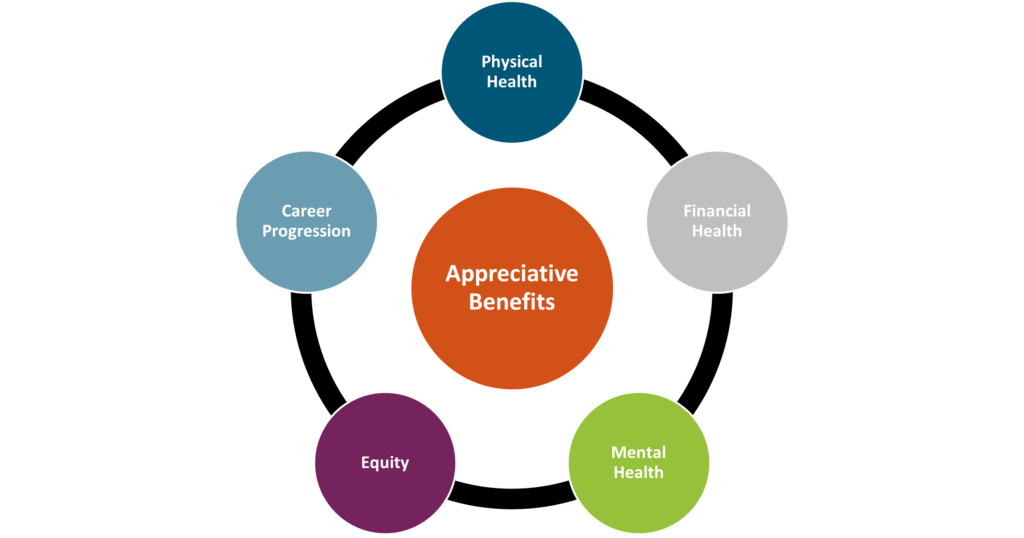

No matter the product or service you’re selling, or the impact your business makes in your community or the world at large, the consensus is that the most important asset an organization has is its people. Our HR and Benefits colleagues know very well that keeping employees happy and engaged (and keeping them in general) is not only makes for a positive atmosphere, but is also a strategic business move. So maybe you’re celebrating Employee Appreciation Day with a grateful shoutout, or a catered lunch, but don’t forget to look at the bigger picture of the precedent you’re setting – whether intentional or not – with your benefits programs.

Physical Health

Beyond the “it’s the right thing to do” mentality, benefits that support employees’ physical health are important for another reason: unhealthy employees will be far less productive, if present at all. Take a look at your health plans to ensure affordability, access, and breadth of care. Components like dental and vision insurance should also be considered here. Beyond health insurance, many companies offer supplementary tools or services that promote physical health such as fitness reimbursements, point solutions for things like diabetes management or musculoskeletal issues, health coaching services, walking challenges, and more.

Mental Health

Mental Health America reported that nearly 20% of Americans were experiencing a mental illness in 2022. The World Health Organization (WHO) states that depression and anxiety cost the global economy approximately $1 trillion every year. While employers cannot solve the mental health crisis, many believe that they do have a responsibility to provide related resources and prioritize employee mental health in some way. At Spring, we recommend tackling mental and behavioral health through the lens of its three most common barriers: cost, access, and stigma. Any programs offered should try and solve for these. For example, does your health plan cover mental health related appointments? In addition, there are a wide range of services available in this area. Some companies bring in yoga instructors on-site. Alera Group provides Spring Health at no cost to employees, which offers complimentary digital therapy sessions, coaching, and other tools. Apps like Calm and Headspace provide guided meditation and anxiety management practices. Paid time off for mental health or built-in “breaks” during the workday, such as designated times when meetings are prohibited, can also help. Simple tactics like demonstrating openness to discussing mental health in the workplace can go a long way to lessen any stigma.

