In August 2022, the Inflation Reduction Act (IRA, P.L. 117-169) was signed into law, bringing significant changes to Medicare. The law expands benefits, reduces drug costs, and improves the sustainability of the program, providing meaningful financial relief to millions of Medicare beneficiaries by enhancing access to affordable treatments1.

For the first time, Medicare now has the authority to directly negotiate the prices of certain high-cost, single-source drugs that lack generic or biosimilar competition. This groundbreaking provision is designed to help control costs and ease the financial burden on both the program and its participants.

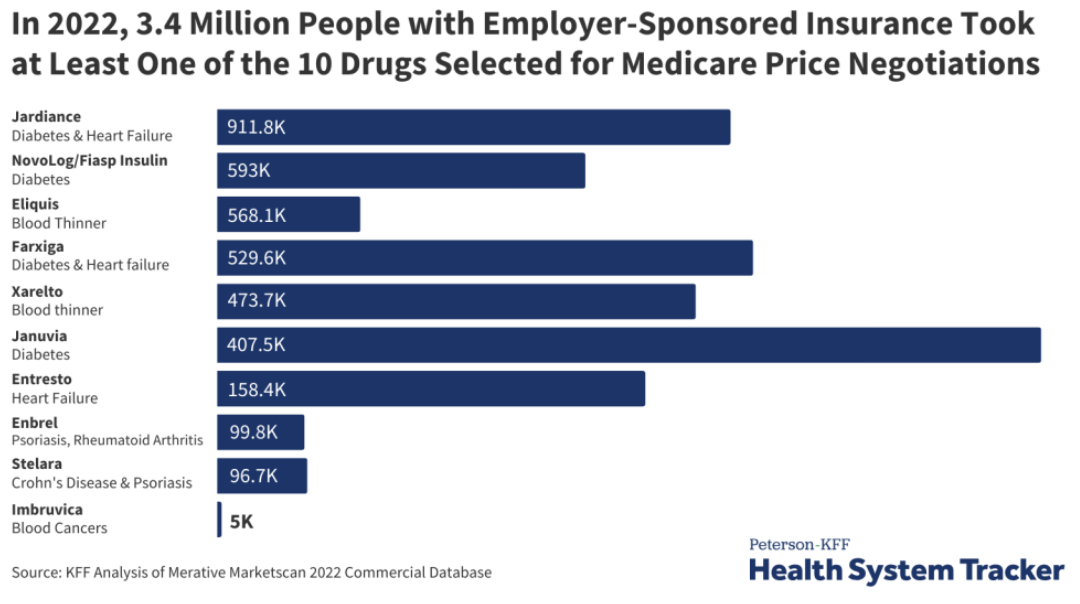

Medications Selected for Price Negotiation

The Centers for Medicare & Medicaid Services (CMS) identified the initial group of drugs for negotiation based on multiple criteria, including the drug’s cost and the number of Medicare Part D enrollees currently using them. CMS engaged in direct negotiations with drug manufacturers to secure lower prices for some of the most expensive brand-name medications.

This negotiation process includes CMS presenting a final offer to the manufacturer, which can either accept or reject the proposal. The outcome? CMS and participating manufacturers have finalized pricing agreements, with Maximum Fair Prices (MFP) for ten selected drugs set to take effect on January 1, 20261,4.

This initiative is part of a broader, multi-year effort. By February 2025, CMS will select up to 15 additional drugs covered under Medicare Part D for negotiation, with new prices projected to be implemented in 2027. Another 15 drugs will be chosen in 2028, and an additional 20 the following year, expanding the reach of negotiated price reductions as required by the IRA4.

Although the Medicare drug price negotiations don’t apply to private insurance, 3.4 million people with employer coverage take at least one of the selected drugs. The ten medications are listed in the below graph3.

How Does This Affect Commercial Insurance?

Although these Medicare negotiations do not directly apply to private insurance, they could still have ripple effects on commercial drug pricing. Currently, 3.4 million people with employer-sponsored coverage use at least one of the drugs selected for negotiation3.

