This Earth Day, we wanted to highlight the effects of climate change and natural disasters on the property & casualty insurance industry. Check out the infographic for a quick glimpse of where things stand.

Sources:

1 Alera Group’s 2023 P&C Market Outlook + Commercial Property Update

What are the biggest trends or developments we should expect to see this year in the Property and Casualty (P&C) market?

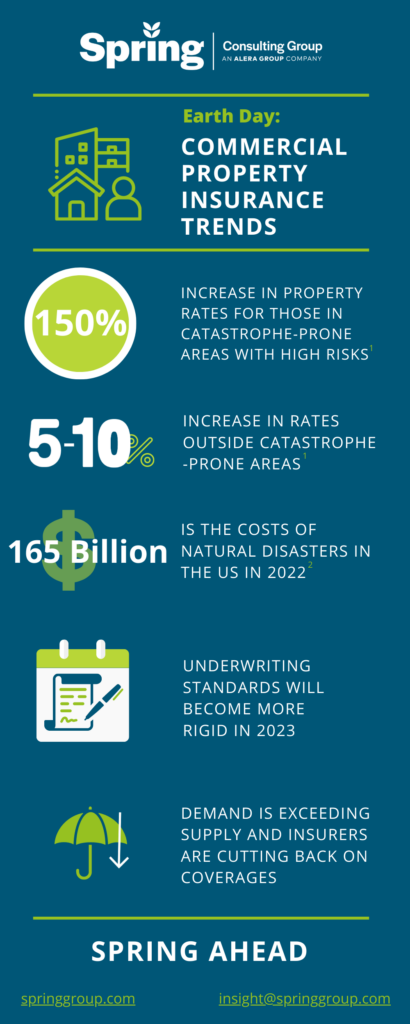

Like many other industries, inflation has been top of mind for risk managers, insurers, and P&C professionals. McKinsey & Company estimated that inflation increased the cost of P&C claims by $30 billion in 2021,1 and it continues to be a primary concern across P&C lines. Property insurance is being hit hard this year. Hurricane Ian alone is expected to cost insurance companies over $60 billion.2 In combination with other recent catastrophic events (CATs) and construction cost inflation, this is driving substantial rate increases and higher underwriting standards for property policies. Inflation in auto costs and increased driving are also forcing insurers to respond with higher auto rates this year. So, cost-control practices will continue to be a main focus throughout 2023, both for insurers and businesses.

What impact is inflation having on the P&C market? Where is it hitting the hardest?

In the current hard market, we are expecting to see price increases across all lines of business, with an overall average increase of 9.3% in rates.1 Some of the top business lines being impacted include cyber, commercial property and personal lines/private risk (including private auto).

Following Hurricane Ian, we saw drastic increases in property insurance rates, with properties with poor risk quality seeing increases of 25% all the way up to 150% at the start of 2023.3 The number of natural disasters and level of exposure have been trending up over time, and costs are compounded by the need to rebuild with inflated prices and strained supply chains. According to NOAA National Center for Environmental Information, natural disasters cost the U.S. over $165 billion in 2022.4

When it comes to cyber, one of the toughest lines of business to write, we expect rates to increase as much as 50% for more complicated risks and 15% for simpler risks.1 This is less a result of inflation and more like growing pains for a newer market. As new risks continue to emerge and underwriting practices strengthen in cyber, it is difficult to predict how significantly inflation will influence costs.

Personal lines/private risk (including auto and homeowners insurance) rates are expected to increase almost 13% on average this year, with automobile rates seeing increases of 8-10% across the nation.1 Although Hurricane Ian and CATs dominated headlines in 2022, of the 15.5% increase in net losses across all business lines, private auto liability represented the largest sector in net incurred losses.5 Supply chain issues that drove up the prices for vehicle repairs and replacement had a direct impact on auto insurance claim severity and created a rate increase need for auto insurers to cover the cost increases. For many companies these rate increases are coming in conjunction with increased underwriting scrutiny, forced up retentions, and coverage reductions.

Workers’ Compensation is an exception to the norm this year. In spite of continued inflation, rates are expected to remain unchanged or slightly drop in 2023, with stable coverage options and underwriting practices. Employment Practices Liability is also looking favorable for buyers in 2023, with modest rate increases of 7% on average. Finally, Surety is also expected to see average increases just above 7%,1 but will face increased underwriting scrutiny with potential for larger rate changes on a case-by-case basis.

