Our Chief P&C Actuary, Peter Johnson participated in a panel discussion at the Vermont Captive Insurance Association (VCIA) Annual Conference on hard-hitting solutions to hard market concerns. Check out this article in Captive International which summarizes key points of the discussion.

The Challenge

A mid-sized (over $1B in annual revenue) architecture, engineering, construction and consulting firm was utilizing an industry group captive to underwrite their workers’ compensation, general liability, automobile coverages and subcontractor default risks. The organization requested Spring to help assess whether the group captive solution was still optimal and to help shape their risk management strategy. As part of this review, we assisted them in considering the pros and cons of exiting the group captive program to form their own single parent captive. To support this decision, we helped them understand both the financial implications and qualitative factors they should contemplate and the implications of this change.

The Process

Spring began by undertaking a total cost of risk assessment at the line of business level for workers’ compensation, general liability, excess general liability, professional liability, subcontractor default, and medical stop-loss insurance lines. The purpose of the study was to explore the universe of options available to the client and included a high-level review of potential risk structures, retention levels, domicile options and reinsurance/fronting options. In addition, Spring commented on the competitiveness of the existing framework, generating a robust view of the advantages and disadvantages of the different solutions, and provided recommendations as to how best to move forward.

Spring’s Solutions

Spring implemented a multi-step approach that included the following:

- The Quantitative Analysis: Creating a total cost of risk comparison between the previous group captive and proposed single parent captive structures for each line to understand program cost savings. The key steps include:

- Analyzing loss and exposure data

- Developing expected claims at various retentions

- Defining operating cost assumptions (other than retained loss)

- Modeling captive company Proforma balance sheet and income statement

- Estimating captive capital requirements

- Obtaining brokerage quotes at the analyzed client retention levels to determine optimal retention level and the anticipated market savings that go with it

- The Qualitative Analysis: Evaluating non-financial factors such as risk distribution, domicile, regulations, administrative requirements and the positives and negatives for each captive solution. The key steps included:

- Evaluating the required structure to meet appropriate insurance tests, like risk shifting and risk distribution

- Evaluating differences between the home state and other potential domiciles

- Conducting a deep dive into the various service provider functions and requirements

- Completing a policy review to outline potential changes to coverage terms with a single parent captive

- Providing a pros and cons analysis for a single parent captive versus the current group captive structure. Some of the benefits of each are as follows:

- A single parent captive model allows additional flexibility in coverage option including medical stop-loss, more control over funding structure and selected services and risk control programs, and the ability to take full advantage of a favorable long-term loss profile

- The original group captive structure offers favorable pricing over commercial markets for certain lines in the near term due to large, self-insured retentions and economies of scale by mixing in the risk of other large insureds with similar risk profiles. It also allows access to certain safety management and other services (if desired)

- Reporting of Results: Preparing and presenting a report highlighting the financial and non-financial differences to enable the client to make a fully-informed decision to either move forward with implementation or stay with the existing captive.

- The Client Decision: After thorough fact finding, analysis and comparisons, and communication with the client, the decision was made to form a Vermont-based single parent captive. To move the process forward, we created an actuarial captive feasibility study, a captive business plan, policy forms and other documents to be submitted to the Vermont regulators. There was initial uncertainty over whether the client would still receive required risk distribution, as there was a change in the third-party risk profile with a single parent captive. However, the accounting and tax team concluded that the new entity, based on the selected coverage structure and underlying insured exposures, still qualifies for risk distribution and can be treated as an insurance company

- Next Steps: Spring began quarterbacking the client through the implementation process once they decided to form their Vermont single parent captive, which involved the following:

- Preparing an actuarial captive feasibility study and worked with the selected captive manager on the application material for submission to the Vermont department of insurance

- Assisting in the selection of service providers for the captive

- Providing ongoing actuarial and consulting services to the parent company and their captive to ensure that they are aware of all possible insurance solutions available and are informed in their insurance choices

Ongoing Success

In the current challenging market conditions, a captive solution is a powerful tool to have during renewal negotiations. Even if it isn’t implemented immediately, having the captive option available provides a competing solution to traditional carriers. Even for coverages not insured through the captive, the client will have increased bargaining power and may receive better offers from traditional insurers. Most importantly, moving from a group captive to a single parent captive has provided the organization the opportunity to use a captive solution to support other aspects of their business. For instance, by adding medical stop-loss to the captive, they will be able to generate additional savings for the HR teams, allowing increased support for employee wellbeing and resources to implement additional wellness initiatives.