The impact on commercial insurance remains uncertain. Some experts suggest that lower Medicare prices could result in higher costs for private insurers as manufacturers look to recoup losses. Conversely, others believe that the negotiated Medicare prices could serve as a benchmark, potentially leading to lower prices in the private sector as well3.

While it’s too early to tell how private insurance will be affected, the ongoing Medicare drug price negotiations will be a closely watched development in the healthcare landscape.

To stay updated on this topic and learn more, click here.

1 Negotiating for lower drug prices works, saves billions. CMS. August 15, 2024. Accessed September 13, 2024. https://www.cms.gov/newsroom/press-releases/negotiating-lower-drug-prices-works-saves-billions

2 https://www.ajmc.com/view/lower-drug-prices-announced-under-medicare-negotiation-program

3 https://www.kff.org/medicare/issue-brief/explaining-the-prescription-drug-provisions-in-the-inflation-reduction-act/

4 https://www.cms.gov/inflation-reduction-act-and-medicare#:~:text=The%20Inflation%20Reduction%20Act%20makes,and%20limiting%20increases%20in%20prices

On September 1, 2024, we celebrated a significant milestone: the 50th anniversary of the Employee Retirement Income Security Act (ERISA). Signed into law by President Gerald Ford on September 2, 1974, ERISA has quietly yet profoundly impacted the lives of countless Americans, ensuring that promises made regarding retirement and health care benefits are promises kept.

ERISA: A Commonly Overlooked Law That Impacts You

While the average American may not recognize the name, ERISA likely plays a crucial role in their lives. This landmark legislation sets minimum standards for most established retirement and health plans in the private sector, providing essential protections for plan participants and beneficiaries in employee benefits plans. From safeguarding retirement savings to ensuring that benefits regulations and requirements are adhered to, ERISA has been a cornerstone in the benefits industry for the past five decades.

A Journey Through ERISA’s History¹

The story of ERISA began with a series of broken pension promises that left thousands of employees without the benefits they were owed. The most notable case was the closure of Studebaker’s South Bend, Indiana plant in 1963, where workers were denied the pensions they were promised. This incident, among others, underscored the urgent need for pension reform and captured the public’s attention.

In response, President John F. Kennedy created the President’s Committee on Corporate Pension Plans in 1961, which issued its report in 1962. Senator Jacob Javits introduced pension reform legislation in 1967, and the momentum continued to build, especially following the release of the 1972 Peabody Award-winning documentary, Pensions: The Broken Promise. Public hearings were held, legislative efforts advanced, and finally, the Employee Retirement Income Security Act was signed into law in September 1974.

Senator Javits, the principal sponsor of ERISA, described it as “the greatest development in the life of the American worker since Social Security.” ERISA has shaped how employers provide retirement and health benefits, working behind the scenes to set standards that protect millions of workers and their families. ERISA was passed by the House in a vote 407 – 2 and unanimously approved in the Senate demonstrating how united the country was behind this important piece of legislation.

The Evolution of Employee Benefits and Captives

ERISA’s influence extends beyond traditional employee benefits. Over the years, there has been notable growth in employee benefits provided through captives—specialized insurance companies owned by the businesses they insure. This trend has enabled companies to have greater control and flexibility over their benefits offerings while managing risks more efficiently. Not all benefits are subject to ERISA, as seen below, but if they are, they need to go through a filing process with the Department of Labor (DOL) to receive a prohibited transaction exemption (PTE). The goal of the PTE process is to ensure that the interests of plan participants in the captive model are still protected, through an additional layer of DOL oversight surrounding fair pricing and compliance.

As captives grow in popularity, they provide new opportunities for employers to offer competitive, tailored benefits while achieving cost control—a trend ERISA has helped enable by providing the regulatory framework necessary for captive expansion and innovation.