Geography is an important factor as well, and not just related to climate. For example, medical professional liability severity trends have increased, but this varies significantly by region. Some states are seeing double digit severity trends and rate increases while others are experiencing very modest increases. Differences in litigiousness and jury awards drive much of these state-by-state differences.

While most buyers are seeing rate increases and some reductions in coverage, high-risk clients are affected the most by continued inflation and other cost increases. This includes businesses with adverse loss histories, located in CAT-prone areas, or with frame construction buildings. Unfortunately, we are not seeing an influx of new players or investment to mitigate rising rates.

When looking at the industry level, Alera Group reports that the two sectors with the most unfavorable market situations are nonprofit organizations and the hospitality and gaming sector. Although nonprofits don’t make up a large portion of organizations in the U.S., they often require specialty insurers which can be costly and hard to find. Nonprofits are also often targets for cyberattacks and face unique underwriting processes that differ from other industries. The industry most impacted by inflation and unfavorable market conditions is the hospitality and casino industry where we expect to see increases in rates, reduced insurer options, and stricter underwriting processes across cyber, employment practices, general liability, property and umbrella.

In wake of recent natural disasters, what’s the outlook for property insurance underwriting and rates? On a practical level, what should buyers expect?

Property rates remain high and are expected to remain high for a while. Hurricane Ian caused big disruptions for property reinsurers, who in turn are pushing carriers for better valuation and stricter underwriting — especially in catastrophe-prone areas. As for how this will realistically play out, buyers may see fewer coverage options and new requirements like recent appraisals, insurance-to-value increases, engineering reports and complete applications. More underwriting processes will also focus on fire suppression systems, difficult-to-place risks and limits on high-rise structures.

According to Alera Group’s P&C Market Outlook, cyber liability pricing is expected to increase by 15% in 2023. What do you think this says about the market and what can organizations do to control their spend?

The cyber market is still relatively young and new risks can emerge quickly. Although rates are expected to increase by 15% on average for the simpler risks in 2023, more complicated cyber risks will see increases as much as 50%, often with difficult underwriting processes. Terms and conditions are changing to better clarify challenging coverages, resulting in longer underwriting processes. Employers and buyers of cyber insurance should ensure they are working with experienced underwriters and that they properly understand the specific cyber risks associated with their business so they can prioritize coverage selections.

Are there any emerging P&C lines that will take the spotlight in the years to come? What about in the captive space?

I cannot say for certain we will see completely new lines of business emerge in the next few years in the P&C market. But I do expect to see changes in coverage within different lines of business, particularly as our economy evolves and new technologies and products are utilized by both individuals and commercial industry. Artificial intelligence and other product innovations are expected to have an impact on both frequency and severity of loss outcome and will influence actuarial pricing indications for various insurance products.

I think captives will continue to emerge as a critical part of the ecosystem. As coverage capacity in lines like commercial property goes down or as new risks emerge in lines like cyber, captives offer organizations new options for layering the coverage they need at a price that truly reflects their own loss history and level of exposure. Captives are able to fill in the coverage gaps in cases where the commercial market has yet to come up with a competitive solution. This happened for cyber risks about a decade ago.

How are actuaries poised to help organizations and risk managers tackle some of the challenges mentioned?

Actuaries specialize in quantifying risks using statistics, whether for a business or an insurer or an entire industry and using that information to manage risks in a cost-effective way. This runs the gamut from reviewing a company’s loss history and current insurance policies to informing better choices in the commercial insurance market, all the way to setting up a captive insurance company tailored to the needs and experience of a specific business. In an environment like today with rising premiums and reductions in capacity and coverage options happening for many P&C lines, actuaries can provide organizations with tools and a higher level of confidence around managing their risks and their costs effectively. As an example, actuarial proforma financial models can be leveraged in a captive solution and aid a company’s decision-making around the appropriate balance between retaining risk and utilizing available market options to transfer risk in a cost-effective way.

The pandemic had certain influences on insurance underwriting. Have we transitioned past these pandemic issues yet?

