Our Senior Vice President, Prabal Lakhanpal wrote an article for the Boston Business Journal on how employers can continue to provide strong benefit packages during a time of high inflation. You can find the full article here.

We would like to congratulate Prabal Lakhanpal for his recent promotion to Senior Vice President at Spring. We are glad to have his positive and driven personality on our team! Check out Captive International’s full recap here.

Our Senior Vice President, Prabal Lakhanpal was quoted in an Captive Intelligence article on how captives can be utilized in the private equity space. You can find the full article here.

After a two-year hiatus, it was great being able to attend The Cayman Captive Forum in person this year. As the Cayman Islands is the second largest captive domicile, and the first for healthcare captives1; it is the perfect location to share leading trends in the captive world, and the warm temperatures and tropical views made it all the more enjoyable. If you weren’t able to attend or could use a refresher after returning to the “real world,” this quick recap might be of interest. Below are some of the buzziest topics at this year’s conference.

1) Tax Updates

On large attraction to captive insurance (and certain domiciles) relates to tax advantages. It’s complicated, though. Some of the tax-focused sessions presented at the conference were:

– Mike Domanski, a lawyer from Honigman LLP, discussed offshore federal tax considerations and U.S. tax reporting requirements in his session titled “Captive Insurance: Basic Tax Fundamentals.”

– In a session titled “The State of Tax: What You Need to Know,” experts discussed U.S. federal tax updates and how taxes will be affected by the Inflation Reduction Act and updates to Section 831(b).

– The penultimate presentation titled, “U.S. Tax Update” tackled IRS and compliance updates in the U.S. on both the federal and state levels.

2) Cyber Risks

Since the start of the pandemic, employers had to adjust to remote and hybrid workplace policies. This transition forced employers and employees to rely more on digital tools to conduct day-to-day operations and made organizations more susceptible to breaches. This is not the first year that cyber took the spotlight, but there were some great discussions around risk in this area, including:

– A session titled “Placing Cyber Liability in Your Captive” reviewed current trends in cyber treats and how insuring cyber in a captive can prevent devastating losses.

– Risk and Cybersecurity experts from the Cleveland Clinic explained why the healthcare industry commonly falls victim to cyber attacks and outlined steps to take to protect patient and caregiver privacy in their session, “Current & Future Cyber Risks In Healthcare: ‘Will you still love me, tomorrow?’”

3) Healthcare-Specific Coverages

In recent years, we have been seeing an increasing number of healthcare organizations leverage their captive to bring new and industry-specific lines. At this year’s Cayman Captive Forum we learned about how captives can be used for the following emerging and alternative risks:

a) Medical Malpractice/Medical Errors

As the Cayman Islands is the most popular captive domicile amongst healthcare organizations, there was a large focus on healthcare-specific risks. There was a particular emphasis on how healthcare employers can reduce and prepare for potential medical malpractice/errors as noted in the following sessions:

– Presenters from the “Criminalizing the Clinical Defendant: Straight from the Headlines” session facilitated a mock deposition to address common medical malpractice trends and how they should be addressed.

– A session titled “Can your Captive Eradicate the Impact of Covid on its Medical Malpractice Program? Will It Ever End?” reviewed how medical malpractice can impact claims and legal outcomes.

– Dr. Dan Shapiro Ph.D., explained his experiences with burnout in the healthcare industry and steps employers can take to support healthcare workers in his presentation “Labor Shortages, Employee Burnout & Medical Errors: Working Together to Improve Results.”

b) Workplace Safety & Patient Care

Workplace safety is another non-traditional captive line (outside of employee benefits and Property and Casualty [P&C]) gaining traction. Healthcare organizations and, more specifically, healthcare workers and patients are prone to violence and discrimination more so than staff in other industries.

– In the session “Workplace Violence in Healthcare,” Trinity Health’s Diane Moritz explained initiatives their captive board are taking to prevent workplace violence injuries and support victims of patient violence.

– Children’s National Hospital’s Chief Diversity Officer, Denice Cora-Bramble discussed biases in data reporting for diverse patients, and experiences minority patients face when seeking health services in the session, “DEI Impact on Quality and Safety of Care.”