Financial Health

Especially in today’s economy, employees need help saving for retirement, investing wisely, and being financially informed and educated. We also know that financial stress can be related to mental health, so by focusing on financial health you can impact multiple components of employee engagement. At a basic level, leading employers offer a 401(K) or similar retirement savings plan, with an employer match. As a next level, tax-friendly benefits like Health Savings Accounts (HSAs) can be helpful, and there has been a lot of buzz around student debt repayment programs which employers can choose to contribute to or just offer as a voluntary benefit. Other voluntary benefits like life insurance, identity theft protection and short- or long-term disability insurance can contribute to an employee’s financial wellness. Other perks might include financial counseling services and educational seminars.

Equity

Do your employees in different states have access to the same paid leave? To the same reproductive healthcare? To the same disability coverage? Do your executives and your more junior team members have the same benefits and incentives? Do your programs address a diverse range of needs, accounting for factors like location, race, gender, and age? Equitable benefits send the message of appreciation to all employees and instill the feeling of fairness and compassion.

Career Progression

Most employers take pride in hiring ambitious and hard-working employees. Don’t let your corporate structure or practices inhibit that ambition. Employees feel appreciated when they have a clear path for growth and opportunities to step up. From a benefits perspective, this might mean incorporating mentorship programs, education or certification programs, tuition reimbursement, or formal training programs.

Employees should feel appreciated on a regular basis, and not just on Employee Appreciation Day. By making sure you have these five pillars accounted for in your benefits program, you can create a positive culture of appreciation and satisfaction.

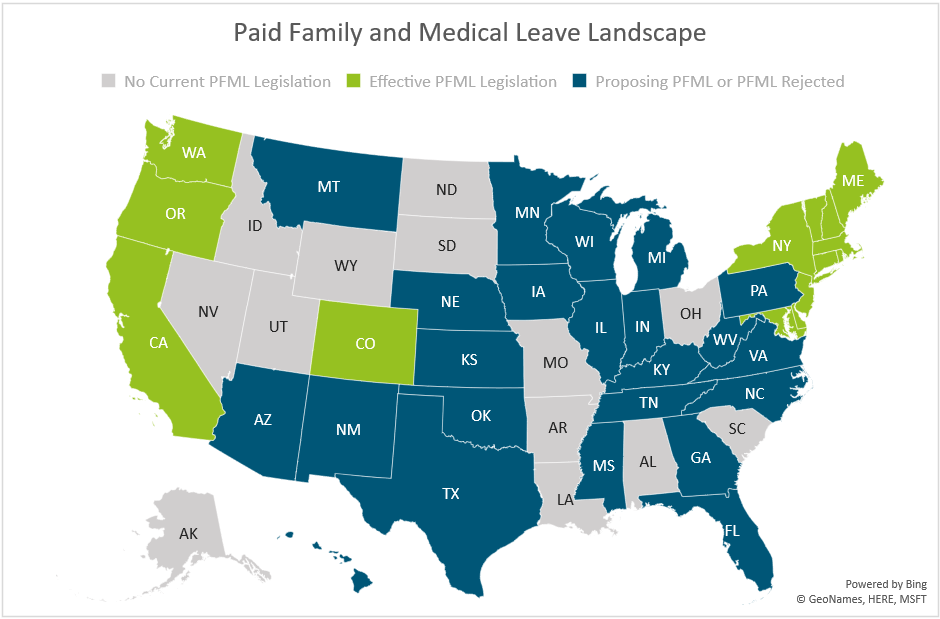

In 2023 we are expecting to see lots of changes when it comes to Paid Family and Medical Leave on both the state and nation-wide level. In this whitepaper, we break down the current landscape of paid leave programs and recommendations for employers to adopt and manage effective paid leave policies.

Title:

Senior Vice President and Co-Founder.

Joined Spring:

I was one of the original founders of Spring (alongside Karin Landry) back in 2004, as a spin out from Watson Wyatt Insurance & Financial Services, Inc.

Hometown:

I was born and raised in Golden Valley, Minnesota (Minneapolis area), but went to college in Wisconsin.

At Work Responsibilities:

I lead our absence management team, and work with employers of all sizes and industries and leading insurance carriers and administrators in the space. I also head up our Spring’s market research surveys and benchmarking.

Outside of Work Hobbies/Interests:

Being outside, going for walks; spending time with family, and of course, watching my kids play basketball.

Fun Fact:

One thing many people don’t know about me is that I actually use to run track in high school and led the 4×100 relay.