Court room closures, significant reductions in vehicles on the road, delayed healthcare surgeries and procedures and other changes at the onset of the pandemic had a big impact on the underwriting experience of insurance companies for most property and casualty lines of business. As one would expect, when our economic engine slows the frequency of claims also does. As we are now well past these issues and our economy is mostly back up and running, we are now working through other, likely temporary issues that are currently impacting the underwriting experience within the commercial market and driving the need for rate increases. We are certainly seeing this in the auto insurance market. After over a decade of low treasury yields and a low inflationary environment, we are now in a high inflationary environment for personal lines auto. Supply chain issues during the pandemic resulted in significant increases in vehicle costs and have resulted in rising auto claim severities and the need for auto rate increases in the market.

Any final thoughts on the P&C landscape?

It’s a difficult year for property and auto costs, and cyber risks continue increasing. Some of the bottom-line impacts of these changes are unavoidable, but rate and coverage changes in the commercial insurance market are also driven by broad industry patterns that might not apply to a specific organization. I expect to see more businesses taking a close look at their own risk profile and exploring all of their options to close coverage gaps and take advantage of alternative risk funding structures when appropriate.

1 Alera Group’s 2023 P&C Market Outlook

2 https://wusfnews.wusf.usf.edu/economy-business/2022-12-01/hurricane-ian-is-expected-to-drive-more-property-insurers-out-of-business

3 https://www.businessinsurance.com/article/20230104/NEWS06/912354660/Some-rates-will-stabilize-less-optimal-risk-profiles-will-see-hikes-

4 https://www.climate.gov/news-features/blogs/2022-us-billion-dollar-weather-and-climate-disasters-historical-context

5 S&P Global Market Intelligence, March 2023

Captive Review has released a Q&A featuring our Chief Property and Casualty Actuary, Peter Johnson, where he explains the impact of inflation on insurance and risk management practices and how how it intersects with captive insurance. Check out the full Q&A here.

Spring Consulting Group provides a wide range of Captive Services when it comes to the Employee Benefits and Property & Casualty (P&C) industries. In this Whitepaper, you can learn more about our captive services and how we approach captive implementation/optimization.

Last week we wrapped up Business Insurance’s 2023 World Captive Forum (WCF) in Miami, FL. This year’s conference brought together hundreds of stakeholders in the captive space to network and discuss leading trends in the industry. As a member of the advisory board, I’m glad the event was such a success; below are some of the topics I found most prevalent during this year’s conference.

1) Captive Updates

When it comes to captive regulations, we have seen many changes in just the last year. With the growth and development of different domiciles all around the world comes new regulations to which captive owners and employers must adhere. Below I have included a couple interesting sessions that explain how regulations surrounding captives have changed across the globe.

– Government insurance representatives from North Carolina, Vermont, Oklahoma, Bermuda and Michigan discussed trends, best practices and laws impacting the captive industry (and their respected domiciles).

– As Latin America has been growing their position in the captive space, a session featuring the Official Advisor for Latin American Affairs from the Government of Bermuda spoke about current LATAM trends and what we can expect to see from the region moving forward.

2) Cyber Captives

Although writing cyber liability coverage into a captive is not a new practice, it is still nowhere near as common as placing medical stop-loss or property & casualty lines into a captive. This year cyber coverage was a hot-button topic at the conference and will most likely continue to be, as cyber attacks continue to pose substantial risks.

– In a breakout session titled “Cyber Captives” a group of risk experts discussed current trends in cyber insurance and the limitations for captive coverage in cyber.

– In a session titled “Secrets Cyber Criminals Don’t Want the Insurance Industry to Know”, the CEO of BlackShield Cyber, Dioly Alexandre, explained how cybercrime has changed over time and what insurance companies need to do to keep up.

3) Healthcare & Captives

Whether an employer in the retail space is looking to use a captive to fund health benefits, or whether a hospital organization is leveraging a captive for its medical malpractice and other unique liabilities, captives and healthcare have always been closely intertwined. At WCF this year some highlights of this dynamic included:

– Spring’s Managing Partner, Karin Landry, presented on trends in medical stop-loss (MSL) and how this tactic can help employers proactively manage healthcare costs and lessen the impact of catastrophic claims. The discussion included a deep dive into what is driving upticks in healthcare costs; walk-throughs of case studies illustrating MSL advantages, including an overview of Canon USA’s captive story; and a detailed explanation of Medical Expense Cost Containment (MECC) and how it comes into play.

– The first session of the final day reviewed implications of medical malpractice coverage following the Supreme Court’s decision on abortion services and best practices for healthcare providers.

