Title:

Director of Client Services/Brokerage Practice Leader.

Joined Spring:

I joined Spring in 2015, before Spring was acquired by Alera Group.

Hometown:

I am a New Englander through and through! I was born and grew up in Boston and lived in Jamaica Plain and Roslindale.

At Work Responsibilities:

As Spring’s Brokerage Practice Leader, I work directly with employers and carriers to implement top-tier employee benefits programs for employers of all sizes. Some of most common areas include group health plans, dental, life insurance, disability, and FSAs, HRAs & HSAs.

Outside of Work Hobbies/Interests:

I love being outdoors (when the New England weather allows!). Some of my favorite things to do outside of the office are hiking, fishing, boating, and sports.

Fun Fact:

Many people don’t know this, but I was actually an extra in the movie, “Blown Away”.

Describe Spring in 3 Words:

It’s very tough simplifying my nearly decade at Spring into just 3 words. But I guess I’d have to go with professional, caring, and reliable.

Favorite Movie/TV Show:

I enjoy the classics, my favorite movies are To Kill a Mockingbird and Casablanca.

Do You Have Any Children?:

Yes, I have two children, Ryan and Kaleigh, they’re both in their 20s now.

Favorite Food:

Italian and Japanese!

Favorite Place Visited:

Although these two places are almost polar opposites, my favorites are Italy and Alaska.

Favorite Band:

I love my 80s music, so I’ll have to go with U2.

Bucket List:

I really want to visit the Pyramids in Egypt.

If You Won the Lottery, What Would You Do With the Money?:

I would start a scholarship program for disadvantaged children, to help give them a full ride through college.

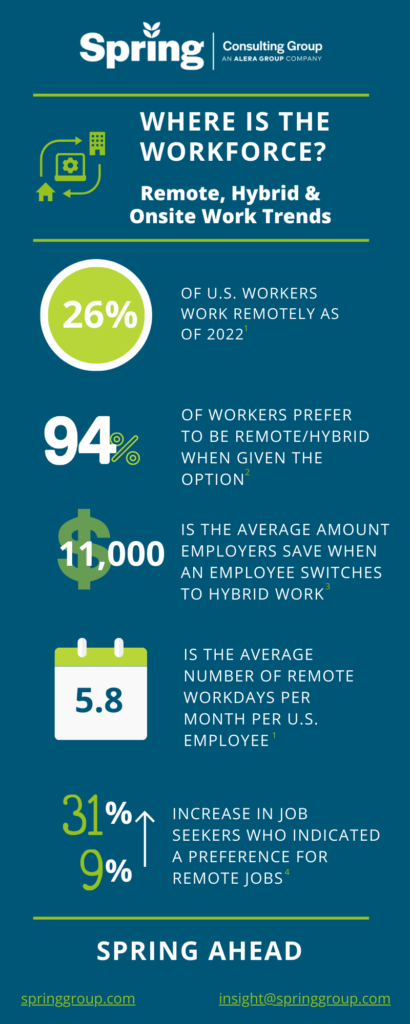

As we transition past the pandemic, we are seeing shifts in remote, hybrid, and onsite practices across the US. Below are some of the top trends impacting workforces nationwide.

1Zippia. “25 Trending Remote Work Statistics [2023]: Facts, Trends, And Projections” Zippia.com. Oct. 16, 2022