In summary, the client chose the solution that provides them flexibility, over maintaining the status quo of their group captive, and enables the parent company a recoup of profits, particularly as it builds surplus over time, that would otherwise go to the group captive and excess carriers. As the captive matures, the client is also expected to receive captive profits back as dividends and be able to further increase self-insured retentions. We will continue to provide insurance consulting (both captive-related and beyond) to the parent company and lead them through the initial year of single parent captive strategies.

In April of 2022, the Bureau of Labor Statistics reported that inflation hit a staggering 8.5%. If current projections hold true, this year will have the highest inflation rate since 1981. COVID-19, supply chain problems, Russia’s invasion of the Ukraine, housing price increases, and more predictable market cycles are some of the driving forces behind such high inflation. In our line of work – insurance, risk management, and employee benefits – macroeconomic factors like these are seen in the challenges our clients face and the solutions they prioritize. To complicate things, the property and casualty realm is also subject to things like natural disasters, climate risk, changes in societal litigiousness, and ransomware/cyber risk. That said, we sat down with Peter Johnson, Spring’s Chief Property & Casualty Actuary, to discuss how this challenging environment interplays with his work in the captive insurance space.

Q: Is inflation having an impact on underwriting and pricing?

A: This is case-by-case between captives but as an overall average, yes. A captive in a strong surplus position and favorable historical loss experience will still be able to provide favorable pricing even when the industry is seeing high loss trend and rate increases. Higher frequency and/or severity trends are certainly still impacting pricing needs for certain lines, such as cyber and excess liability where experience isn’t frequent in nature and the credibility of a single company’s experience is low. Specifically for cyber, ransomware loss costs have grown exponentially over the last 3 years and rate increases are being observed by both commercial carriers and captives. Further for both cyber and excess liability where commercial market pricing issues exist capacity has also shrunk and captive are being looked to, to fill the gap.

Q: Is inflation currently impacting reserving and if not, do you think it will in the future?

A: In general, yes, for many casualty lines where loss trends are high or increasing, but this is also a case-by-case basis since captives with good data credibility and stable historical loss experience can respond to their actual loss development and may not have a need for much, if any, reserve increases due to inflation. Cyber liability, commercial auto liability and excess liability are three lines in the industry with increasing severity trends and captive reserving practices often consider industry trends when company experience isn’t fully credible by itself, so I would expect some reserve strengthening for these lines due to trend assumption increases. Supply chain issues have been an obvious issue in the used car market and depending on a captive’s auto exposure and experience, there may be both increasing auto rate levels and reserve levels for the captive.

Q: Some analysts have suggested that while commercial market insurers are concerned about inflation, the impact might be offset to some extent by the benefit of higher interest rates in their investment portfolios. Would you expect captives to realize a similar investment benefit? Would you expect it to be significant?

A: To the extent a captive’s investment portfolio is invested in higher yielding fixed income, securities or other investments that are inflation sensitive then yes, there would be some offset.

Q: Are there specific coverage lines in captives that will be more affected by inflation than others?

A: Cyber, excess liability/umbrella and auto liability have seen higher trends than workers’ comp. Geography is an important factor as well since certain areas have seen noticeably higher/lower trends than the industry average. For example, medical professional liability severity trends have increased, but this varies significantly by region. Some states are seeing double digit severity trends and rate increases while others are experiencing very modest increases. Difference in litigiousness and jury awards drive much of these state-by-state differences. Property is certainly impacted by inflation with increases in cost to build, but natural catastrophes such as hurricanes, wildfire and wind/hail have typically had more of an impact and to compound things the current supply chain and inflation issues immediately after a disaster can lead to even costlier natural disasters. According to NOAA National Center for Environmental Information 2021 came is second all-time with 2020 coming in first as far as the total number and total cost of these disasters.

Q: Would you anticipate any changes in captive strategies in response to inflation?

A: For captives with active investment advisors, I’d expect a response on the investment side depending on their current investment profile and the surplus and loss reserve position of the captive. There certainly could be a variety of responses on the insurance risk side, particularly if inflation is driving up claim severity and significantly changing the risk profile of a captive. Capitalization, limits, retentions, reinsurance, and pricing are all potentially impacted and would need to be considered.

Q: Is there any advice you’d offer captive owners regarding inflation strategy?

A: In general, it is important to sensitivity test your proforma projections every few years based on practical adverse loss outcomes and investment income scenarios. These financial projections can consider higher than anticipated inflation trends over a multi-year projection horizon. This will help determine appropriate captive capitalization levels, reinsurance, pricing, and risk margin to protect against possible adverse events.