– In the session “Global Medical Claims Developments – Covid-19, Hyperinflation, Musculoskeletal and Mental Health,” the panelists discussed how captive managers should address specific medical conditions and unusual medical claim patterns.

4) The Future of Captives

Although nobody knows for certain the future of the captive industry, we are seeing various patterns that suggest we will see many changes to come. Aside from new domiciles and new types of coverages, we are also seeing different approaches when it comes to current captive practices.

– In a session on “Hybrid Captives,” I presented on innovations in the property & casualty market that allow captives to more meaningfully control property exposures and premiums.

– As a newer member to the World Captive Forum Advisory Board, I was joined by University of California’s Karen Hsi in a roundtable for younger professionals entering the industry, including a discussion of what the next generation of talent is looking for and how they can get themselves on a promising career trajectory.

– As diversity, equity, and inclusion (DE&I) is a current top priority for many companies, this session discussed how by reinvesting underwriting profits, captive programs can be used to finance DE&I strategies to meet the needs of a diverse workforce.

Getting a break from Boston winter was a plus, but the ability to reconnect with industry leaders and collaborate on strategies was the real draw. We are excited to see what the World Captive Forum holds in store for us next year and we will continue to keep you up-to-date with developments in the captive space.

Following Business Insurance’s 2023 World Captive Forum, an article was written about our SVP, Prabal Lakhanpal‘s session on how captives can be a solution to the changing property insurance market. During which he was quoted on tactics employers can take to help control coverage gaps. Check out the full article here.

As seen on Alera Group’s Insights Page

In the cyclical market for Property and Casualty Insurance, we are more than a year into hard-market conditions, leading growing numbers of businesses to consider alternative risk funding. That, in turn, has created an abundance of work for insurance actuaries and Captive Insurance consultants.

OK, that’s a lot of insurance speak for one paragraph. Let’s unpack:

— A hard market for insurance is characterized by a rise in rates, a reduction in options for coverage, heightened scrutiny by policy underwriters and reduced carrier capacity for coverage limits. A combination of catastrophic weather events and so-called “nuclear verdicts” in liability lawsuits — as well as the cyclical nature of the Property and Casualty (P&C) Insurance market — were the driving forces behind the hardened conditions before the onset of COVID-19, and the pandemic exacerbated matters. Rate increases have leveled off to some extent in 2022, but, in general, most conditions in the market remain unfavorable to consumers.

— Alternative risk funding — also known as alternative risk financing or alternative risk transfer — is a mechanism for providing coverage by means other than commercial insurance. Types of alternative risk funding include Captive Insurance programs, in which a business or group of like businesses creates and funds its own private insurance company to cover one or more risks in the realms of both P&C and employee benefits. Workers’ Compensation, General Liability, Auto, Professional Liability and Medical Stop-Loss are the more common coverages to start with when insuring through a captive, but captives often expand into a funding mechanism for many of an organization’s other lines of insurance, including Cyber and Umbrella (also known as Excess Liability Insurance).

— Insurance actuaries use math, statistics and financial models to analyze the cost of risk and determine how much money a company should pay to protect itself against risk. All insurance carriers employ actuaries to help set policy premiums and limits. Some insurance agencies work with actuaries to negotiate policy details with carriers or, in a captive arrangement, to determine a premium that will cover claims and, in the long term, reduce the insured’s total cost of risk. Captives have the advantage of also building up retained earnings over time and allowing companies to take on more risk, generating additional insurance cost savings for the parent. Among multiple P&C capabilities, actuaries who work with or for an agency also educate clients on the cost of risk and how to manage it.

Now that we’ve cleared that up, let’s talk about the role of an actuary in managing the cost of risk and protecting your business with a customized insurance program — whether you’ve chosen to pursue alternative risk funding or not.

Why an Alternative Solution? And Why Now?

Business leaders know all too well about the hard market for Property and Casualty Insurance. Just as the pandemic began to wane early in 2022 and there were some signs of casualty rate increases leveling off, Russia’s invasion of Ukraine escalated supply-chain disruption and fuel shortages, accelerating the rise in economic inflation. Damage resulting from Hurricane Ian only made matters worse, of course, driving reinsurance — insurance for insurers — into what the Bank of America termed a “true hard market” of its own, with rising costs getting passed on to consumers. These issues have led to overall increases in U.S. P&C industry combined ratios over the past few quarters, sparking further rate increases for certain lines.