2Alera’s EB Market Outlook

3https://globalworkplaceanalytics.com/telecommuting-statistics

4https://fortune.com/2023/01/25/workers-prefer-remote-first-roles-hybrid-work/

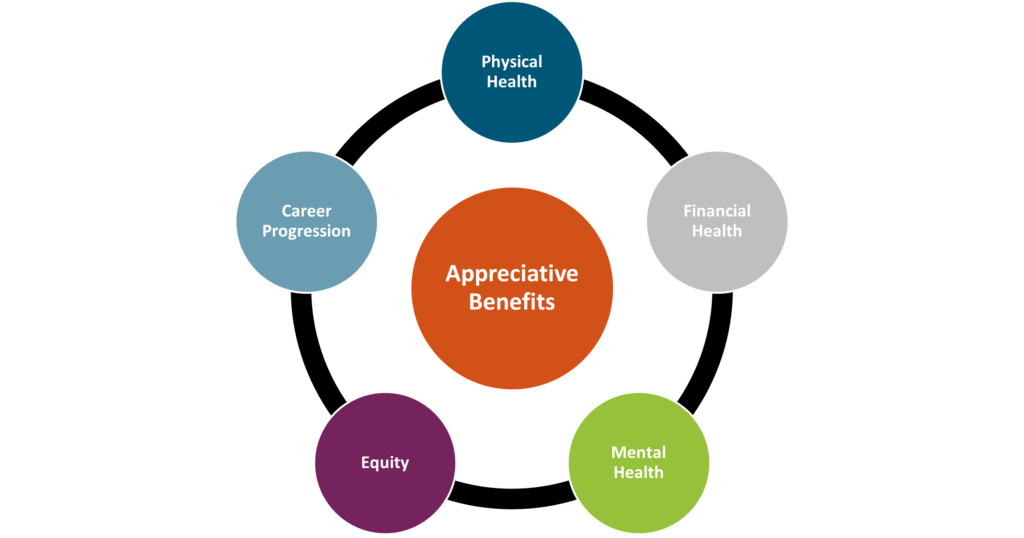

No matter the product or service you’re selling, or the impact your business makes in your community or the world at large, the consensus is that the most important asset an organization has is its people. Our HR and Benefits colleagues know very well that keeping employees happy and engaged (and keeping them in general) is not only makes for a positive atmosphere, but is also a strategic business move. So maybe you’re celebrating Employee Appreciation Day with a grateful shoutout, or a catered lunch, but don’t forget to look at the bigger picture of the precedent you’re setting – whether intentional or not – with your benefits programs.

Physical Health

Beyond the “it’s the right thing to do” mentality, benefits that support employees’ physical health are important for another reason: unhealthy employees will be far less productive, if present at all. Take a look at your health plans to ensure affordability, access, and breadth of care. Components like dental and vision insurance should also be considered here. Beyond health insurance, many companies offer supplementary tools or services that promote physical health such as fitness reimbursements, point solutions for things like diabetes management or musculoskeletal issues, health coaching services, walking challenges, and more.

Mental Health

Mental Health America reported that nearly 20% of Americans were experiencing a mental illness in 2022. The World Health Organization (WHO) states that depression and anxiety cost the global economy approximately $1 trillion every year. While employers cannot solve the mental health crisis, many believe that they do have a responsibility to provide related resources and prioritize employee mental health in some way. At Spring, we recommend tackling mental and behavioral health through the lens of its three most common barriers: cost, access, and stigma. Any programs offered should try and solve for these. For example, does your health plan cover mental health related appointments? In addition, there are a wide range of services available in this area. Some companies bring in yoga instructors on-site. Alera Group provides Spring Health at no cost to employees, which offers complimentary digital therapy sessions, coaching, and other tools. Apps like Calm and Headspace provide guided meditation and anxiety management practices. Paid time off for mental health or built-in “breaks” during the workday, such as designated times when meetings are prohibited, can also help. Simple tactics like demonstrating openness to discussing mental health in the workplace can go a long way to lessen any stigma.

Financial Health

Especially in today’s economy, employees need help saving for retirement, investing wisely, and being financially informed and educated. We also know that financial stress can be related to mental health, so by focusing on financial health you can impact multiple components of employee engagement. At a basic level, leading employers offer a 401(K) or similar retirement savings plan, with an employer match. As a next level, tax-friendly benefits like Health Savings Accounts (HSAs) can be helpful, and there has been a lot of buzz around student debt repayment programs which employers can choose to contribute to or just offer as a voluntary benefit. Other voluntary benefits like life insurance, identity theft protection and short- or long-term disability insurance can contribute to an employee’s financial wellness. Other perks might include financial counseling services and educational seminars.

Equity

Do your employees in different states have access to the same paid leave? To the same reproductive healthcare? To the same disability coverage? Do your executives and your more junior team members have the same benefits and incentives? Do your programs address a diverse range of needs, accounting for factors like location, race, gender, and age? Equitable benefits send the message of appreciation to all employees and instill the feeling of fairness and compassion.

Career Progression

Most employers take pride in hiring ambitious and hard-working employees. Don’t let your corporate structure or practices inhibit that ambition. Employees feel appreciated when they have a clear path for growth and opportunities to step up. From a benefits perspective, this might mean incorporating mentorship programs, education or certification programs, tuition reimbursement, or formal training programs.

Employees should feel appreciated on a regular basis, and not just on Employee Appreciation Day. By making sure you have these five pillars accounted for in your benefits program, you can create a positive culture of appreciation and satisfaction.

