At the VCIA 2022 Annual Conference, our Managing Partner participated in a panel that highlighted the scary long-term care landscape, but that ended on a high note in exploring the possibility of captives as a next generation solution for long-term care insurance.

With innovation embedded in the DNA of both Spring and captive insurance, we are interested in helping reshaping the long-term care market of the future. Check out the other discussions our team members had on VCIA session panels, or get in touch to talk in more detail about long-term care captive strategies.

In our latest podcast on Global Captive Podcast, our Managing Partner is joined by President and CEO of Spring’s client, edHEALTH to discuss the evolution of the captive program and its success.

A (Brief) VCIA Session Recap

I had the pleasure of speaking at Vermont Captive Insurance Association (VCIA) Annual Conference last week, joined by two colleagues with impressive backgrounds. Jeff Caudill, Director of Risk Management at Haskell and a client of Spring’s, and Mary Ellen Moriarty, Vice President, Property & Casualty at College Insurance Company (EIIA) joined me to discuss different ways that captives can be used to tackle the hard market hurdles we’re currently facing in the insurance industry.

With myself as the moderator and consulting actuary, Jeff representing a brand new single parent captive, and Mary Ellen representing a veteran captive, it was a well-rounded panel that pulled in multiple perspectives.

The Clouds Behind the Hard Market

This visual does a great job at illustrating the many challenging atmospheric effects in the insurance air right now, particularly on the property & casualty (P&C) side of the fence (no pun intended). With Mary Ellen representing the higher education space, we felt it important to highlight unique risks that colleges and universities are grappling with, in addition to the other complicating factors (or clouds) we see here.

In my work I’ve seen that this climate has resulted in increased carrier profitability for certain lines over the last couple of years, such as auto liability, but decreased carrier profitability in others (such as cyber and commercial property).

In higher education, Mary Ellen explained there have been hard market consequences due to underwriter inability to achieve profitability, and as noted in the visual, they are dealing with risks many organizations don’t need to think about, like traumatic brain injuries, the general public accessing the property, and a different kind of medical malpractice. As a result, there are a limited number of carriers willing to provide coverage in this space. As a nod to captive advantages, EIIA was able to grow surplus from their captive prior to the hard market, from 2002 to 2022, which has been extremely helpful in this “stormy environment.”

This success story led us to a discussion around the business case for captives, a snapshot of which you can see here in this video.

Jeff then gave a bit of a play-by-play regarding the process, implementation, timelines and driving forces behind Haskell’s decision to switch from a group captive to a single parent captive (a synopsis of which you can find in this case study).

Looking Ahead

Both Jeff and Mary Ellen described some next steps for their captives, which may include writing in:

- Integrated deductible plans

- Directors & officers

- Cyber

- Employee benefits

- Other P&C lines

Food For Thought

Like most good things in life, you kind of had to be there to get the full experience and maximize your take-aways. So I don’t want to give it all away, but I will leave you with some food for thought that came out of the Q&A for the session. If you want to know the answers, please get in touch!

- With a newer captive that hasn’t had time to build up surplus yet, how do you think about keeping your captive adequately capitalized?

- What are the next coverages or exposures you see on the horizon for higher ed that you would like to add to the captive program?

- What were the key drivers for your CFO to be on board to establish the captive?

- Can you talk about how reviver statutes have impacted obtaining/maintaining abuse coverage?

- As we face uninsured risks like communicable disease, how do you assess the use of the captives together with unique insurance solutions like parametric options? What is the value pitch to the organization?

- What type of coverages perform well in the hard market and why?

- Does forming a captive in a hard market only make financial sense if your company’s loss ratio is below the industry average?

- How do you handle cyber in a captive? Do you have a TPA on retainer?

- Are you using the captive for deductible reimbursement? Do you take any quota share or excess layer risk?

- What does your auto exposure look like and what risk mitigation strategies have you implemented (via the captive or otherwise)?

- How do you market your captive to new members who may not understand captives? Especially in light of the hard market, where captives are especially attractive.