Looking to the Future: ERISA’s Continued Relevance

Fifty years on, ERISA remains as relevant as ever. A recent example of ERISA’s modern influence is the tentative approval given by the DOL to leverage a captive to fund pension plan risk for the first time. This development benefits both plan sponsors (employers) grappling with pension plan liability and benefits recipients.

As we navigate new challenges in the benefits landscape—from evolving retirement needs to the complexities of modern healthcare—ERISA provides a foundation that ensures the rights and protections of millions of Americans are upheld.

1 https://www.dol.gov/agencies/ebsa/about-ebsa/about-us/history-of-ebsa-and-erisa

As Vermont was named the largest captive domicile globally in 2022, it has developed into a hub for alternative risk financing and insurance innovations. The Vermont Captive Insurance Association (VCIA) recently hosted its 2024 Annual Conference, a beacon in the captive insurance industry. This year’s conference, held in the heart of Vermont (Burlington), offered a dynamic platform for industry professionals to delve into the evolving landscape of captive insurance. From exploring the fundamentals of captive formation to addressing the pressing challenges posed by emerging technologies and regulatory changes, the conference provided invaluable insights and strategies. Attendees had the opportunity to engage with thought leaders, share best practices, and discover innovative solutions that will shape the future of the industry.

1) Captive Formation and Feasibility

Since Vermont is the most popular domicile globally, VCIA provides a great avenue to help first-time employers explore potential captive endeavors. Understanding the basics of captive formation and testing for feasibility is essential for anyone looking to establish or manage a captive insurance company. Here are some related sessions that caught my eye:

-The opening session, “Captive Immersion: Feeling Puzzled? Let’s Piece It Together,” brought together various stakeholders, including an attorney, underwriter, actuary, consultant and a state official to give piece-by-piece instructions on entering the captive industry.

– The presentation, “The Economic Landscape & Your Captive’s Investment Portfolio,” reviewed the current state of the economy and macroeconomic factors that may influence investment gains in a captive.

2) Emerging Technologies and Innovation

As the risk landscape evolves rapidly, captives must adapt to emerging tools and technologies. Addressing emerging risks such as cyber threats and leveraging innovations like AI and data analytics are vital for maintaining relevance and effectiveness in risk management, ensuring captives can proactively manage and mitigate modern challenges. These presentations spotlighted the need for alternative solutions to address emerging (and at times unforeseen) risks:

– The Cost of Compliance: ADA/FMLA Court Cases and Jury Verdicts offered a deep dive into recent legal cases, providing lessons on how to avoid costly compliance mistakes.

– The presentation, “Your Data Reimagined! A Captive Case for Data Visualization,” showcased how employers can utilize data visualization to help interpret large data sets and areas for risk optimization.

3) Regulatory and Compliance Updates

Navigating the complex regulatory environment and staying updated on captive taxation and oversight changes are crucial for compliance and strategic planning. It is essential that captive managers and owners are informed about regulatory requirements and can adapt their practices to remain in good standing and avoid potential legal pitfalls. Some insightful sessions include:

– Our VP, TJ Scherer, teamed up with the State of VT’s Dan Patterson in an open discussion group to chat about “Upcoming Changes in Regulation Oversight” and what captive owners in VT should keep their eyes out for.

– Four tax experts convened to discuss “Captive Taxation: What’s New & What’s Next.” They reviewed recent IRS, federal and state updates and discussed how companies can best prepare for an IRS audit.

4) Passing the Torch

Energizing new leaders and providing growth opportunities for newcomers are essential for the long-term sustainability of the captive insurance industry. By fostering new leadership, organizations can drive future success and address the ongoing challenge of talent shortages. These topics focused on the importance of developing talent to ensure that fresh perspectives and innovative ideas are woven into the industry:

– State of VT’s Chief Examiner, Heidi Rabtoy’s “Discussion Group: Attracting & Energizing New Leaders” spotlighted the current talent shortage in the insurance space, and tips to attract and retain next-generation industry leaders.