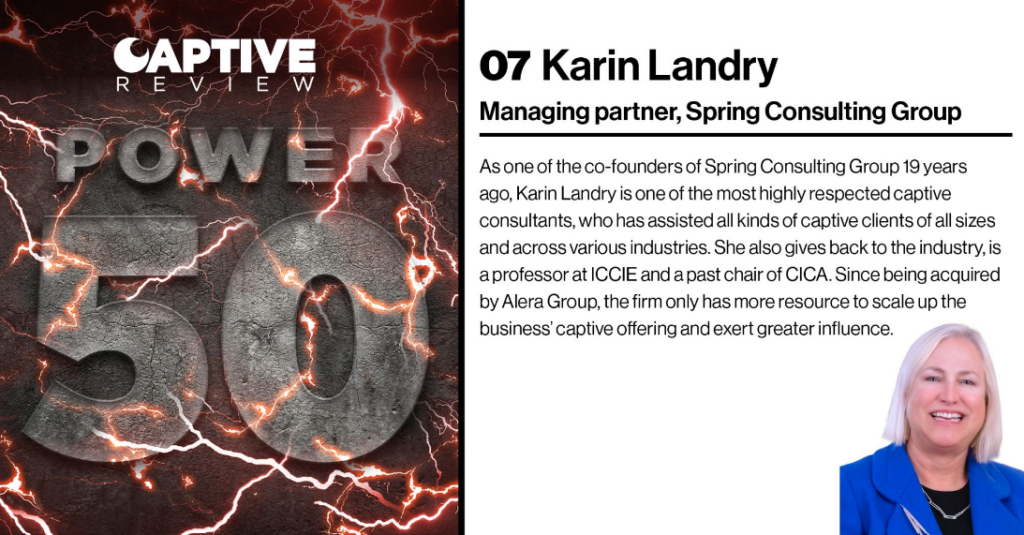

Captive Review releases their annual Power 50, where they showcase top leaders in the captive space. This year, they selected our Managing Partner, Karin Landry, #7. Check out the top 10 professionals here.

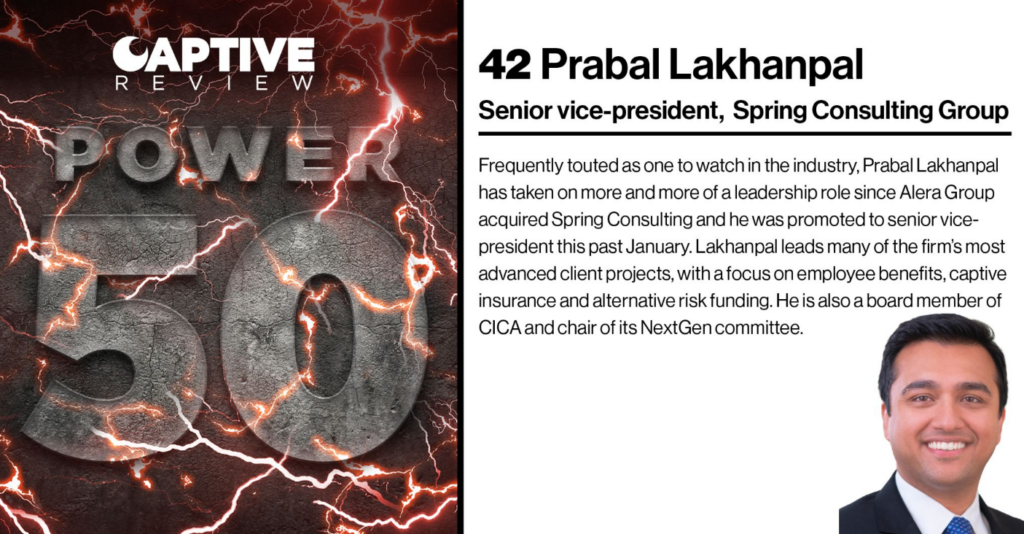

Every year, Captive Review releases their Power 50 list, which spotlights top professionals in the world of captive insurance. This year our SVP, Prabal Lakhanpal was featured on the list at #42. Check out the full article here.

When it comes to Actuarial Services, many people are unclear what it entails. The video below breaks down how actuaries can help cut costs and optimize benefits plans.

Spring Consulting Group provides a wide range of Captive Services when it comes to the Employee Benefits and Property & Casualty (P&C) industries. In this Whitepaper, you can learn more about our captive services and how we approach captive implementation/optimization.

In 2023 we are expecting to see lots of changes when it comes to Paid Family and Medical Leave on both the state and nation-wide level. In this whitepaper, we break down the current landscape of paid leave programs and recommendations for employers to adopt and manage effective paid leave policies.

Title:

Senior Vice President and Co-Founder.

Joined Spring:

I was one of the original founders of Spring (alongside Karin Landry) back in 2004, as a spin out from Watson Wyatt Insurance & Financial Services, Inc.

Hometown:

I was born and raised in Golden Valley, Minnesota (Minneapolis area), but went to college in Wisconsin.

At Work Responsibilities:

I lead our absence management team, and work with employers of all sizes and industries and leading insurance carriers and administrators in the space. I also head up our Spring’s market research surveys and benchmarking.

Outside of Work Hobbies/Interests:

Being outside, going for walks; spending time with family, and of course, watching my kids play basketball.

Fun Fact:

One thing many people don’t know about me is that I actually use to run track in high school and led the 4×100 relay.

Describe Spring in 3 Words:

Interesting work & caring culture, I guess that’s actually 5 but that’s how I would describe Spring. The people all care about each other and have each other’s backs and support each other. We have a motivated team that is eager to collaborate.

Do You Have Any Children?

Yes, I have two beautiful children, my daughter is 17 and my son is 15.

Favorite Place Visited:

Greece, by land and sea! It has to be my favorite because of the history, beautiful architecture and amazing weather!

If You Were a Superhero, Who Would You Be?:

It would be Elastigirl from The Incredibles because her arms are so long and she can hold everybody. She can take care of everything!