Describe Spring in 3 Words:

Interesting work & caring culture, I guess that’s actually 5 but that’s how I would describe Spring. The people all care about each other and have each other’s backs and support each other. We have a motivated team that is eager to collaborate.

Do You Have Any Children?

Yes, I have two beautiful children, my daughter is 17 and my son is 15.

Favorite Place Visited:

Greece, by land and sea! It has to be my favorite because of the history, beautiful architecture and amazing weather!

If You Were a Superhero, Who Would You Be?:

It would be Elastigirl from The Incredibles because her arms are so long and she can hold everybody. She can take care of everything!

the International Foundation of Employee Benefit Plans recently wrapped-up their 32nd Annual Health Benefits + Conference Expo (HBCE) in Clearwater Beach, Florida. The conference brought together healthcare and benefits professionals from a range of industries to discuss leading topics and share expectations for the future. Having heard such positive feedback about the event, Spring was glad to attend, exhibit, and speak at the conference. Below are some of our biggest takeaways.

1) Pharmacy Cost Containment

This year there was a lot of talk surrounding the price of prescription drugs and tactics employers can adopt to help control costs without cutting benefits. There are many factors influencing the high costs of pharmacy drugs, some of which include chronic disease prevalence, the aging population and the growing volume of specialty medications. Below are some of the top sessions focused on controlling Rx costs.

– Representatives from Express Scripts explained the upsides to working with a Pharmacy Benefit Manger (PBM) and how they can help address pharmacy policies in their session titled, “How to Work With Your Pharmacy Benefit Manager.”

– The CEO and Co-Founder of TruDataRx, Cataline Gorla, discussed how comparative effectiveness research (CER) is being used by other countries to decide which drugs work best for specific medical conditions, and how self-insured employers can save money with said data.

2) Addressing Chronic Conditions

According to the Center for Disease Control (CDC), 90% of the nation’s healthcare spending goes towards people with chronic and mental health conditions1. As chronic diseases are very common among the American workforce, employers have started implementing specific benefits and policies to address common conditions, such as diabetes and obesity. Some of the sessions around this topic that we found most interesting include:

– Speakers representing the Nashville Public School System explained how they were able to introduce free resources such as telenutrition and fitness center access to help combat obesity and other health disparities.

– Dr. Mudita Upadhyaya from St. Jude Children’s Research Hospital presented on prevention strategies to address mental health and obesity in a pre- and post-COVID world; and why a mixed approach may be best.

– The Diabetes Leadership Council’s CEO, George J. Huntley spoke on diabetes and chronic disease risk management strategies, including medicines and technology that can help patients manage and prevent the disease.

3) The Future of Healthcare & Benefits

In recent years we have seen a great shift in the healthcare and benefits industry; we saw a great increase in telehealth, mental health resources, new/alternative types of paid leave, including sick leave and more. As we transition to a post-COVID world, we expect the evolution to continue. Below are some of the top trends professionals believe we will face in the coming years.

– Our Senior Vice President, Teri Weber, presented on market forces employers can utilize to meet future absence management challenges. Her session listed techniques employers can adopt to improve day-to-day administration of disability, absence and accommodations.

– In a session titled “Innovative Health Care Models—The Future of Direct Primary Care,” the presenter explained how many employers are changing to value-driving healthcare models to boost access and reduce costs.

– A session titled “Breaking the PTO Mold, Without Breaking the Bank,” reviewed how typical Paid Time Off (PTO) programs can be altered to better support employees’ well-being and financial health.

– The final session of the conference spotlighted how the pandemic has led to an increase in personal, economic and other stressors and has had a drastic impact on mental health, substance misuse and addiction. Attendees were informed on how they can implement workplace solutions that address these issues as well as identify warning signs.

The warmer weather was certainly a bonus, but the insights we gleaned and connections we made were what will keep us coming back to the HBCE conference. We want to thank IFEBP and our fellow colleagues who took the time to share their experience, stop by our booth, and make the energy so positive.

1https://www.cdc.gov/chronicdisease/about/costs/index.htm

Our Senior Vice President, Prabal Lakhanpal wrote an article for the Boston Business Journal on how employers can continue to provide strong benefit packages during a time of high inflation. You can find the full article here.