Q: Any final thoughts on the subject?

A: Firstly, large jury awards remain top of mind for many company executives and boards. Although the impact on industry combined ratios is less obvious based on what I’ve seen, this continues to be a big concern and is part of the driving force behind pricing increases in the commercial market for certain liability lines.

Secondly, as carrier capacity presumably decreases and underwriting profit margins increase for certain carrier lines where rate level increases outpace loss trend, captives will continue to be utilized to insure more risk and recoup underwriting and investment income related profits otherwise going to commercial carriers.

There you have it. While there are many negatives that sprout from inflation, one positive is that it allows captives to continue to elevate their status as a strategic risk management and financial tactic for organizations of all kinds, and help companies better face the difficult economic climate.

A recap of a presentation by Peter Johnson of Spring, Deyna Feng of Cummins, and Melissa Updike of KMRRG at the VCIA 2021 annual conference.

Black Swan Events and Market Capacity

Over the last year and a half, the world as we know it has been flipped on its head. Not only did everyone’s day-to-day processes change completely, but the COVID-19 pandemic also stressed the insurance system significantly and resulted in a number of changes across various lines. “Black Swan” events are those that are unexpected, severe and affect a large number of companies and individuals which is exactly what happened with the COVID-19 pandemic. While the healthcare industry faced increasing premiums and alterations to mental health coverage, the property-casualty (P&C) market also was affected in an unpredictable way.

Rewinding back to prior to March 2020, the P&C market was experiencing an all-time high surplus, and was in a 10-year trend of suppressed rates. Therefore, when the “Black Swan” event of a pandemic hit, insurance companies were forced to significantly reduce capacity to mitigate social inflation and high-cost claim issues. In some cases this drop down insured limits by 75 percent or more of their prior year policy limits. This was evident particularly for cyber liability and umbrella coverage. Additionally, rates across lines were seeing double and triple previous years’ numbers.

On the other hand, some P&C lines actually saw improvement in their combined ratio during 2020. This means that where some lines saw increases in cost, other lines saw a drop in utilization, which “evened out” the overall market. This improvement can be seen in commercial and personal lines auto lines over the last year. The auto industry saw a dramatic downturn in utilization due to reoccurring “Stay at Home” executive orders hindering travel as well as other related changes to the industry.

Needless to say, this all yielded a difficult environment for employees and employers. In order to appropriately mitigate these new or changed risks, companies have been turning to policy exclusions as well as captive financing to better protect themselves and their employees from high-cost claims.

Policy Exclusions and How They Impact Your Business

During the pandemic, no insurance company or insured was truly prepared for the changes that were to come, and many insureds were faced with unexpected coverage exclusions and were left with potentially catastrophic payments. Some examples of policy exclusions include pandemic situations, interrupted business, long-term care, and others. However, employers who had a captive insurance company set up were sometimes safeguarded from policy exclusions, and companies without a captive increasingly flocked to establish one.

To illustrate the advantages, one captive held their policy exclusions to the standard of COVID-19 claims and were able to mitigate those costs through their reinsurance retention. As another example, the Kentuckiana Medical Reciprocal Risk Retention Group (KMRRG), a captive, was able to flip their exclusion around long-term care, a move which, although it was only a small component of their business, significantly minimized costly losses. The framing of this exclusion allows employers to wrap reinsurance around this risk, specifically if they utilize a captive funding vehicle.

Captives offer more flexibility around policy language and terms, which can be adjusted according to the specific risks of the parent company. It is generally the responsibility of the brokers to let their insureds know which reinsurance renewals were at risk during the pandemic. Most commonly these lines were workers compensation, healthcare programs, and other P&C lines, which can be written into a captive or an RRG solution. Note RRG’s cannot write workers’ comp and can only insure liability lines.

Maximizing Captive/RRG Solutions

Captive insurance is not a new concept; however, it is often overlooked as a method for employers to protect themselves against risk. Captives not only better reflect underwriting records but also allow insureds to recoup investment incomes that would normally have been lost to insurance companies.

Captives support the parent company’s risk management overall and provide financial protection and long-term savings, both necessary for any business in ordinary and extraordinary times. Generally, our team sees that, for every $1 of premium that a client converts from a commercial reinsurer to a captive, 10 percent to 40 percent of long-term savings in the form of investment income and underwriting profits are yielded.