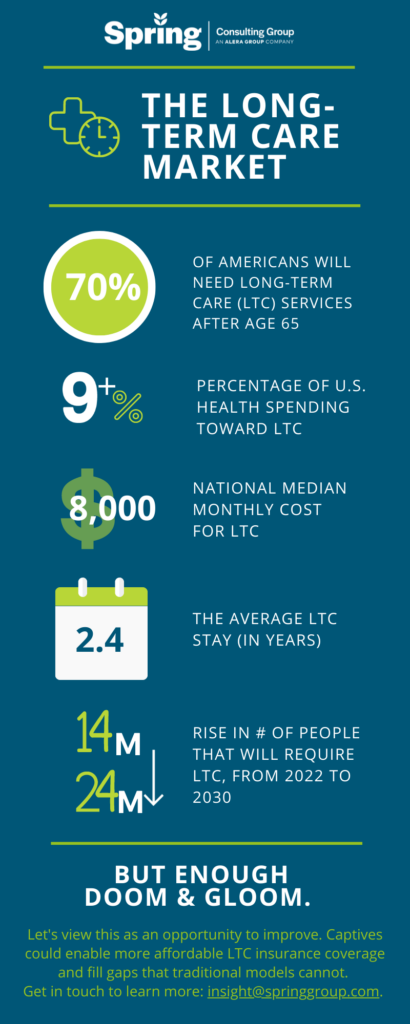

– I was joined by lawyer, Michael Domanski in a pre-recorded session titled “Using a Captive to Fund Long-Term Care,” during which we reviewed the current LTC market and different captive models (both taxable and tax-exempt) that can cover long-term care policies.

As we transition into a new era of captive insurance, this year’s Cayman Captive Forum acted as a perfect vehicle for addressing current and future themes in the industry. It was a strong end (almost) to an exciting year and we look forward to next year’s conference to continue these and other important discussions. Our team was fortunate to be part of the action in the Cayman Islands this year and is here to answer any questions you may have related to an existing or new captive program. Check out our captive expertise here and let’s chat!

1 https://caymanintinsurance.ky/about/

As seen on Alera Group’s Insights Page

In the cyclical market for Property and Casualty Insurance, we are more than a year into hard-market conditions, leading growing numbers of businesses to consider alternative risk funding. That, in turn, has created an abundance of work for insurance actuaries and Captive Insurance consultants.

OK, that’s a lot of insurance speak for one paragraph. Let’s unpack:

— A hard market for insurance is characterized by a rise in rates, a reduction in options for coverage, heightened scrutiny by policy underwriters and reduced carrier capacity for coverage limits. A combination of catastrophic weather events and so-called “nuclear verdicts” in liability lawsuits — as well as the cyclical nature of the Property and Casualty (P&C) Insurance market — were the driving forces behind the hardened conditions before the onset of COVID-19, and the pandemic exacerbated matters. Rate increases have leveled off to some extent in 2022, but, in general, most conditions in the market remain unfavorable to consumers.

— Alternative risk funding — also known as alternative risk financing or alternative risk transfer — is a mechanism for providing coverage by means other than commercial insurance. Types of alternative risk funding include Captive Insurance programs, in which a business or group of like businesses creates and funds its own private insurance company to cover one or more risks in the realms of both P&C and employee benefits. Workers’ Compensation, General Liability, Auto, Professional Liability and Medical Stop-Loss are the more common coverages to start with when insuring through a captive, but captives often expand into a funding mechanism for many of an organization’s other lines of insurance, including Cyber and Umbrella (also known as Excess Liability Insurance).

— Insurance actuaries use math, statistics and financial models to analyze the cost of risk and determine how much money a company should pay to protect itself against risk. All insurance carriers employ actuaries to help set policy premiums and limits. Some insurance agencies work with actuaries to negotiate policy details with carriers or, in a captive arrangement, to determine a premium that will cover claims and, in the long term, reduce the insured’s total cost of risk. Captives have the advantage of also building up retained earnings over time and allowing companies to take on more risk, generating additional insurance cost savings for the parent. Among multiple P&C capabilities, actuaries who work with or for an agency also educate clients on the cost of risk and how to manage it.

Now that we’ve cleared that up, let’s talk about the role of an actuary in managing the cost of risk and protecting your business with a customized insurance program — whether you’ve chosen to pursue alternative risk funding or not.

Why an Alternative Solution? And Why Now?

Business leaders know all too well about the hard market for Property and Casualty Insurance. Just as the pandemic began to wane early in 2022 and there were some signs of casualty rate increases leveling off, Russia’s invasion of Ukraine escalated supply-chain disruption and fuel shortages, accelerating the rise in economic inflation. Damage resulting from Hurricane Ian only made matters worse, of course, driving reinsurance — insurance for insurers — into what the Bank of America termed a “true hard market” of its own, with rising costs getting passed on to consumers. These issues have led to overall increases in U.S. P&C industry combined ratios over the past few quarters, sparking further rate increases for certain lines.

It’s no wonder more organizations are looking at captives and other alternative risk-funding solutions.

“Overall, between 2017 and 2021, captives added $4.3 billion to their year-end surplus while returning $5.8 billion in stockholder and policyholder dividends, representing $10.1 billion in insurance cost savings over purchasing coverage from commercial market third parties.”

“The number of U.S. captives continues to rise, although the growth of captive formations was tempered by the onset of economic uncertainty resulting from the pandemic, as well as ongoing scrutiny from the IRS and greater regulatory and reporting requirements.”

“However, these adverse conditions can serve to highlight the benefits of the captive segment and provide businesses an incentive to establish them,” said Fred Eslami, associate director, AM Best.

“‘This current environment allows captives to customize coverage for risks that may be uncommon or difficult to write or place in the standard market,’” Eslami said.