And last but perhaps most importantly:

- What do you think the impact to the insurance market will be if the Browns win more than 2 games this year?

As you can see, we can have some fun in the captive world, and much of it was had at VCIA! Before you leave, check out our captive business case video here, inspired by this presentation.

In this quick video, we outline 6 points that build the business case for captives. Check them out if you are struggling with getting executive buy-in to enter the captive space, or even if you are looking to do more with your existing captive.

With healthcare costs skyrocketing and employee needs shifting, many employers are examining how they can save money while still providing strong benefits packages. Last week I spoke at the Vermont Captive Insurance Association (VCIA)’s 2022 Annual Conference on current medical stop-loss market trends and how captives can help cut costs. My fellow panelist, Tracy Hassett, President of edHEALTH, a collection of educational institutes and client of Spring’s spotlighted their captive which has seen significant savings.

Cost of Healthcare

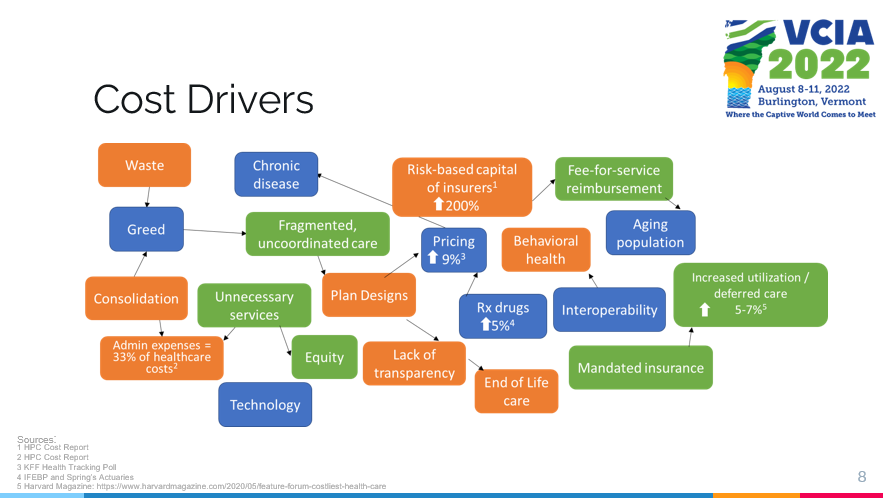

Healthcare costs keep climbing for both employers and employees and our actuaries predict an increase in medical trends for 2022 between 4%-7%. Looking back further, within the past decade healthcare costs have risen roughly 80% for employees and 60% for employers while economic growth has been consistent at 2.5% annually. This increase in costs is coming from a range of factors including administrative expenses, prescription drug prices, increased utilization/deferred care, and risk-based capital of insurers.

We are also seeing a transition in what employees want out of their benefits packages. Our working population is changing; boomers are retiring and transitioning from employer health insurance to Medicare. Millennials have different needs and are looking for straightforward and convenient benefits without high costs. These shifts in healthcare priorities along with high costs have slowly made self-insurance the norm, with a Spring survey reporting 64% of all employers are now self-insured.

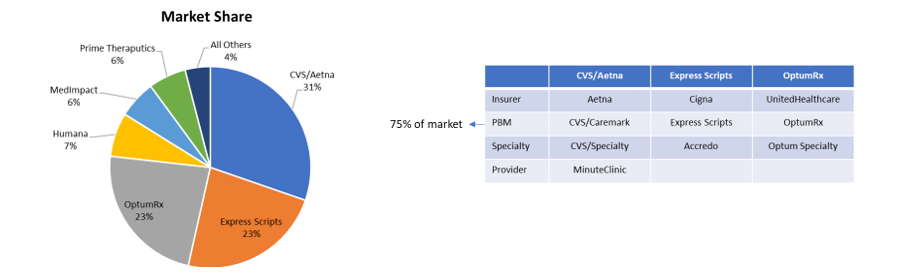

When looking at the healthcare market the vast majority of pharmacy spending is through pharmacy benefit managers (PBMs). Employers estimate outpatient pharmacy to be about 18% of health spending, with an additional estimated 10% within medical claims. Also in 2020, overall drug spending rose by almost 5%, with utilization and new drugs driving most of this increase.

