In a recent article published by Captive Intelligence, our Chief Property and Casualty (P&C) Actuary, Peter Johnson, reviews current trends in the P&C industry and how risk optimization can help cut costs and increase coverages. Check out the full article here.

Our Managing Partner, Karin Landry will be presenting at The Connecticut Captive Insurance Association (CTICA)’s webinar titled “How to Level Up Your Medical Stop-Loss Program” later this April. You can learn more about her presentation here, and register here.

Captive Review has released a Q&A featuring our Chief Property and Casualty Actuary, Peter Johnson, where he explains the impact of inflation on insurance and risk management practices and how how it intersects with captive insurance. Check out the full Q&A here.

Our Senior Vice President, Prabal Lakhanpal, has recently joined The Captive Insurance Companies Association (CICA)‘s board of directors. He also currently chairs CICA’s NEXTGen Young and New Professionals Committee; check out the full article here.

During The Captive Insurance Companies Association (CICA)’s 2023 annual conference, our SVP, Prabal Lakhanpal presented on behalf of our Managing Partner, Karin Landry, during which he present on what next-gen professionals value most in in a job. You can find Captive International’s recap here.

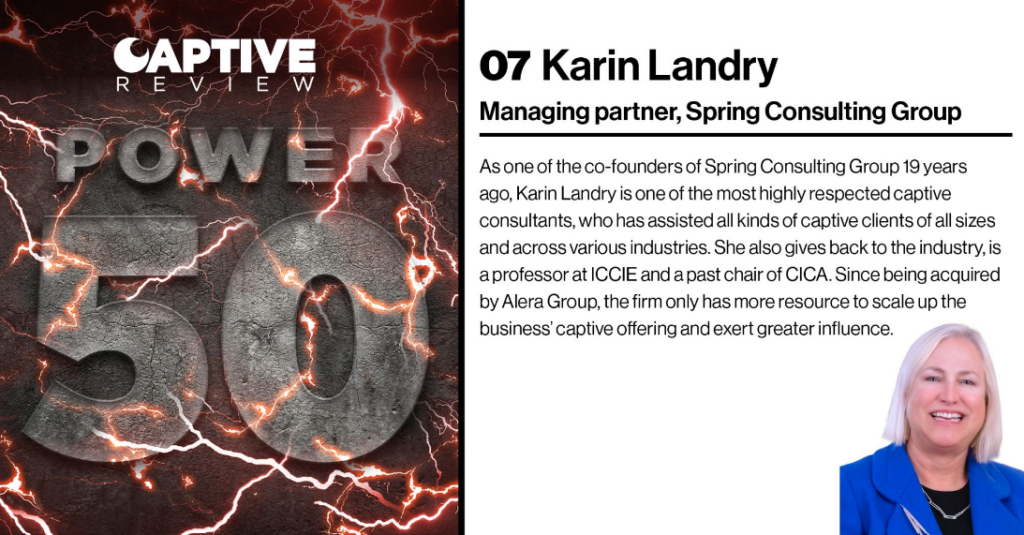

Captive Review releases their annual Power 50, where they showcase top leaders in the captive space. This year, they selected our Managing Partner, Karin Landry, #7. Check out the top 10 professionals here.

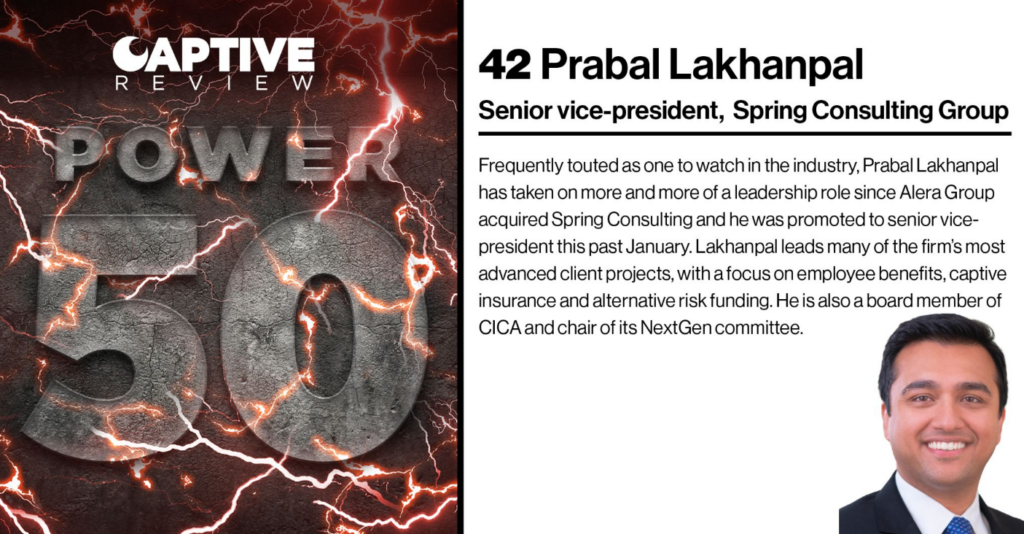

Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our SVP, Prabal Lakhanpal was featured on the list at #42. Check out the full article here.

Our captive insurance team was spotlighted in an article by Captive Intelligence, after helping a client reinsure their employee benefits under the United States’ Employee Retirement Income Security Act (ERISA) into their captive. Our client received final approval from the Department of Labor (DOL) in February 2022, with the last successful applicant obtaining approval in 2017. Check out the full article here.

Following Business Insurance’s 2023 World Captive Forum, an article was written about our SVP, Prabal Lakhanpal‘s session on how captives can be a solution to the changing property insurance market. During which he was quoted on tactics employers can take to help control coverage gaps. Check out the full article here.