As seen in the New England Employee Benefits Council (NEEBC)’s blog.

Last year around this time, I gave a year-one progress report on the Massachusetts Paid Family and Medical Leave (PFML) program, as it had finished its first year of paying out benefits to eligible workers. Since then, the MA PFML program has continued to mature and adjust according to experience, and, around New England, Connecticut has had PFML benefits available for one year, and there are related updates from Rhode Island, New Hampshire, Vermont and Maine to report.

Massachusetts: A Year in Review

In fiscal year 2022 (July 1, 2021 – June 30, 2022), the Massachusetts Department of Family and Medical Leave (DFML) experienced1:

– Over 112,500 applications, with 20% being denied

– 59% of applications were related to medical leave, 31% for bonding, and 10% to care for a family member

– Only 32 approved applications for military exigency leave and 7 approved applications to care for a service member

– Claimants aged 31-40 had the most approved claims (40%) and more than 1.5 times as many women had an approved leave (61% of claims), compared to men (35% of claims)

– Average weekly benefits were $793.55 for family leave and $754.84 for medical leave

– Turnaround times from the time the application was submitted to an initial decision was a median of 17 calendar days

– Average duration of leave was 12 weeks, assuming a 5-day work week

– Total benefits paid was equal to about $603 million (an increase of about 245% from FY21 which accounted for January 1, 2021-June 30, 2021)

In 2023, Massachusetts will be updating maximum benefit amounts and reducing total contributions.

– The maximum weekly benefit is increasing to $1,129.82, effective 1/1/2023. This is an increase of about $45 from the 2022 weekly maximum. For any employees who may have leave that runs from 2022 into 2023, the weekly benefit that was determined when leave was approved will continue. The new maximum will not be applied until there is a new MA PFML leave application.

– Contributions, however, will be reduced in 2023. The total contribution is decreasing from 0.68% to 0.63%, for employers with 25 or more covered individuals. The medical leave contribution will be 0.52%, with employers funding 0.312% and employees responsible for up to 0.208%. The family leave contribution will be 0.11%, with employers able to collect the total contribution from employees. Employers with less than 25 employees are not required to submit the employer portion of premium.

The financial earnings requirement was also updated in 2023. Employees must have earned at least $6,000 and 30 times the PFML benefit amount during the base period to be considered eligible for MA PFML.

Connecticut: First Year Activity

Connecticut has now had PFML benefits available for 1 year. During the first six months of the program2:

– Over 44,127 applications, with 40% being denied of those that received a decision

– 44% of approved applications were related to medical leave, 29% for bonding (own child and adoption/foster care), 18% for pregnancy/childbirth, and 9% to care for a family member

– Only 15 applications were approved for family violence, 12 for organ and bone marrow donation, and 2 for qualifying exigency

– Claimants aged 26-41 had the most filed claims (53%) and more than double the number of females applied for leave (28,814), compared to males (14,213)

– Average weekly benefits paid were $562.01

– Average approved duration of leave was 6.79 weeks

– Total benefits paid was equal to about $81 million

– Almost 137,000 businesses have registered with the CT Paid Leave Authority and claim applications have been received from every city and town in the state

Based on the experience in the state in 2022, Connecticut is not making any major changes to the program in 2023. However, the social security contribution and benefit base increased to $160,200 on January 1, 2023, and CT minimum wage increases to $15/hour on June 1, 2023, which will impact benefit and contribution amounts.

Please note that the program has some key differences when compared to MA PFML, such as the availability of leave for organ and bone marrow donation, as well as leave related to family violence. Differences in benefit amounts, leave duration, and eligibility conditions also make it difficult to directly compare CT and MA PFML experience.