– One of my favorite parts of VCIA is the Newcomers’ Orientation; ensuring first-time attendees are educated and feel welcome is essential to the industry’s future success.

The enthusiasm and forward-thinking discussions from this year’s conference left a lasting impact on the captive insurance landscape. The conference highlighted the importance of understanding the fundamentals of captive formation and staying ahead of emerging risks, underscoring the critical need for compliance amidst shifting regulations. Moreover, the focus on cultivating new leadership promises a vibrant future for the industry. By harnessing the knowledge and connections gained at VCIA, risk professionals are well-equipped to navigate the complexities ahead and drive continued success in the world of captive insurance.

As summer winds down, the Disability Management Employer Coalition (DMEC) hosted its 2024 Annual Conference in the energetic city of Nashville, TN. Known for its rich musical heritage, Nashville provided a lively backdrop for this year’s event, bringing together professionals from across the absence management spectrum to discuss the latest trends, challenges, and best practices. Here are some key highlights from the conference.

1) The Future of Paid Family and Medical Leave (PFML)

The focus on mental health remains prevalent as organizations continue to find innovative ways to support employee well-being. This year’s conference offered valuable insights into how mental health is evolving in the benefits industry:

-The session The Importance of a Guided Claim Experience emphasized the need for compassionate and informed support during the claims process, which can significantly impact employee well-being.

– I was joined by a group of leave solution leaders to examine findings from a recent leave report which looked at various factors including recruitment, retention, productivity, moral, and more with a focus on how successful employers are addressing leave managementns on benefits spend and workplace culture.

– One of the catchiest presentations, Walk, Crawl, Run: The PWFA Turns One, reflected on the one-year anniversary of the Pregnancy Workers Fairness Act (PWFA) and best practices for HR teams to stay compliant.

2) ADA/FMLA Compliance Updates

Navigating the complex web of federal, state, and local regulations remains a critical challenge for employers. This year’s sessions provided valuable guidance on staying compliant while managing diverse and geographically dispersed workforces:

– The Cost of Compliance: ADA/FMLA Court Cases and Jury Verdicts offered a deep dive into recent legal cases, providing lessons on how to avoid costly compliance mistakes.

– The ADA Compliance Mini Boot Camp led by Rachel Shaw was a must-attend for anyone looking to deepen their understanding of ADA requirements and refine their compliance strategies. This workshop was instrumental in equipping participants with tools to tackle common challenges and elevate their programs.

– I led a workshop with Baystate Health’s Manager of Disability and Leave, Lauren McCormick, in a session titled A Step-by-Step Guide to Refining Your ADA Strategy. In an interactive format, the session provided participants an opportunity to address real-life ADA scenarios and how to best address each individual case using a methodical process.

3) Telework Accommodations

As companies continue to navigate the post-pandemic landscape, finding the right balance between remote work and returning to the office is top of mind. The conference sessions provided practical insights into managing this transition effectively:

– The session “You Can Have Paid Leave AND a Productive Workforce. Here is the Secret Sauce.” explored how flexible work arrangements can coexist with robust paid leave policies to enhance employee satisfaction and productivity.

– Council from Reliance Matrix explained how many employers are quick to provide leave of absence to workers with a medical condition, whereas many alternative compliant leave options exist in their presentation, Encouraging Employees to Stay at Work or Return to Work.

–Another eye-catching session, We Goofed. Now What? An Accommodations Tale, brought light to a common scenario in which an employer fails to provide adequate accommodations under the ADA and/or PWFA; as well as best practices to address said employees’ needs.

4) Tech/AI’s Role in Absence Management

Technology continues to play a transformative role in the absence and disability management space, offering new ways to streamline processes and improve decision-making:

– Spring’s in-house attorney, Lynne Noel, together withPatagonia’s Senior Manager, Leave of Absence, Lauren Shipper, discussed Using Benchmarking to Refresh Your Program. They highlighted the importance of leveraging data to stay competitive and refine absence management programs. Insights provided actionable strategies for using benchmarking as a tool for continuous improvement.

