future.

As Captive Review celebrates its 25th birthday, they have released a list of the 25 most influential people in the captive space in the last 25 years. Our Managing Partner, Karin Landry was featured in their list for her expertise in risk management and alternative risk financing solutions. You can find the full article here.

Title:

Senior Consulting Actuary

Joined Spring:

I joined Spring in May 2014, shortly after graduating from Northeastern.

Hometown:

Central MA

At Work Responsibilities:

My actuarial focus is mainly health and medical stop-loss.

Outside of Work Hobbies/Interests:

Sports

Fun Fact:

I’ve been known to card count.

Describe Spring in 3 Words:

Never a dull Moment!

Favorite Movie/TV Show:

Inception/Seinfeld

Favorite Food:

Cheese

Favorite Place Visited:

Italy

Favorite Band/Musician:

Changes by the day!

If You Were a Superhero, Who Would You Be?

Batman.

Name One Thing On Your Bucket List:

Retire

What is One of Your Proudest Moments?:

I don’t know that I have any singular big ones, but I am proud every time we get positive client feedback

If You Win the Lottery, What is the First Thing You Would Do?

Invest!

What are You Passionate About?

Financial Literacy