Other New England Updates

Massachusetts and Connecticut are not the only New England states to be seeing PFML progress. Rhode Island has an established temporary disability insurance program (TDI), which was the first statutory disability program in the country, established in 1942. In 2014, they became the third state to offer family leave benefits through temporary caregiver insurance (TCI). In addition, the state does not allow private plans, making the model slightly different than other PFML programs in the region. On January 1, 2023, a few updates to TDI and TCI became effective. The state’s taxable wage base increased to $84,000, which will impact the contribution calculation. The benefit duration also increased to 6 weeks, from 5 weeks in 2022. Finally, the financial eligibility conditions claimants must meet increased so that employees must have paid at least $15,600 in the base period or meet the alternative conditions wherein they earned at least $2,600 in one of the base period quarters and base period taxable wages equal to at least $5,200.

A new outlier is New Hampshire’s first-in-the-nation, state-sponsored voluntary plan where NH employers and eligible NH workers can purchase a paid family and medical leave plan through the state’s insurance carrier. New Hampshire selected MetLife as its insurance partner and began paying benefits on January 1, 2023.

Similarly, Vermont spent 2022 developing a voluntary program to be administered by The Hartford, their selected insurance carrier. Beginning July 1, 2023, state employees will be covered under the program, with other private and public employers with 10 or more employees eligible for coverage in 2024, and small employers and individuals able to purchase coverage in 2025.

Maine also made strides in developing the structure of their state mandated PFML program. Maine created a commission to study PFML programs and to propose a PFML model for the state, which kicked off in May 2022. Policy recommendations are expected to be presented to the Legislature in 2023.

Are You Up to Speed?

As the PFML landscape continues to evolve at the local, state and federal leaves, policies need to be monitored on an ongoing basis. Employers should ensure they are compliant with the requirements of each individual leave program, as differences exist between all established paid family and medical leave policies. If any of your employees are impacted by a state PFML policy, organizations should review plans, policies, and processes to confirm they are in line with any legislative changes. To do so, the following checklist can be followed:

– Register in any new states where employees are located, if required

– Ensure contributions are being collected appropriately

– Update employee notices and benefit documentation, as appropriate

– Confirm employee count to determine if any changes to contributions are required

– Review private plan strategies based on previous year experience and changes to contributions

– Renew private plans as appropriate

– Validate company sponsored leave programs coordinate with PFML to the extent possible

If you need assistance ensuring PFML compliance or to assess the optimal plan set up for your organization, Spring’s consultants are happy to help www.springgroup.com

As point solutions for health and benefits continue to pop up, it’s sometimes hard to understand what solution(s) might be most valuable for your workforce. Our “Point Solutions Spotlight” series is meant to hone in on one area of point solutions at a time, so you can make an informed decision. As January is Glaucoma Awareness Month, we thought this month we would spotlight a large potential risk factor for glaucoma: diabetes. A diabetes diagnosis doubles your risk for developing glaucoma1, among other vision impairments.

Executive Summary

Diabetes is one of the most common chronic health conditions in the US; in 2020 it was estimated that 34.2 million adults in the US were diagnosed with diabetes (roughly 11% of the population)2. This number is inflated even further when considering those who are undiagnosed or have prediabetes; in fact, the CDC believes one in three Americans will develop some form of diabetes in their lifetime3. Diabetes is caused by both genetic and lifestyle factors, some of which include weight, diet, and physical activity.

Employees diagnosed with diabetes often see their condition affect their work life, in the form of both productivity and absence, because some of the most common symptoms include urinating often, extreme fatigue and a constant feeling of thirst and hunger (even while eating). According to the American Diabetes Association (ADA) individuals diagnosed with diabetes spend on average $16,752 per year on medical expenses, $9,601 of which is attributed to diabetes (2.3 times more than spending by those without diabetes).

What is the impact on healthcare spending?

Diabetes is the most expensive chronic condition in the US, with an estimated $1 in every $4 of healthcare spending going towards diabetes-related care. Other top healthcare cost drivers include heart disease, cancer and musculoskeletal (MSK) conditions. In 2017, diabetes healthcare costs were $327 billion, with $237 billion accounting for medical costs and $90 billion in reduced productivity costs4.