A captive can step in to help when commercial market rates are unreasonable, such as the 200 percent to 300 percent rate increases, we have seen recently, which of course are impossible for CFOs to plan for. This happened with many insureds’ umbrella coverage. Many companies over the last 20 months were forced to significantly lower their limits and increase their retention levels simultaneously. With changing premiums (mainly increasing) on top of this reduced market capacity, more and more often companies are utilizing captives to get control over these types of high costs and expand coverage.

Additional benefits of a captive or RRG solution include transparency and improved claims management. For example, if COVID-19 claims do develop, with a captive you can react with a very specific claims management strategy instead of relying on a commercial carrier to do so. This allows you to hand select your partners such as attorneys and other advisors. You can also be sure that your discovery responses are consistent. Additionally, group aggregates have hardened even more in the market which has forced captive managers to become more creative than before. An illustration of that creativity can be seen in the example below.

Hospital Professional Liability in a Captive: Many entities were trying to get their mitigation placed, and by increasing primary levels they were able to provide some protection and increase their claims control.

Bracing for the Future

In order to be properly prepared for the next “Black Swan” event, employers and employees should consider the major lessons learned from the past year:

Risk Diversification

This is not unique to a pandemic situation. When leveraging a captive, it is imperative to have a wide range of exposures. Our actuaries know that, in line with the law of large numbers, the more risks and more exposures, adverse financial outcomes become less likely and more manageable. Considering the correlation between the risks is equally critical as one risk could lead to a domino effect of triggering another high-cost risk. A general rule of thumb for captives is adding low correlating risk to a captive will lead to more stable year-to-year financial results.

Speed to Market

What is your process to quickly adapt to changing market conditions?

Analyze Current Structure

Can you withstand another “black swan” event? What are the coverage improvements that can be made internally?

Financials

What is your cots of risk and risk tolerance? Do you need an improved insurance/reinsurance strategy?

Supply Chain

Has an appropriate strategy been considered?

Other

Do you have uninsured/underinsured risks? Is there sufficient market capacity for your exposure?

If there is a positive we can take from COVID-19, it should be that we learned important lessons and won’t be as blind sighted in the future. Looking ahead, companies should ascertain whether they have the right tools in place to better manage risk and financial losses. In addition to the risk structures and their advantages outlined above, considering cross exposures and diversified risks is the best and easiest way for companies to protect themselves and their employees in the event of another “Black Swan” event. Lastly, having an aggregate view of risks across the organization often leads to creating the most efficient and cost effective risk funding programs.

Check out Captive.com’s writeup of a panel Spring’s Peter Johnson moderated at the Vermont Captive Insurance Association (VCIA) 2021 Annual Conference.

Our Chief P&C Actuary, Peter Johnson was spotlighted in Captive International’s Captives Rising: Hard market brings new opportunities report. In which Peter how the pandemic has changed the risk management practices and what businesses should look out for. Check out the digital report here.

Check out this article by Captive International, where they spotlight Spring’s experience with captives and how we approach captive and risk optimization.

Our Senior Consulting Actuary, Peter Johnson has been selected for Business Insurance’s 2019 Break Out Awards! Check out this quick Q&A with Peter that gives insights into his background.

For employers with robust benefits programs in place, an integrated approach is continuing to become an increasingly popular way to take things to the next level, and for good reason. Although the concept is not new, and our team of experts has been developing solutions for years, certain aspects are getting employers’ attention.

Spring’s 2016 and 2018 employer surveys, led by Spring’s Senior Vice President Karen English, show that the core drivers to developing an integrated program are:

- Costs savings

- Simpler administration

- Upgraded employee experience

- Enhanced tracking capabilities

- Improved compliance

There’s a lot more impacting these areas than you might think, so let’s take a deeper dive.

Cost Savings:

Having an efficient benefits program with systems that speak to and work with each other can go a long way for your bottom line. Integration provides greater transparency into your workforce – absence management challenges, productivity, employee health – among other things. This knowledge is an opportunity to create a healthier, more present workforce.

If this sounds like qualitative “fluff”, it’s not. One healthcare client was able to save over $10M in direct and indirect costs through integration. These savings resulted from savings in the following areas:

- Workers’ compensation

- Disability

- Unplanned absence

- Vacation

- Other Leaves of Absence

Their program, done in tandem with captive insurance company funding, also yielded risk diversification and stability, as well as further savings of 10% of premiums.