– A group of data analytic experts explained the practical parameters of AI solutions in claims processes and the upsides and dangers to implementing AI systems in their presentation, The Transformation: How AI is Enhancing Analytics and Optimizing Decision-Making.

– During the session, The Future of AI in Leave and Disability Management, three leave and disability administrators discussed the current state of AI in the industry and how it can help streamline processes and improve employee satisfaction.

Final Thoughts

The DMEC 2024 Annual Conference in Nashville was a resounding success, filled with opportunities to learn, connect, and share best practices. From deep dives into compliance and mental health to exploring the latest technological innovations, the conference offered something for everyone. As always, it was a pleasure to reconnect with industry leaders and bring back fresh ideas to enhance our consultative offerings. We’re already looking forward to what next year’s conference will bring!

One of the most exciting attributes of captive insurance is that every program looks different. There is so much variety and a wide range of ways to structure coverage and utilize surplus. I have been talking with captive owners representing various industries, organizational sizes, and stages of captive maturation to get their unique stories and understand how they are putting their captive to work for their specific risks. Indeed, no two stories have been the same.

In a recent interview, I sat down with Karen Hsi, Executive Director, Captive Programs at University of California Office of the President, and one of the sharpest minds of young captive talent. The University of California (UC) did not need to obtain Department of Labor (DOL) approval for their captive programs, making the process simpler!

Q: What benefits do you currently have within your captive, and why did you choose the captive path?

A: On the employee benefits side, we have voluntary benefits – accident, critical illness, and hospital indemnity – in our cell captive. This program has been in effect since the start of 2020 and uses a fronting carrier, and as of this year (start of 2024), it is 100% seeded to the cell captive.

We brought these products into the captive because we wanted to customize offerings and add some bells and whistles for employees at a better price. We used a cell captive so that we wouldn’t jeopardize the tax status of our single parent captive. Our original goal with this strategy was not to make money but break-even while primarily to be able to offer better benefits.

Over the course of time we have been able to build a stable program, and after shifting away from a broker structure so that commissions and other costs are stripped out. As we establish these financial efficiencies, we want to keep building upon the program either by reducing employee costs or by further enhancing or customizing offerings. For example, one unique benefit that we were able to add with our surplus is a mammography offering within critical illness. We found that utilization was high, so we are confident it adds value to employees. Another policy we were able to add into the supplemental health program was a COVID-19 rider, which had a cash incentive for employees to proactively get tested for the virus. We were able to put this in place quickly and think we would have had a hard time doing so without the captive.

Overall, we have seen about 20% savings with this program and as things stabilize, we hope to lower rates further for employees.

Q: Are there any other benefits UC has in a captive?

A: We write life insurance – employer and employee paid – in a separate cell captive because it is large enough for its own cell. The life cell captive also launched in 2019 and is doing well, with approximately $16.3M in accumulated earnings since inception. During the pandemic, we had a fair amount of turnover, so we used the success of the captive to boost our life insurance policy as a tactic for succession planning and business continuity.

We hope to someday to move disability into the captive, but the timing hasn’t been right yet. We want to better manage the risk first so that the board is more amenable to bringing it into the captive.

Q: Any other surprises?

A: I think in the beginning it was a mindset and relationship change when we shifted things with the carrier to move to a fronting company. They now have a seat at the table and we have a longstanding relationship.

Q: Anything interesting on the horizon?

A: We are looking into the potential of long-term care insurance in a captive. There also might be an opportunity to rent out a cell captive to one of our sister/affiliate organizations (e.g., California State entities), where they have their own cell and voice and where we can provide resources. I think this might be a beneficial move and would be a valuable way to collaborate.

No matter what the future brings, I know that we are not done yet (with growing our captive programs), and we’re excited to see what else we can do. I appreciated the time Karen spent in chatting with me and will be paying close attention to these exciting developments and opportunities to expand their captive. If you’re looking for expert advice to assess feasibility of additional benefits in your captive, feel free to get in touch with our team.