Self-Insurance

We are seeing a fundamental change in the healthcare market, and all parties within the healthcare continuum are being asked to handle risk and chase healthcare dollars. This has pushed many employers to move towards self-funding plans which allow for greater customization, more control over risk, and potential cost savings. Many of these self-insured programs are looking at putting medical stop-loss into a captive, with a Spring survey reporting that although less than 50% of self-insured programs have stop-loss coverage, 42% of those that do have it within a captive.

Within the COVID era we have also seen many changes in the industry and numerous employers are reevaluating their healthcare packages. There has been a giant spike in mental health and COVID-19 resources like telehealth, and a decline in elective surgery. These trends have left hospitals and providers with the short end of the stick, leaving self-insured employers and health plans as the parties saving the most in the insurance landscape.

Case in Point: edHEALTH

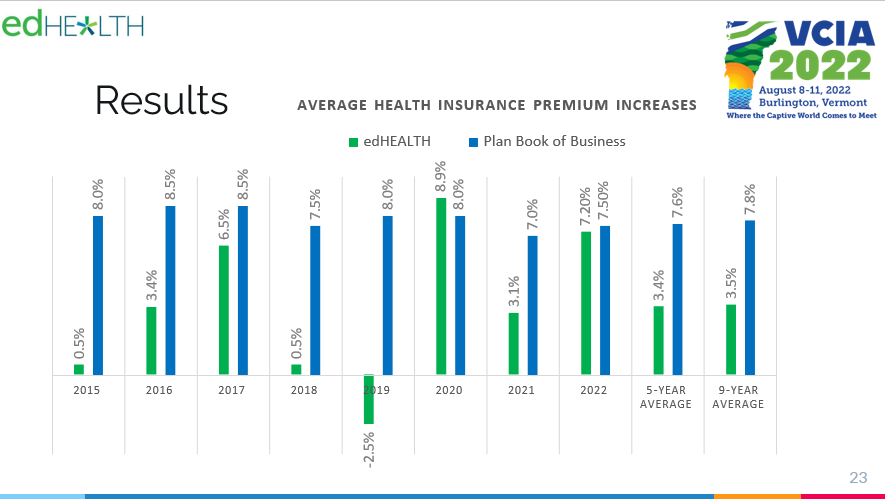

Tracy Hassett led the case study portion of the presentation, with edHEALTH being a prime example to of a captive successfully yielding savings in healthcare costs as well as flexibility of options. edHEALTH is a consortium of 25 higher education institutions who came together (originally as a group of six schools) to bend the trend in rising healthcare costs. Today, edHEALTH covers almost 15,000 employees (~30,900 lives) and aim to better understand and control their healthcare costs and risk. Tracy explained edHEALTH’s captive structure and how the captive retained savings of $6.7M since inception through 2020, in addition to paying out $3.2M in dividends.

These universities all have similar risks when it comes to healthcare, so investing in a group captive was the ideal solution. Each member chooses their own level of risk and pays for their own claims (below the established self insured retention level [SIR]), but still has control of their program. Tracy continued to explain how prescription drug costs are one of their largest challenges when trying to save money in creating/reevaluating healthcare plans. However, with their captive in the past four years edHEALTH members have saved an estimated $50M on Rx costs.

All in all, I was honored to join in the thought-provoking discussions that took place at VCIA. Since medical stop-loss is one of the biggest areas of focus for our clients right now, it was a pertinent conversation and I was glad to have the opportunity to share my perspective, as well as the success of edHEALTH. Burlington remains as perfectly quaint as ever, and I look forward to next year’s event.

We are all feeling the impacts of inflation, and as the word “recession” continues to be a popular one among political, economic and social conversations, we thought we would sit down with our captive insurance experts (Karin Landry, Prabal Lakhanpal and Peter Johnson) to get their two cents on how a possible recession or economic downturn interplays with risk and financial management tactics, with a focus on captives. Here’s what they had to say.