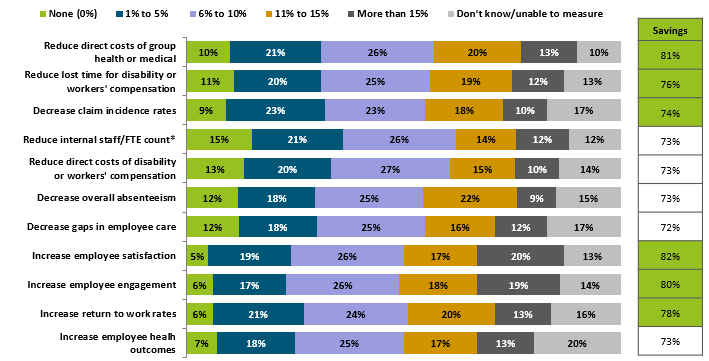

The graph below shows the average levels of employer savings achieved by implementing an integrated program, spanning a range of direct and indirect cost categories.

Simpler Administration:

All parties benefit from an integrated benefits system. An immeasurable amount of time and effort is saved from not having to go to different platforms for critical information. This will speed up the claims process.

The best integrated programs send notifications and communications, and offer automated triggers, case management and documentation. For managers, results are easier to explain. For employees, access is simpler and more approachable. At the corporate level, you can expect faster turnaround time and greater visibility.

Upgraded Employee Experience:

Employees do not typically understand the nuances surrounding absences, nor the various policies, plans, and processes involved. They simply need time away. By integrating absence to include occupational and non-occupational events, your employees will experience:

- Fewer points of contact

- Clearer processes to follow

- Faster turnaround times

- Improved information access

- Increase self-service options

- Decreased confusion

These benefits lead to an enhanced employee experience including higher engagement, both at the organization and with their health. As all HR professionals know, engagement is critical for recruiting, retention and overall performance. Whether at risk or not, all employees will appreciate a smarter, more robust benefits program and an employer that is looking out for their wellbeing.

Enhanced Tracking Capabilities:

To make sustainable improvements, it is imperative to track your integrated program and mine the data across all absences to investigate patterns and draw predictions. An integrated program allows for metrics across plans and policies with drill-down features such as:

- Occupational vs. non-occupational

- Paid vs. unpaid

- Job protected vs. non job protected

- Return-to-work vs. stay-at-work

- Sick, vacation, etc.

- Self vs. family

- Continuous vs. intermittent

- Diagnosis specific

With all these different facets captured uniformly, you have reporting that is comprehensive; supports workforce planning and budget; allows for strategic planning with HR as a business partner; and offers opportunities for prevention; so that your organization can be proactive instead of reactive. These kinds of insights allow employers to move into population health management.

Improved Compliance:

With the hub of intelligence that an integrated program offers, employers have a more reliable way of remaining compliant when it comes to things like the ADA, FMLA and ERISA, as well as any state-specific regulations and policies unique to the company. Automation will make leave requests and absence tracking much easier to manage, and accurate documentation will aid accountability for employers and employees alike.

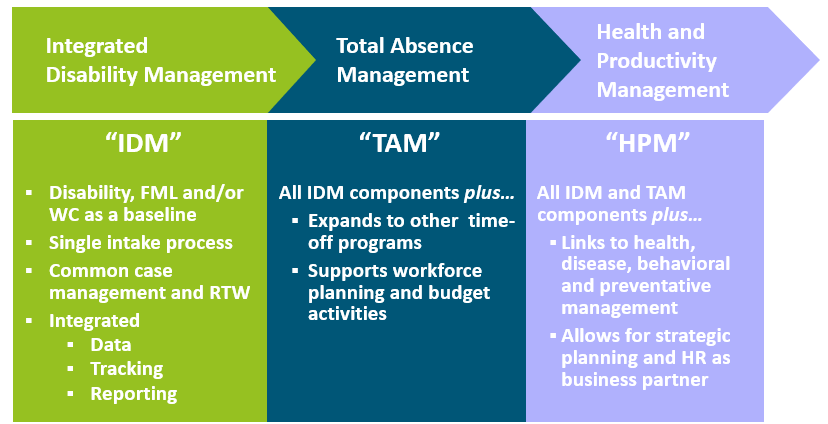

Ultimately, an integrated workers’ compensation and disability program can have significant positive impact on a company and its employees, especially for larger employers. We have seen great, quantifiable success with integrated programs from our clients. If you are thinking that this process seems too big a task to take on, don’t worry. Any company can start at any point along the continuum shown below, and gradually work their way to a model that facilitates population health management in the workforce.

Most Common Approach is Phased