The United States Department of Labor (DOL) has tentatively authorized an Employee Retirement Income Security Act (ERISA) exemption regarding pension plan risk transfer to a captive. This healthcare network is the first organization in history to receive ERISA approval to transfer pension risk in a captive. This is groundbreaking news, as it opens the doors for plan sponsors to better manage their risk related to defined benefit pension plans programs. In short, using captive insurance companies rather than traditional insurers alone gives plan sponsors the opportunity to fund their pension risk more cost effectively.

Their employees engage in groundbreaking cancer research and provide lifesaving care for patients. The employer engaged with Spring, to help design and implement this unique program for its retirement benefits. This included conducting actuarial analyses, navigating vendor and partner avenues, structuring transaction and direct contact with the DOL to work through the exemption process. Once approved, the employer is anticipated to receive $126.4 million in financial benefits from the DOL. As part of the terms of the exemption, the employer will be providing a one-time cost of living increase to the monthly retirement benefit to all plan participants and beneficiaries.

This is a groundbreaking next step in the evolution of risk management programs and set the stage for many other employers who are trying to structure a better program for their employees.

Every industry has its own challenges and nuances. Since our client base is widely varied, we routinely partner with our clients to tackle unique, industry specific obstacles as they build out customized employee benefit programs and strategies. When it comes to the airline sector, a specific pain point relates to adequate long term disability coverage for their licensed pilot employees.

Background

Pilot union contracts typically require airlines (the employer) to provide long term disability (LTD) insurance to their pilots, but this coverage has become nearly impossible to procure in the traditional LTD market, for a range of risk reasons:

- Volatility and financial hardships in the airline industry, with bankruptcies and federal bailouts not uncommon

- Pilot unions, such as ALPA, APA, and SWAPA, can be litigious in fighting for their members, making pilots less favorable in the eyes of insurance carriers

- Federal Aviation Administration (FAA) oversight regarding the fitness of a pilot complicates claims processes

- The nature of the job poses special risks, including:

- Consistent exposure to high altitude

- Safety considerations

- Prone to illness or injury due to physical and mental demands

Pilots are humans like the rest of us, but given the stressful nature of their job and the consequences of their environment, they might be in greater need of LTD coverage than the average worker. For example, the FAA estimates the prevalence of substance misuse is 8.5% among pilots, with other sources placing that rate as high as over 15%1.

Sensibly, the FAA’s regulations around pilot licensing are very stringent, so there is a large risk that a pilot will lose their license over a medical condition, including the substance issues referenced above. As a result, the gap in the market for conventional LTD coverage has yielded a specialty market specific for pilots, which is based on the loss of a pilot’s license instead of the traditional definitions of disability, which are based on the ability to perform either the material and substantial duties of one’s own occupation or any occupation which could be reasonably expected to perform in light of their background. Since these loss of license plans are generally structured either as a monthly benefit while a pilot is grounded or as a lump sum, pilots who do not lose their license essentially have no product option available that provides income replacement as a traditional LTD plan would. In addition, even when the specialty coverage would provide a benefit, it is limited in availability and, with very little competition, premiums are high and there is minimal, if any, room for customization.

Potential Solution

At Spring, we often say that captives are the whiteboard of insurance, meaning that they can be leveraged and crafted in a diverse range of ways to solve for unique and evolving challenges. LTD coverage for pilots can be added to that whiteboard.

Most airlines currently have a captive insurance company, which they may only be utilizing for property and casualty (P&C) lines of coverage. Even when an airline does have employee benefits in their captive, they are typically not leveraging the captive for long term disability insurance or other voluntary benefits.

Long tail risks such as disability are particularly beneficial for captives. Traditionally, when premiums are paid to carriers they hold and maintain any investment income earned on reserves. When funding these long-term liabilities through a captive, the investment income earned is held until the time of loss and stays within the captive. These investment returns are substantial and serve as yet another benefit for placing disability coverages into the captive.