The growth in Captive Insurance has led to an increasing willingness on the part of carriers to work with captives and regard them as partners rather than threats, increasing options for captive solutions. And even if an organization in the end chooses to forgo alternative risk funding – either for an entire P&C program or for individual coverages, such as cyber or commercial umbrella – simply exploring an alternative and having it as an option can improve its position in the insurance market.

Actuary Capabilities: Your Data, Your Future

For insurance agents and brokers, designing an insurance program tailored to your industry and company is as much art as it is science. Working with an actuary enables you to incorporate greater amounts of empirical evidence into evaluating risks and determining insurance solutions: Here’s what the numbers demonstrate about your situation now, and here’s what our analysis shows about how you’ll perform using this solution.

While any good broker will work to design an insurance program customized for your business, a broker working with an actuary will be especially well-equipped to design a solution tailored to your unique needs and goals. Among the key issues an actuary can help brokers work through are:

- Determining appropriate retention/deductible levels to help the client reduce the total cost of risk;

- Estimating client retained unpaid claims liabilities at quarter/year-end;

- Estimating carrier letter-of-credit need for a large deductible program;

- Estimating possible retained loss outcomes at various confidence levels;

- Performing a captive feasibility study.

Many brokers work in silos, taking a vertical approach in evaluating risk based on industry. Actuaries generally don’t distinguish by industry; they analyze across various industries, focusing on each individual client’s loss history (including frequency and severity), claim status, policy details, exposures and risk-control program before determining financial projections for the organization. Taking the long-term view allows for consideration of fluctuations in company and market performance over a period of time, and increases the likelihood of long-term savings and profits.

Optimizing Your Insurance and Benefits Solutions

As companies grow, they generally reach a point where their claims experience is predictable across one or more lines of coverage. Able to determine such predictability, an actuary can then help you:

- Minimize your total insurance spend, directing more money to the coverage your business needs the most.

- Reduce spending on the risks you have under control. This is where alternative risk funding becomes viable.

If you’ve reached the point where your business is paying, say, $100,000 to $250,000 in annual premium, a group captive might be the best solution because you probably aren’t yet structured appropriately to meet the insurance tests required to form a single-parent captive and the economies of scale may not be there for a single-parent captive solution. In such a case you may need to diversify your risk with other organizations (heterogeneous or homogeneous) — in a group captive or in a shared-risk pool solution utilizing reinsurance — for at least the time being.

The bigger, more complex, more diversified a company becomes, the more a fully funded, single-parent captive emerges as an optimal solution in which the business is insuring only its own risk. A single-parent captive also allows for more coverage flexibility and transparency than a group captive program. Quite often, both benefits and P&C risks are insured by a single-parent captive.

What drives the decision to move from traditional, carrier-based insurance to a captive program is savings and, ultimately, return on investment (ROI). How? By moving expenditures that create carrier profits into the captive solution. Captives are highly efficient, with very low expense ratios, unlike carriers. Free from providing a carrier with underwriting income and investment income on held reserves, you’re able to retain this income to ultimately generate a profit and facilitate an insurance mechanism that competes with the commercial market.

An Organization-Focused Approach

In taking an organization-focused approach toward financial analysis, actuaries look not only at funding for Property and Casualty Insurance but also at spending on employee benefits. Most captive insureds will see annual savings between 10% and 40% for premiums that flow through a captive instead of the commercial market.

As we approach the end of the year, Alera Group invites you to the final event in our 2022 Engage series of employee benefits webinars, A Look Ahead to 2023: Hot Topics and Trends. Join us on Thursday, December 15 as we discuss benefits financial officers and HR professionals need to think about now — including alternative solutions — as they plan for the year ahead.

ACCESS ALERA’S WEBINAR HERE

As the Cayman Captive Forum starts just this week. We are proud to announce Spring and our consultants have been recognized for multiple awards from Captive International’s Cayman Awards 2022. We look forward to continuing to do excellent captive work in all domiciles, including but not limited to the Cayman Islands.

Spring has been awarded for:

Captive International has released the winners for the 2022 US Awards. Spring is proud to announce that our company and our Managing Partner, Karin Landry were selected as winners for Best Feasibility Study Firm and Best Feasibility Study Individual (respectively). We were also highly commended for Best Actuarial Firm, Best Individual Feasibility Study (Prabal Lakhanpal) and Best Actuary (Peter Johnson).

At the VCIA 2022 Annual Conference, our Managing Partner participated in a panel that highlighted the scary long-term care landscape, but that ended on a high note in exploring the possibility of captives as a next generation solution for long-term care insurance.

With innovation embedded in the DNA of both Spring and captive insurance, we are interested in helping reshaping the long-term care market of the future. Check out the other discussions our team members had on VCIA session panels, or get in touch to talk in more detail about long-term care captive strategies.

In our latest podcast on Global Captive Podcast, our Managing Partner is joined by President and CEO of Spring’s client, edHEALTH to discuss the evolution of the captive program and its success.