1. What are some possible impacts of a recession on captive insurance companies?

Peter: Changes in risk profiles driven by economic changes (examples include commercial auto frequency moved down then up, cyber ransomware on the rise, healthcare workers’ compensation programs utilized, excess liability/umbrella rates increased substantially, etc.). This also impacted the commercial market and captives often stepped in to fill the gap.

Prabal: Changes in exposure units: a recession may lead to reduction in workforce and therefore a change in insurance spend. On the employee benefits side, during times of uncertainty we typically see an increase in disability claims as well as a spike in usage of health insurance. When taken together with the change in exposure units, benefits programs may see a reduction in performance.

Karin: A continued increase in captive interest. Clients are looking at different ways to save money during a recession. For those organizations that already have captives, risk managers will need to prove the value of the captive, as typically there are a lot of dollars funding reserves that management wants access to in order to improve cash flow during a period like a recession.

2. Are there steps captive owners can take to safeguard their captive against a recession? If so, at what point should they implement them?

Peter: We recommend having service provider and reinsurer relationships in place to be enable the ability to make quick changes and file a captive business plan change to adapt according to the market.

Prabal: For existing captives, we advise undertaking a captive optimization or “refeasibility study” every few years, and this will be especially important if we enter a recession. This process assesses captive performance against original goals, aims to realign the captive according to changes in corporate objectives or priorities, evaluates impacts from recent regulatory changes and/or market trends, considers additional lines, analyzes the domicile, and so forth. Captive optimization helps organizations understand the vulnerabilities of your captive and help you shore them up.

Further, have your actuaries undertake stress testing of the captive to ensure financial stability and consider getting rates as a captive, where appropriate. Then, implement a dividend return policy, which ensures that in the time of need, there is a clear outline of how the parent organization can access any surplus in the captive. Be careful here as you don’t want the parent entity drawing down the surplus so much that the captive loses financial strength.

Karin: Risk managers should determine whether or not their captives are optimally funded. They should calculate the value of the captive to the organization before it becomes a management issue. They should explore other lines of coverage to determine whether or not it will save money, improve investment income, and/or increase cash flow for the organization going forward.

3. How would a recession affect underwriting?

Prabal: Insurance companies have two main revenue streams: 1) underwriting income and 2) investment income. In a recession environment, investment income becomes less likely or harder to come by. Therefore, underwriters are laser-focused on ensuring underwriting income, resulting in tighter underwriting standards. For example:

Peter: Carriers often tighten underwriting standards and may refuse to underwrite certain risks and/or business types all together. We’ve seen this for certain casualty lines like cyber, GL, and excess liability. Carriers may also be forced to remove manual rate discounts and/or increase rates all together while narrowing coverage at the same time.

Karin: Because underwriting practices may tighten, risk managers must understand their organization’s risks better than the marketplace. You could find that your experience is better than the book of business at the carrier level. If this is the case, a captive may make sense.

4. What about reserving?

Peter: To the extent a carrier’s or a captive insurer’s reserves are in a strong position due to favorable experience, reserve releases can be expected and may offset some of the poor 2022 investment experience we’ve experienced. The opposite also holds for exposures with loss trend on the rise that are driving up overall loss costs.

Prabal: Actuarial stress testing of the captive also comes into play here to ensure stability and dividend return strategy so that there is a consistent approach.

Karin: For captives that book discounted reserves, changes in the discount rates will affect the level of reserves captives carry. For those lines of coverage that are sensitive to recessions like workers’ comp and disability, the impact of negative experience should be factored into the reserving process.

5. Could the economic environment cause changes in captive methodology or the lines placed within a captive?

Peter: We’ve seen captive owners become more interested in captive utilization particularly when they feel like carrier coverage and pricing is unjustified based on their own loss experience.

Prabal: Captive optimization helps with optimal capital utilization. In a recession where capital is scarce, companies benefit from being efficient with how they use it.

6. What sort of pressures might captives face during a recession in terms of loan backs or dividends to the parents, or any impacts on capitalization?