Having employee benefits (including LTD) in a captive provides the following advantages:

- Cost savings and improved cash flow

- Increase cost certainty and support budgeting

- Reduce operating costs

- Control over underwriting and funding

- Flexibility in terms and conditions

- Better claims management

- Improved access to data

The biggest benefits for airlines placing LTD through their captive program is creating greater control of customization of coverage and are less susceptible to market volatility and pricing by moving away from the commercial market.

Having a combined P&C and employee benefits captive program, which incorporates LTD, would further strengthen the airline’s overall captive and risk management strategy by offering risk diversification, since LTD risks are unrelated to the existing P&C risks underwritten in the captive. Along with projected increased profits of the LTD line of coverage, this approach increases the number of statistically independent exposures, which improves the stability of the overall program. In addition to LTD, medical stop loss could also be added to the captive to protect against catastrophic claims and create more predictability.

Action Plan

LTD insurance for pilots has been an issue for years in the airline industry, and no optimal commercially available solution has come forth. Captive insurance has long been a strategic approach to niche or especially challenging insurance obstacles and essentially how and why captives were born. The LTD commercial market is prime for disruption, and for those willing to move towards a more flexible and beneficial program, a captive insurance company can provide an answer.

The absence management conversation is a critical component of every employer’s broader employee benefit strategy discussion these days, especially given the competitive talent market and the rapidly evolving regulatory landscape surrounding leave of all types and at all levels (federal, state, local). Now, more than ever, employers and employees need to understand how all available benefits, including supplemental health plans, such as Accident, Critical Illness, and Hospital Indemnity, work together. Compliance isn’t the only consideration, though. Employers need to be sure not to duplicate processes which can increase costs as well as to ensure a smooth and positive employee experience.

Understanding supplemental health products and the benefits provided by them ensures that those paying for the coverage will fully utilize the benefits available. Since Accident, Critical Illness, and Hospital Indemnity benefits are paid when an accident occurs, a critical illness is diagnosed, or a hospital stay is required due to injury or illness, they offer a way to fill in the financial gaps left by traditional health insurance, disability coverage, and paid leave benefits. The lump sum benefits paid by the supplemental health plans can be used to cover out-of-pocket expenses like medical copays and deductibles, as well as to supplement the income replacement benefits provided by paid leave and/or disability plans.

The good news is that insurance carriers have made significant progress over the last few years toward the integration of absence and supplemental health products.1 Many are, now, not only bundling supplemental health products with their core disability and absence products and offering a package discount to the core products when quoting, but also tackling the more complex issue of how to ensure that employees enrolled in supplemental health plans are receiving the financial benefit of the products they pay for with payroll deductions.

To ensure that supplemental health plan participants receive the benefits they are entitled to under their policies, most carriers are digging into questions like:

- How can they identify disability and leave claimants who are also enrolled in one or more supplemental health product(s)?

- Is there a way to leverage the claim information obtained during the leave and disability claim process(es) to pay supplemental health claims without having to request redundant or additional medical information?

Carriers are also reviewing their processes to find efficiencies and create a better claimant experience. This internal retrospection has led to things like coordinated leave, disability, and supplemental health claim intake and the sharing of medical information across all claims. Many carriers are not only building out coordinated claim paths and workflows for leave, disability, and supplemental health claims, but they are also having their leave and disability claim specialists conduct routine analysis of current leave and disability claim files to see what other coverages an insured is eligible for and whether the medical information on file could be used to adjudicate the corresponding supplemental health benefit claims. Some carriers who have access to medical claim files offer auto-generated notifications, which are sent to supplemental health plan participants, reminding them of their supplemental health benefits based on the medical claim data. Software and technology companies as well as third-party administrators (TPAs) who often handle leave benefit administration are also focused on product improvements in the areas of artificial intelligence (AI), automations, self-service portals, communications, intake, and reporting. All these claim process adaptations alleviate steps for the insured and make it easier, overall, for them to know what benefits are available and be able to utilize them. They also help claimants to maximize the value of the benefits for which they are paying and enhance the customer experience that is top of mind for employers of all types, sizes, and industries.