According to the ADA, most diabetes medical spending goes towards:

- Hospital inpatient care (30% of the total medical cost)

- Prescription medications [including insulin] (30%)

- Anti-diabetic agents and diabetes supplies (15%)

- Physician office visits (13%)

The ADA also found diabetes leads to many indirect costs (often at the helm of employers):

- Increased absences ($3.3 billion)

- Reduced productivity while at work ($26.9 billion) for the employed population

- Reduced productivity for those not in the labor force ($2.3 billion)

- Inability to work because of disease-related disability ($37.5 billion)

- Lost productive capacity due to early mortality ($19.9 billion)

Our client, edHEALTH, is a consortium of 25 educational institutions that came together with the goal of reducing health and benefits costs for their employees while enhancing offerings at the same time. They consistently review the data, including diabetes, to find ways to help bring the costs down for their member-owner schools.

What solutions exist?

As diabetes has been the top chronic illness in the U.S. for some time, the distribution of costs for care (mostly towards inpatient care and prescription medications) have not changed drastically over time. As inflation continues to increase and many organizations are seeing healthcare costs rise, savvy employers are moving towards alternative models for addressing diabetes.

Employers who see a substantial impact of diabetes costs on their claims, may want to consider alternative treatment or lifestyle benefit offerings. Some of the top alternative solutions include:

- Diabetes Prevention Programs (DPPs)

- Diabetes management point solutions programs, some of which provide:

- Education of risks and potential treatments associated with diabetes

- Glucose testing/monitoring supplies and insulin pumps

- Apps that track blood sugar levels, weight, calories, and other metrics

- Digital platforms to connect employees directly with doctors

- One-to-one coaching

- Meal planning/nutrition goals

- Mental health resources

- Inpatient care coordination

- Health and wellness programs/initiatives

- Gym memberships

- Weight-loss programs

- Providing healthy food options (in the cafeteria, kitchen, vending machines, etc.)

- Mental health benefits

- Financial benefits

- To help control diabetes costs for employees

As an important note, employers may ask employees about health information following a job offer regarding diabetes, including how long said employee has had diabetes, if they need any work accommodations and if they need assistance during a low blood sugar episode. However, under The Americans with Disabilities Act (ADA), employers cannot discriminate against qualified individuals with diabetes. If your organization is seeing high diabetes healthcare costs, we suggest you revisit your healthcare plan(s) and/or adopt one or more of the alternative solutions above.

What should I do as an employer interested in a diabetes management program?

Employers must first understand the costs and trends associated with diabetes within their population/workforce. If diabetes is driving costs (medical, pharmacy and productivity), employers should consider alternative programs that align with their specific problem area(s). Identifying these patterns is key to understanding the need for tailored approaches such as preventative programs or introducing health and well-being benefits.

From there, market research will be necessary to understand pricing and select a vendor with the best program for your population. Spring’s consultants are here to help with market research, claims and data analysis, and/or a Request for Proposal (RFP) process so that you find a solution that best meets your organizational needs.

1https://www.smarteyecare.nyc/blog/the-link-between-diabetes-and-glaucoma

2https://www.singlecare.com/blog/news/diabetes-statistics/

3https://bit.ly/CDCchronicdisease

4https://diabetesjournals.org/care/article/41/5/917/36518/Economic-Costs-of-Diabetes-in-the-U-S-in-2017

When Congress passed the Consolidated Appropriations Act of 2021, this omnibus appropriations bill included the No Surprises Act (NSA). In 2022, much of the NSA focused on implementing consumer protections surrounding surprise medical bills after receiving emergency medical care. This was a big win for patients who were inadvertently receiving out-of-network care and billed non-negotiated rates in emergency situations where in-network providers and hospitals were leveraging out-of-network services and balance billing patients. The NSA specifically targeted air ambulance services and identified certain non-emergency services where notice and consent requirements must be satisfied for balance billing.

Two components of the NSA received much less fanfare and were not implemented on the original timeline. This includes: (1) requirements for providers to make good faith estimates (GFE) of charges for services within three hours (if immediate) or three days (if scheduled) and (2) the requirements around Advanced Explanation of Benefits (AEOB). The Department of Health and Human Services (HHS) delayed enforcement of these requirements for insured individuals, originally slated for plan years beginning on or after January 2022, given the lack of infrastructure for providers to transmit the necessary data on the GFE, which also directly impacted the ability to supply AEOBs.