Peter: We’ve certainly seen dividend policies put into place for certain clients that have been hit harder during the recession than others. Some have looked to access their captive capital that was built up to significant levels over the years.

Karin: As noted earlier, management may see the reserves of the captives as a pot of money to access; proving the value of the captive negates that issue.

7. The Great Recession around 2008 caused a stall in captive formations. Do we think that could happen again?

Peter: It seems fairly unlikely to have a similar scenario to 2008 since a portion of the collapse was driven by extremely poor mortgage underwriting standards in place. But anything is possible.

Prabal: Further, unlike in 2008, the commercial markets are still in a hard market cycle. This will likely be accentuated in a recession and therefore yield an increase in captive formations.

Karin: Because capital is scarce during a recession, this may spur the use of cell captive programs as opposed to pure captives to meet the needs that risk managers have to control costs and minimize price increases.

8. Anything else related to economic volatility that captive owners and risk managers should keep in mind?

Prabal: One thing would be the potential to free up captive capital by using loss portfolio transfers. The current interest rate environment is likely to create a preferential market for these opportunities.

Karin: Organizations’ hurdle rate might change as a result of the recession. This would necessitate looking at the opportunity costs associated with captives and their reserving process. Additionally, organizations should evaluate their insurance partners to make sure they are sound as they will be grappling with some of the same recession issues noted here. I wouldn’t be surprised if some of the insurers experienced difficulties and either left the marketplace, contracted and changed the coverage levels that they offer, and/or focused in on certain risks while excluding other risks from their policies in accordance with market shifts.

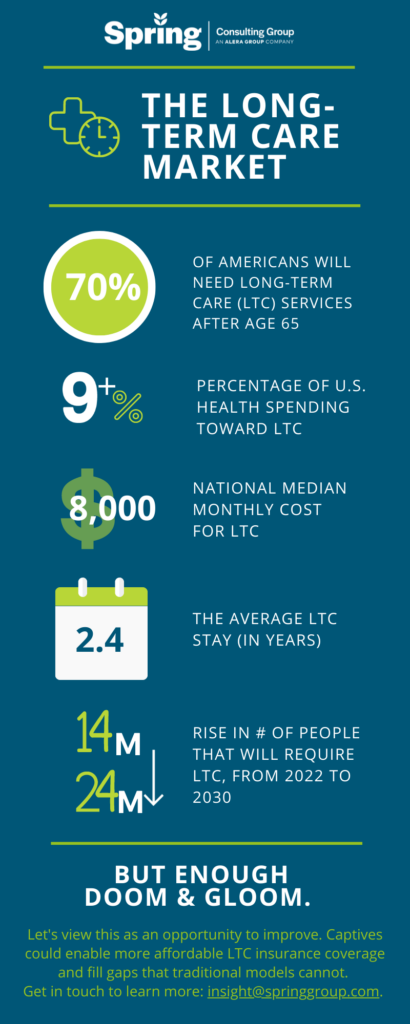

Our Managing Partner, Karin Landry led a panel discussion at the Vermont Captive Insurance Association (VCIA) Annual Conference on the potential use of captive insurance to be a tool for long-term care insurance in the future. Check out this article in Captive International which summarizes key points of the discussion.

Our Chief P&C Actuary, Peter Johnson participated in a panel discussion at the Vermont Captive Insurance Association (VCIA) Annual Conference on hard-hitting solutions to hard market concerns. Check out this article in Captive International which summarizes key points of the discussion.

The Challenge

A mid-sized (over $1B in annual revenue) architecture, engineering, construction and consulting firm was utilizing an industry group captive to underwrite their workers’ compensation, general liability, automobile coverages and subcontractor default risks. The organization requested Spring to help assess whether the group captive solution was still optimal and to help shape their risk management strategy. As part of this review, we assisted them in considering the pros and cons of exiting the group captive program to form their own single parent captive. To support this decision, we helped them understand both the financial implications and qualitative factors they should contemplate and the implications of this change.