It’s no wonder more organizations are looking at captives and other alternative risk-funding solutions.

“Overall, between 2017 and 2021, captives added $4.3 billion to their year-end surplus while returning $5.8 billion in stockholder and policyholder dividends, representing $10.1 billion in insurance cost savings over purchasing coverage from commercial market third parties.”

“The number of U.S. captives continues to rise, although the growth of captive formations was tempered by the onset of economic uncertainty resulting from the pandemic, as well as ongoing scrutiny from the IRS and greater regulatory and reporting requirements.”

“However, these adverse conditions can serve to highlight the benefits of the captive segment and provide businesses an incentive to establish them,” said Fred Eslami, associate director, AM Best.

“‘This current environment allows captives to customize coverage for risks that may be uncommon or difficult to write or place in the standard market,’” Eslami said.

The growth in Captive Insurance has led to an increasing willingness on the part of carriers to work with captives and regard them as partners rather than threats, increasing options for captive solutions. And even if an organization in the end chooses to forgo alternative risk funding – either for an entire P&C program or for individual coverages, such as cyber or commercial umbrella – simply exploring an alternative and having it as an option can improve its position in the insurance market.

Actuary Capabilities: Your Data, Your Future

For insurance agents and brokers, designing an insurance program tailored to your industry and company is as much art as it is science. Working with an actuary enables you to incorporate greater amounts of empirical evidence into evaluating risks and determining insurance solutions: Here’s what the numbers demonstrate about your situation now, and here’s what our analysis shows about how you’ll perform using this solution.

While any good broker will work to design an insurance program customized for your business, a broker working with an actuary will be especially well-equipped to design a solution tailored to your unique needs and goals. Among the key issues an actuary can help brokers work through are:

- Determining appropriate retention/deductible levels to help the client reduce the total cost of risk;

- Estimating client retained unpaid claims liabilities at quarter/year-end;

- Estimating carrier letter-of-credit need for a large deductible program;

- Estimating possible retained loss outcomes at various confidence levels;

- Performing a captive feasibility study.

Many brokers work in silos, taking a vertical approach in evaluating risk based on industry. Actuaries generally don’t distinguish by industry; they analyze across various industries, focusing on each individual client’s loss history (including frequency and severity), claim status, policy details, exposures and risk-control program before determining financial projections for the organization. Taking the long-term view allows for consideration of fluctuations in company and market performance over a period of time, and increases the likelihood of long-term savings and profits.

Optimizing Your Insurance and Benefits Solutions

As companies grow, they generally reach a point where their claims experience is predictable across one or more lines of coverage. Able to determine such predictability, an actuary can then help you:

- Minimize your total insurance spend, directing more money to the coverage your business needs the most.

- Reduce spending on the risks you have under control. This is where alternative risk funding becomes viable.

If you’ve reached the point where your business is paying, say, $100,000 to $250,000 in annual premium, a group captive might be the best solution because you probably aren’t yet structured appropriately to meet the insurance tests required to form a single-parent captive and the economies of scale may not be there for a single-parent captive solution. In such a case you may need to diversify your risk with other organizations (heterogeneous or homogeneous) — in a group captive or in a shared-risk pool solution utilizing reinsurance — for at least the time being.

The bigger, more complex, more diversified a company becomes, the more a fully funded, single-parent captive emerges as an optimal solution in which the business is insuring only its own risk. A single-parent captive also allows for more coverage flexibility and transparency than a group captive program. Quite often, both benefits and P&C risks are insured by a single-parent captive.

What drives the decision to move from traditional, carrier-based insurance to a captive program is savings and, ultimately, return on investment (ROI). How? By moving expenditures that create carrier profits into the captive solution. Captives are highly efficient, with very low expense ratios, unlike carriers. Free from providing a carrier with underwriting income and investment income on held reserves, you’re able to retain this income to ultimately generate a profit and facilitate an insurance mechanism that competes with the commercial market.

An Organization-Focused Approach

In taking an organization-focused approach toward financial analysis, actuaries look not only at funding for Property and Casualty Insurance but also at spending on employee benefits. Most captive insureds will see annual savings between 10% and 40% for premiums that flow through a captive instead of the commercial market.