The Centers for Medicare and Medicaid Services (CMS) and HHS asked for public comment related to the GFE and AEOB requirements. Comments were due November 15, 2022, and we expect clarifications or revisions to the regulations based on the feedback received. Implementation of the GFE and AEOB will demonstrate the fragmented health care structure that currently exists and that health plans, including self-insured plans, need to carefully monitor the impact.

GFE will impact every provider. Small, independent practices will likely experience the biggest disruption, which may translate into further consolidation. In addition, most services require coordination between multiple providers and ambiguity exists around ownership of those GFEs.

Although GFEs are a provider responsibility, health plans – including self-insured employer plans – are not immune to these pending guidelines. Compliant AEOBs must be supplied by health plans and one component is information related to the GFE. Therefore, information not only needs to be shared from providers to patients, but also from providers to health plans, so that it can be included in the AEOB.

In short, the No Surprises Act will likely be full of surprises in 2023 as CMS and HHS begin to address the following questions:

- How will data be exchanged (i.e., FHIR-based API or other means)?

- Is electronic notification sufficient, or will hard copy documents be required?

- How much time will be given for compliance (i.e., system updates, IT development, testing, printing, production, etc.)?

- Will any self-service options exist

As additional guidance is released and these questions are answered, we look forward to sharing our thoughts and recommendations in accordance. In the meantime, please reach out with questions related to the No Surprises Act, AEOB Compliance, or anything related.

Paid Family and Medical Leave continues to be a confusing point for employers, compounded by new legislation being proposed at a seemingly constant pace. As leaders in the disability and absence management space, we are dedicated to staying on top of updates around PFML, among other areas. After a busy year in that regard, with another on the horizon, we wanted to share this brief overview.

In 2022, there was more movement towards state PFML laws being passed after decreased activity in previous years, largely due to the COVID-19 pandemic. For example:

- Delaware and Maryland both passed laws establishing PFML programs

- Virginia established insurance rules, allowing carriers in the state to provide insured PFML plans to clients

- Colorado and Oregon began collecting contributions on 1/1 and have been working to ensure they are prepared to do so, while establishing other rules for the effective administration of PFML

- New Hampshire worked to develop their voluntary PFML program selecting MetLife as its insurance partner and began coverage on 1/1/2023

- Vermont selected The Hartford as its insurance partner for its voluntary PFML program

- Maine made strides in developing the structure of their state mandated PFML program

In 2023, we expect continued activity. Pennsylvania and Michigan have outstanding proposals for PFML, which will likely be decided upon in 2023, one way or another. Additional states may also put forward proposals in upcoming legislative sessions.

In addition, and as seen in the updates below, states with existing legislation continue to make adjustments to their PFML programs. Adjustments to contributions and benefits are typically expected, most commonly, but not always, at the end of the calendar year.

The map below shows a summary of states with existing PFML legislation and programs in place, those who have proposed legislation without it being passed, and those that have not had any activity related to PFML in recent years.