The Process

Spring began by undertaking a total cost of risk assessment at the line of business level for workers’ compensation, general liability, excess general liability, professional liability, subcontractor default, and medical stop-loss insurance lines. The purpose of the study was to explore the universe of options available to the client and included a high-level review of potential risk structures, retention levels, domicile options and reinsurance/fronting options. In addition, Spring commented on the competitiveness of the existing framework, generating a robust view of the advantages and disadvantages of the different solutions, and provided recommendations as to how best to move forward.

Spring’s Solutions

Spring implemented a multi-step approach that included the following:

- The Quantitative Analysis: Creating a total cost of risk comparison between the previous group captive and proposed single parent captive structures for each line to understand program cost savings. The key steps include:

- Analyzing loss and exposure data

- Developing expected claims at various retentions

- Defining operating cost assumptions (other than retained loss)

- Modeling captive company Proforma balance sheet and income statement

- Estimating captive capital requirements

- Obtaining brokerage quotes at the analyzed client retention levels to determine optimal retention level and the anticipated market savings that go with it

- The Qualitative Analysis: Evaluating non-financial factors such as risk distribution, domicile, regulations, administrative requirements and the positives and negatives for each captive solution. The key steps included:

- Evaluating the required structure to meet appropriate insurance tests, like risk shifting and risk distribution

- Evaluating differences between the home state and other potential domiciles

- Conducting a deep dive into the various service provider functions and requirements

- Completing a policy review to outline potential changes to coverage terms with a single parent captive

- Providing a pros and cons analysis for a single parent captive versus the current group captive structure. Some of the benefits of each are as follows:

- A single parent captive model allows additional flexibility in coverage option including medical stop-loss, more control over funding structure and selected services and risk control programs, and the ability to take full advantage of a favorable long-term loss profile

- The original group captive structure offers favorable pricing over commercial markets for certain lines in the near term due to large, self-insured retentions and economies of scale by mixing in the risk of other large insureds with similar risk profiles. It also allows access to certain safety management and other services (if desired)

- Reporting of Results: Preparing and presenting a report highlighting the financial and non-financial differences to enable the client to make a fully-informed decision to either move forward with implementation or stay with the existing captive.

- The Client Decision: After thorough fact finding, analysis and comparisons, and communication with the client, the decision was made to form a Vermont-based single parent captive. To move the process forward, we created an actuarial captive feasibility study, a captive business plan, policy forms and other documents to be submitted to the Vermont regulators. There was initial uncertainty over whether the client would still receive required risk distribution, as there was a change in the third-party risk profile with a single parent captive. However, the accounting and tax team concluded that the new entity, based on the selected coverage structure and underlying insured exposures, still qualifies for risk distribution and can be treated as an insurance company

- Next Steps: Spring began quarterbacking the client through the implementation process once they decided to form their Vermont single parent captive, which involved the following:

- Preparing an actuarial captive feasibility study and worked with the selected captive manager on the application material for submission to the Vermont department of insurance

- Assisting in the selection of service providers for the captive

- Providing ongoing actuarial and consulting services to the parent company and their captive to ensure that they are aware of all possible insurance solutions available and are informed in their insurance choices

Ongoing Success

In the current challenging market conditions, a captive solution is a powerful tool to have during renewal negotiations. Even if it isn’t implemented immediately, having the captive option available provides a competing solution to traditional carriers. Even for coverages not insured through the captive, the client will have increased bargaining power and may receive better offers from traditional insurers. Most importantly, moving from a group captive to a single parent captive has provided the organization the opportunity to use a captive solution to support other aspects of their business. For instance, by adding medical stop-loss to the captive, they will be able to generate additional savings for the HR teams, allowing increased support for employee wellbeing and resources to implement additional wellness initiatives.

In summary, the client chose the solution that provides them flexibility, over maintaining the status quo of their group captive, and enables the parent company a recoup of profits, particularly as it builds surplus over time, that would otherwise go to the group captive and excess carriers. As the captive matures, the client is also expected to receive captive profits back as dividends and be able to further increase self-insured retentions. We will continue to provide insurance consulting (both captive-related and beyond) to the parent company and lead them through the initial year of single parent captive strategies.