1 Spring Consulting Group. 2022-2023 Integrated Disability, Absence, and Health and Productivity Vendor Benchmarking Survey.

Since I started my career in this space many moons ago, I have seen the captive industry continuously grow and evolve. There have been new risks, changes in regulatory and Department of Labor (DOL) policies and protocols, economic fluctuations, the addition of technologies, and the integration of captive programs focused on different lines, whether employee benefits or property and casualty (P&C). As I believe we are at the cusp of the next era of change for captives, I wanted to connect with captive owners and risk managers to gather their outlook on where we are today and where we’re headed.

I sat down with David Arick, who is currently the President of RIMS, the risk management society® and Managing Director, Global Risk Management at Sedgwick. He has previously held insurance and risk management roles at companies like International Paper and General Electric, and brings forth a wide range of experience spanning decades.

Q: How has the hard insurance market impact risk professionals’ ability to financial cover their organizations’ top risks?

A: Different industries have had different experiences in this market. My last job was in the packaging and forest products industry and it, along with other sectors like transportation, have been challenged. The hard market coupled with specific insurance conditions like nuclear verdicts and natural disasters on the P&C side have been driving up property costs. Cyber insurance has also faced obstacles. The economics of a specific company along with the insurance budgets that get blown out of the water really have people looking for alternatives like captives.

Q: What do you feel are some of the contributing factors that have led to the increased popularity in captives?

A: Aside from what I mentioned above, captives are no longer uncommon or kept behind closed doors; they are now a part of mainstream risk management and C-suites are willing to make the investment given the volatile insurance markets they are facing.

Q: What benefits are most appropriate for organizations to place in their captives? Have you seen any new developments in this area?

A: From a risk management perspective, I hear my fellow risk managers talking about three areas where benefits and captives can interplay:

- Global benefits. Risk managers are hoping that captives can help stabilize programs that historically were variable and volatile across different countries, particularly with a workforce moving between countries.

- Medical stop-loss. Captives are playing a huge role in this area where a risk manager can partner with HR in understanding stop loss buying options available thanks to the captive and also creating savings and flexibility within the program.

- ERISA benefits. Multinational companies have been focused here in terms of trends, take-up rates, etc. Benefits spend in the US is more significant than in other countries and to that end there is renewed interest in utilizing a captive to address these rising costs.

Q: I’ve heard you say before, “risk management is much more than buying insurance or financing losses,” can you elaborate on that statement a bit?

A: Both risk management and insurance buying are critical aspects of running a business. The point is that I would hope that risk management could be more strategic, aimed at creating risk awareness and focused on people, processes, and technology in addition to the more traditional items like mitigation plans, business continuity and the like.

Q: This year, as RIMS President, what are some of your priorities for the organization and the risk management profession overall?

A: I would like to improve the perception of risk management by increasing education and development for those in the field, so that we can more broadly speak the same language. RIMS has developed a global certification for risk management education called the RIMS-CRMP that is ANSI-accredited and meant to build credibility around the profession. We are investing in our future by highlighting the careers available and introducing risk management curricula to more colleges and universities. It’s important that we routinely assess how to support new talent that joins the field in their professional growth and that is what we’re focused on.

Q: What insights can you offer a risk professional who is either considering starting a captive or who has just started one?

A: I promise you didn’t make me answer the question in this way, but I truly think organizations need to search for the best captive advisors and not just default to their primary brokerage team. An existing team may be sufficient in handling most needs, but a captive is unique and you need an expert team in place, from consultants to lawyers, to captive managers and the like. Secondly, I will say that a risk management professional needs to prioritize building internal support and alignment for an initiative like a captive, including finance, accounting, treasury, legal, and tax. Internal buy-in is critical to long-term success.