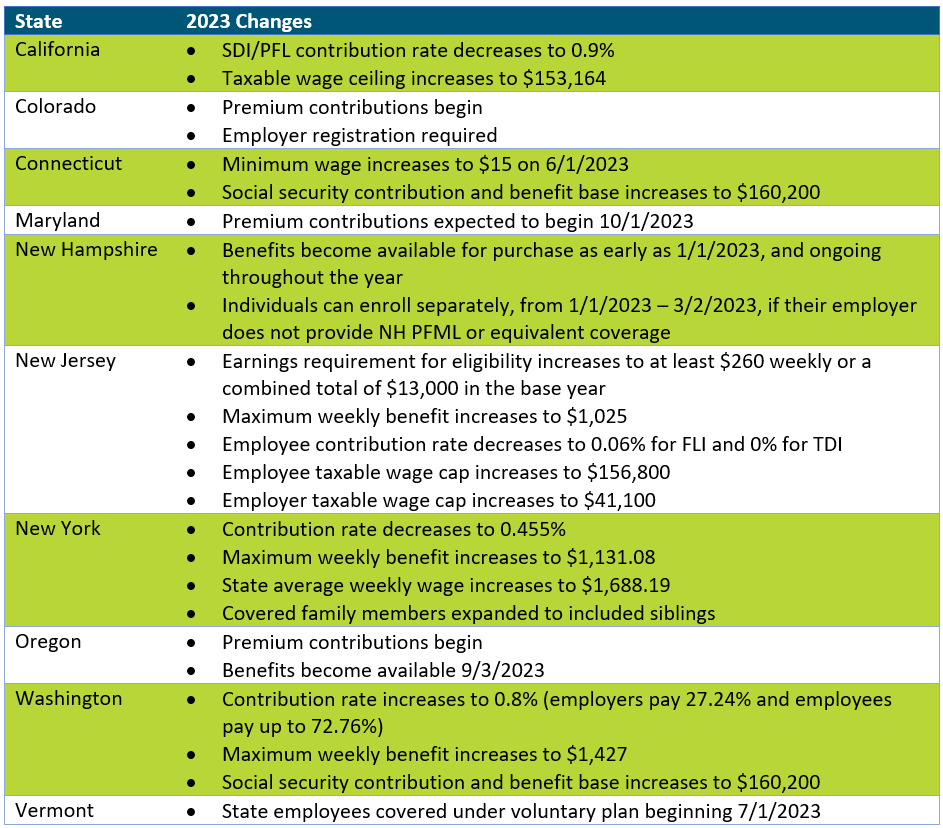

Massachusetts

In 2023, Massachusetts will be updating maximum benefit amounts and reducing total contributions.

The maximum weekly benefit is increasing to $1,129.82, effective 1/1/2023. This is an increase of about $45 from the 2022 weekly maximum. For any employees who may have leave that runs from 2022 into 2023, the weekly benefit that was determined when leave was approved will continue. The new maximum will not be applied until there is a new MA PFML leave application.

Contributions, however, will be reduced in 2023. The total contribution is decreasing from 0.68% to 0.63%, for employers with 25 or more covered individuals. The medical leave contribution will be 0.52%, with employers funding 0.312% and employees responsible for up to 0.208%. The family leave contribution will be 0.11%, with employers able to collect the total contribution from employees. Employers with less than 25 employees are not required to submit the employer portion of premium.

Other State Updates

Other states have made updates to their programs effective January 1, 2023, unless otherwise noted below. Some states may make changes off calendar year (e.g., District of Columbia, Rhode Island), which are not included if they have not yet been released.

Recommended Approach

Employers should review their PFML plans, policies, and processes to confirm they are in line with any legislative changes. To do so, the following checklist can be followed:

– Update employee notices and benefit documentation, as appropriate

While formal notices may not always be required, especially if contributions are decreasing, communicating updates to employees is recommended, especially if the change will impact their pay. Most states provide sample notices that can be customized to fit an employer’s needs. Keep in mind that there may be timing requirements in place (e.g., 30 days in advance).

– Confirm employee count to determine if any changes to contributions are required

Some states require contributions from both employers and employees however do not require employer contributions from “small” employers. This definition of small varies by state (e.g., less than 25, less than 50 employees). Confirming the total number of employees will verify the contributions being remitted to the state are accurate.

– Review private plan strategies based on previous year experience and changes to contributions

Whether or not a private plan is an ideal method for an employer to provide PFML to employees may vary from year to year. This can largely be based on the cost of a private plan versus going with the state plan, but the employee experience also plays a major role. From a cost perspective, a private plan, in most states, will be based on that employer’s leave experience. If an employer has high PFML incidence rates, insurance carriers or TPAs may charge more than is required to be paid under the state plan. From an employee experience perspective, having to file PFML claims to the state and what are often concurrent disability, FMLA or other leave claims to the employer or its vendor partner, can be confusing and require more effort for both employees and employers. While the driving factors will vary by employer, both cost and employee experience should be considered.

– Renew private plans as appropriate

When a private plan is in operation, states may require these be renewed at certain intervals. Massachusetts, for instance, requires this annually, while Connecticut only requires it every three years, unless a material change to the plan is made. Employers should review the timing of their private plan approval and guarantee it is up to date.

If you need assistance ensuring PFML compliance or assessing the optimal plan set up for your organization, Spring’s consultants are happy to help.