As we approach the end of the year, Alera Group invites you to the final event in our 2022 Engage series of employee benefits webinars, A Look Ahead to 2023: Hot Topics and Trends. Join us on Thursday, December 15 as we discuss benefits financial officers and HR professionals need to think about now — including alternative solutions — as they plan for the year ahead.

ACCESS ALERA’S WEBINAR HERE

Captive International has released the winners for the 2022 US Awards. Spring is proud to announce that our company and our Managing Partner, Karin Landry were selected as winners for Best Feasibility Study Firm and Best Feasibility Study Individual (respectively). We were also highly commended for Best Actuarial Firm, Best Individual Feasibility Study (Prabal Lakhanpal) and Best Actuary (Peter Johnson).

A (Brief) VCIA Session Recap

I had the pleasure of speaking at Vermont Captive Insurance Association (VCIA) Annual Conference last week, joined by two colleagues with impressive backgrounds. Jeff Caudill, Director of Risk Management at Haskell and a client of Spring’s, and Mary Ellen Moriarty, Vice President, Property & Casualty at College Insurance Company (EIIA) joined me to discuss different ways that captives can be used to tackle the hard market hurdles we’re currently facing in the insurance industry.

With myself as the moderator and consulting actuary, Jeff representing a brand new single parent captive, and Mary Ellen representing a veteran captive, it was a well-rounded panel that pulled in multiple perspectives.

The Clouds Behind the Hard Market

This visual does a great job at illustrating the many challenging atmospheric effects in the insurance air right now, particularly on the property & casualty (P&C) side of the fence (no pun intended). With Mary Ellen representing the higher education space, we felt it important to highlight unique risks that colleges and universities are grappling with, in addition to the other complicating factors (or clouds) we see here.

In my work I’ve seen that this climate has resulted in increased carrier profitability for certain lines over the last couple of years, such as auto liability, but decreased carrier profitability in others (such as cyber and commercial property).

In higher education, Mary Ellen explained there have been hard market consequences due to underwriter inability to achieve profitability, and as noted in the visual, they are dealing with risks many organizations don’t need to think about, like traumatic brain injuries, the general public accessing the property, and a different kind of medical malpractice. As a result, there are a limited number of carriers willing to provide coverage in this space. As a nod to captive advantages, EIIA was able to grow surplus from their captive prior to the hard market, from 2002 to 2022, which has been extremely helpful in this “stormy environment.”

This success story led us to a discussion around the business case for captives, a snapshot of which you can see here in this video.

Jeff then gave a bit of a play-by-play regarding the process, implementation, timelines and driving forces behind Haskell’s decision to switch from a group captive to a single parent captive (a synopsis of which you can find in this case study).

Looking Ahead

Both Jeff and Mary Ellen described some next steps for their captives, which may include writing in:

- Integrated deductible plans

- Directors & officers

- Cyber

- Employee benefits

- Other P&C lines

Food For Thought

Like most good things in life, you kind of had to be there to get the full experience and maximize your take-aways. So I don’t want to give it all away, but I will leave you with some food for thought that came out of the Q&A for the session. If you want to know the answers, please get in touch!

- With a newer captive that hasn’t had time to build up surplus yet, how do you think about keeping your captive adequately capitalized?

- What are the next coverages or exposures you see on the horizon for higher ed that you would like to add to the captive program?

- What were the key drivers for your CFO to be on board to establish the captive?

- Can you talk about how reviver statutes have impacted obtaining/maintaining abuse coverage?

- As we face uninsured risks like communicable disease, how do you assess the use of the captives together with unique insurance solutions like parametric options? What is the value pitch to the organization?

- What type of coverages perform well in the hard market and why?

- Does forming a captive in a hard market only make financial sense if your company’s loss ratio is below the industry average?

- How do you handle cyber in a captive? Do you have a TPA on retainer?

- Are you using the captive for deductible reimbursement? Do you take any quota share or excess layer risk?

- What does your auto exposure look like and what risk mitigation strategies have you implemented (via the captive or otherwise)?

- How do you market your captive to new members who may not understand captives? Especially in light of the hard market, where captives are especially attractive.

And last but perhaps most importantly:

- What do you think the impact to the insurance market will be if the Browns win more than 2 games this year?

As you can see, we can have some fun in the captive world, and much of it was had at VCIA! Before you leave, check out our captive business case video here, inspired by this presentation.